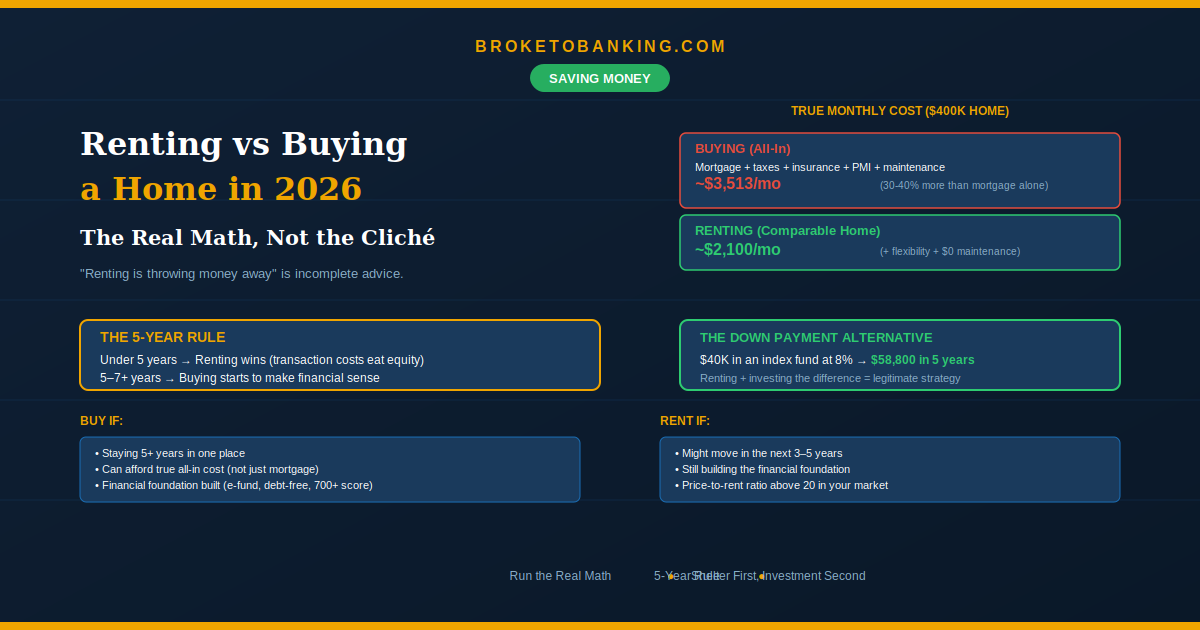

Renting vs Buying a Home in 2026 (The Real Math, Not the Cliché)

Quick Verdict: “Renting Is Throwing Money Away” Is the Worst Financial Advice in America

If you’re in your 20s or 30s and renting, someone in your life has told you you’re “throwing money away.” It sounds like wisdom. In the 2026 housing market, it’s closer to a mathematical myth.

Here’s what they’re not telling you: both renting and buying involve “throwing money away.” The real question is which unrecoverable costs — the money that never comes back to you — are lower for your specific life stage. Mortgage interest, property taxes, insurance, maintenance, and PMI are all “thrown away” too. Only the principal portion of your mortgage builds equity — and in the early years of a 30-year loan at 6–6.5%, that principal is shockingly small. On a $400,000 mortgage at 6.25%, only about $550 of your ~$2,460 monthly payment goes to principal in year one. The other $1,910 goes straight to the bank. You’re not buying a house in year one — you’re renting money from a bank.

The Quick Verdict:

- STACK: The 5–7 Year Rule ✅ — If you’re not staying at least 5 years, renting almost always wins the math.

- STACK: Run the unrecoverable cost comparison, not just “rent vs. mortgage” ✅ — The true cost of ownership is 30–40% higher than the mortgage alone.

- RUNNER UP: If you rent, invest the difference — Your down payment in an index fund can outpace home equity for years.

- SKIP: The “Forced Savings” Trap ❌ — Buying a house just because you’re bad at saving is an extremely expensive way to learn discipline.

The Unrecoverable Cost Comparison (The Honest Math)

To make a real decision, compare only the costs that never come back to you:

| Unrecoverable Costs of Renting | Unrecoverable Costs of Owning |

|---|---|

| Rent: ~$2,200/mo | Mortgage interest: ~$1,910/mo |

| Renter’s insurance: ~$20/mo | Property taxes: ~$400/mo |

| Maintenance: $0 | Maintenance (1% rule): ~$333/mo |

| Homeowner’s insurance: ~$170/mo | |

| PMI (if under 20% down): ~$150/mo | |

| Total: ~$2,220/mo | Total: ~$2,963/mo |

In many 2026 markets, it’s roughly $743/month cheaper to rent when you compare unrecoverable costs — even before you consider the $30,000+ in closing costs you lose the moment you sign. That gap is money you could be investing.

If you invest that $743/month difference in a broad index fund earning 8% annually, it grows to roughly $54,000 in 5 years. The “wasted” rent money was actually building wealth — just in a brokerage account instead of a house.

The 5-Year Rule: The Only Rule That Matters

In 2026’s market, buying only beats renting if you stay at least 5–7 years.

Transaction costs are massive. Closing costs buying (2–5%) plus commissions and fees selling (5–6%) means you lose 8–10% of the home’s value just to get in and out. On a $400,000 home, that’s $32,000–$40,000 in friction.

Appreciation needs time. At 3–4% annual growth (the historical average), it takes 5+ years for your home’s value increase to exceed transaction costs, interest, maintenance, and PMI combined.

Rent is cheaper monthly in most metros. In 2026, renting wins on a monthly basis in the majority of U.S. markets, especially coastal cities. The math only flips once appreciation and equity have had years to compound.

Simple version: 5+ years → buying starts to make sense. Under 5 years → renting wins. Under 3 years → buying is almost guaranteed to lose money.

The Opportunity Cost Nobody Talks About

What happens to your down payment if you invest it instead?

$40,000 down payment (10% on $400K home):

| Years | Invested in Index Fund (8%) | Home Equity (rough, after costs) |

|---|---|---|

| 3 | ~$50,400 | ~$20,000 |

| 5 | ~$58,800 | ~$55,000 |

| 7 | ~$68,500 | ~$95,000 |

| 10 | ~$86,400 | ~$155,000 |

At 5 years, it’s roughly a wash. At 7–10 years, home equity pulls ahead — especially with strong appreciation. But under 5 years, the invested money builds more wealth because there are no transaction costs eating returns.

“Renting and investing the difference” isn’t a consolation prize — it’s a legitimate wealth-building strategy. But it only works if you actually invest the savings. If you’d just spend the extra money, buying might win by default — not because the math is better, but because the mortgage forces the discipline.

When Buying Makes Sense

Buying isn’t wrong — it’s wrong as a default. The math works when:

You’re staying 5–7+ years. This gives appreciation time to cover the 8–10% friction cost of buying and selling.

You can afford the true all-in cost. Add 30–40% to the mortgage for taxes, insurance, maintenance. If that number strains your budget, you’re not ready.

You’ve hit Step 4 of the Money Sequence. Emergency fund of 3–6 months (owning makes emergencies more expensive), high-interest debt cleared, credit score above 700. Financial foundation first. House second.

You’re buying shelter, not an investment. Homes appreciate 3–4% — barely above inflation. The S&P 500 returns ~10%. Your primary residence is a consumption item — a place to live. Build wealth in your 401(k) and Roth IRA, not your house.

The Stability Bonus: There’s one non-financial argument for buying that’s real — a landlord can’t sell the house out from under you, raise your rent, or decline to renew your lease. If you have a growing family and want the peace of mind that your housing is locked in, that stability has genuine value that doesn’t show up in a spreadsheet.

When Renting Is the Smart Move

You might move in 3–5 years. Career mobility, relationship changes, or uncertainty about where you want to live all favor renting.

Your local price-to-rent ratio is above 20. If a home costs more than 20× the annual rent for a comparable place, renting is almost certainly cheaper. Many coastal metros are well above this in 2026.

You haven’t finished the Money Sequence. Credit card debt, thin emergency fund, credit score below 680 — buying amplifies financial stress, not solves it.

You value flexibility. A lease ends in 12 months. A mortgage doesn’t.

The Skeptic’s Friction Report

Forced savings is real — but so is the Forced Savings Trap. A mortgage forces equity building. Most people lack the discipline to invest the rent difference monthly. If you rent and spend the savings instead of investing them, buying wins by default. But if you’re disciplined enough to automate the difference into an index fund, renting and investing can win for years. Know yourself.

Rents rise; fixed mortgages don’t. Your landlord can raise rent every year. A 30-year fixed locks your P&I. After 10 years of increases, the buyer’s payment looks increasingly affordable — but only if you stay long enough.

A house is a place to live, not a get-rich-quick scheme. In 2026, the smartest move is often to stay light, keep your capital in the market, and wait for the math to flip in your favor.

FAQ

Am I really “throwing money away” renting?

No. You’re paying for shelter, flexibility, and zero maintenance. Mortgage interest, taxes, insurance, and repairs don’t build equity either — only principal does, and that’s a tiny fraction early on.

What credit score do I need to buy?

620 minimum for most conventional loans. 700+ for the best rates. See our credit score guide.

How much should I save before buying?

At minimum: 3–5% down + 2–5% closing costs + 3–6 months emergency fund that accounts for higher ownership costs. 20% down eliminates PMI.

Should I wait for rates to drop?

Nobody knows. Waiting for 3% rates is probably waiting forever. 2026 advice: “Date the rate, marry the house.” You can refinance later. You can’t undo buying at the wrong time.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: