How to Save $1,000 Fast (Even If You’re Starting From Zero)

Quick Verdict: Breaking the “Thousand Dollar Wall”

If you have less than $1,000 in the bank, you aren’t just “short on cash” — you are one flat tire away from a debt spiral.

In 2026, the cost of a basic emergency has ballooned to between $400 and $800. A cooling fan in your car. An urgent dental copay. A laptop repair. If you don’t have that cash sitting in a separate account, you’ll reach for a credit card. At 22%+ APR, that $600 repair will cost you over $700 by the time you pay it off. Do this cycle three or four times and you’re carrying thousands in debt from expenses that were predictable in aggregate — just not individually.

This is the Thousand Dollar Wall. Below it, every problem becomes a debt. Above it, every problem is just an inconvenience.

According to Bankrate’s 2026 Emergency Savings Report, only 47% of Americans could cover a $1,000 emergency without borrowing. Nearly 1 in 5 have no emergency savings at all. Getting to $1,000 isn’t about being rich — it’s about finally stepping out of the reactive cycle that keeps tight budgets stuck.

The Stack (Fastest path): The Liquidation Sprint — sell the Dead Capital sitting in your home. It’s the only way to generate real cash without trading more of your finite time. Runner-up move: The Loyalty Tax Reversal — call your insurance and internet providers. You are likely paying a $50+/month premium just for being a long-term customer who never complained. Skip entirely: The “I’ll save whatever’s left at the end of the month” approach. In an inflationary 2026 economy, there is never anything left. The $1,000 has to be moved before you see it.

Why $1,000 Specifically

Financial experts consistently cite $1,000 as the first real savings milestone because the math is anchored to reality. Most surprise expenses that force Americans to borrow fall in the $400–$800 range — car repairs, urgent medical bills, broken appliances, emergency travel. A $1,000 buffer absorbs the majority of these events without triggering debt.

Once you have it, the whole game changes. You stop reacting to crises and start making actual choices about money. It’s not the end goal — it’s the first step toward breathing room.

The Three Paths to $1,000

Your starting point determines the fastest route. Most people combine all three.

Path A: The Liquidation Sprint — You have Dead Capital sitting around that you can convert to cash. Usually the quickest route — often 1–2 weeks.

Path B: The Loyalty Tax Audit — You have subscriptions, bills, and loyalty taxes quietly bleeding your budget. Recovering $50–$100/month gets you there without earning a single extra dollar.

Path C: The Income Layer — Your budget is genuinely tight with nothing obvious to cut. Adding even $100–$200/month in recurring income changes the math dramatically.

Path A: The Liquidation Sprint — Recovering “Dead Capital”

The Verdict: STACK ✅ — Fastest path

Most households have hundreds of dollars in unused items in their closets, garages, and junk drawers. This is your Dead Capital — objects you don’t use that are worth real money to someone who will.

You are not trying to “get what it’s worth.” You are trading an object you don’t use for a financial shield you desperately need. Price to sell in 48 hours, not to maximize profit.

What sells fast on Facebook Marketplace:

- Old smartphones, tablets, game consoles, laptops

- Weights, dumbbells, exercise bikes, yoga gear

- Kids’ clothes, toys, gear they outgrew

- Name-brand kitchen appliances used twice (the air fryer, the instant pot)

- Tools and home equipment — duplicates, abandoned projects

The protocol:

- Spend one Saturday morning walking through your home and pulling anything untouched for 6+ months

- List each item with clear photos and honest descriptions — check what similar items are selling for

- Every dollar collected moves to a separate savings account before it touches your checking

Target: $300–$400 in the first two weekends. Combined with the loyalty tax audit below, that’s already 30–50% of your $1,000 goal before you’ve changed a single spending habit.

The Skeptic’s Friction Report:

The “But I Might Need It” Problem: If you haven’t used it in 6 months, the probability you’ll genuinely need it before you could replace it is very low. Sell it. If you ever truly need it again, you’ll buy it back — with the cash you just made from selling it.

Path B: The Loyalty Tax Audit — Stop the Leakage

The Verdict: STACK ✅ — Permanent gains

You aren’t “saving” money with this path. You’re stopping a slow corporate theft that’s been running on autopilot.

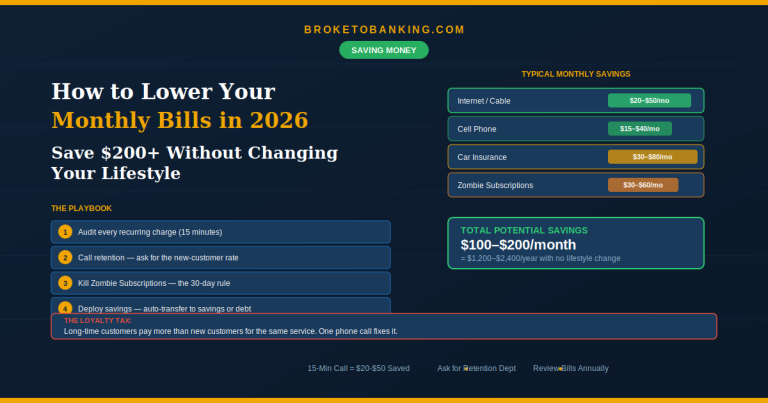

Step 1: The Insurance Call Call your car insurance company and say: “I’m shopping for lower rates — what can you do to keep my business today?” Retention departments have pricing authority that frontline reps don’t. The average savings from this call is $40–$60/month according to published insurance comparison research.

Step 2: The Zombie Subscription Hunt Open your bank app and pull up the last 90 days. Highlight every recurring charge. For each one, ask: have I actively used this in the last 14 days? If not, cancel it.

Most people find $30–$80/month in subscriptions they’re paying for but not actively using. That’s $360–$960 per year — nearly your entire $1,000 goal, just waiting to be uncanceled.

Step 3: Phone and Internet Loyalty Tax Call your internet and phone providers and ask for their current new-customer rate. If they won’t match it, switch. Easy $20–$40/month back in your pocket, permanently.

The math that matters: Finding $100/month in leaks is mathematically identical to getting a $1,500 annual raise — after taxes. One afternoon of calls.

The Skeptic’s Friction Report:

The “Small Numbers” Problem: $50/month feels meaningless against a $1,000 goal. Reframe it: $50/month is $600/year, every year, permanently. These savings continue compounding while you sleep. The call takes 15 minutes and pays you back indefinitely.

Path C: The Income Layer — For the Truly Broke

The Verdict: STACK ✅ — Transforms the timeline

If your budget is already “beans and rice” tight, you cannot cut your way to $1,000. You have to earn your way there. Even a small amount changes the math fast.

The 30-day math: To hit $1,000 in 30 days, you need roughly $33 per day. That sounds hard until you break it into pieces — a TaskRabbit job ($75–$100), two delivery shifts ($80–$120), one Marketplace sale ($50–$100). Four moves gets you there.

Fastest income options:

- TaskRabbit — moving help, furniture assembly, yard work. $25–$40/hour. Two jobs per month = $100–$200 in 2–3 hours of work.

- Delivery apps (DoorDash, Uber Eats, Instacart) — $15–$25/hour depending on market and timing. Five hours a week adds $300–$500/month.

- Fiverr — data entry, writing, graphic design, video editing. Low barrier, scales with reviews.

- Benefits.gov — a 10-minute eligibility check for over 1,000 federal and state programs: SNAP, energy assistance, childcare subsidies, Medicaid. If the state covers $100 of your grocery bill, that’s $100 that stays in your savings account.

The Windfall Protocol: Any unexpected cash — tax refund, birthday money, work bonus — goes directly to the $1,000 goal before it touches your checking account. The average federal tax refund in 2025 was over $3,000. One transfer covers the entire goal.

The Skeptic’s Friction Report:

The Bandwidth Problem: If you’re already working full time, significant gig income requires real time. Be honest about sustainability. Even one TaskRabbit job per month generating $75–$100 is meaningful progress. The goal is a small, manageable income layer — not running yourself into the ground.

The “Friction” Strategy — How to Make It Actually Stick

All three paths generate the money. This step ensures it stays saved.

If you save $1,000 in your regular checking account, you will spend it. Checking Account Gravity is too powerful. Money that is visible and accessible gets absorbed by daily life. Every time.

The fix: Open a separate high-yield savings account at a different bank than your checking. Ally, Marcus, and SoFi all take 10 minutes to open, have no minimums, and earn around 4% APY.

The 2–3 day transfer window between the HYSA and your checking account is the entire point. It prevents you from using your emergency fund for a “Friday night emergency” — which isn’t an emergency.

The Ghost Paycheck: Set up an automatic transfer of $25 per week from your checking to your HYSA. You won’t feel $25. But the momentum of watching the balance grow is a psychological win that keeps you engaged. Automate it and forget it.

The 30-Day Sprint Plan

| Week | Action | Estimated Result |

|---|---|---|

| Week 1 | List 5–10 items on Facebook Marketplace | $150–$300 |

| Week 1 | Open a separate HYSA | Account ready |

| Week 2 | Cancel unused subscriptions | $30–$80/month recovered |

| Week 2 | Call insurance — say “shopping for lower rates” | $40–$60/month recovered |

| Week 3 | Two gig shifts (TaskRabbit or delivery) | $150–$200 |

| Week 3 | Check Benefits.gov eligibility | Variable |

| Week 4 | Sell remaining items, route all funds to HYSA | $100–$200 |

| Ongoing | Ghost Paycheck auto-transfer + one gig/month | $1,000 reached |

This is an aggressive plan. Most people hit $500–$750 in the first month and finish in the second. For genuinely tight budgets, 60–90 days is an honest timeline.

What to Do After You Hit $1,000

- Keep the money in the HYSA earning 4% APY. Don’t move it back to checking.

- Set the next target: $2,500, then one month of expenses, then three months.

- Define “emergency” clearly — unplanned, urgent, necessary. Planned expenses don’t count.

- The Replacement Rule: Any time you use the fund for a real emergency, every extra dollar goes to refilling it first — before any other financial goal — until it’s whole again.

FAQ

How long does this realistically take? Using the Liquidation Sprint plus one insurance call, many people reach $500 in the first two weeks. The full $1,000 typically takes 30–90 days using all three paths. For very tight budgets with no sellable items, 3–6 months at $50–$100/month saved is honest and achievable.

Where should I keep the $1,000? In a separate HYSA at a different bank than your checking — Ally, Marcus, or SoFi. The physical separation prevents Checking Account Gravity from absorbing it.

Should I save $1,000 before paying off debt? Yes. Build the buffer first, then attack high-interest debt. Without the buffer, every emergency adds more debt and resets your progress.

What counts as a real emergency? Unplanned, urgent, and necessary: car repairs to get to work, medical bills, urgent home fixes, family emergencies. If you had two weeks to plan for it — it’s not an emergency.

What if I keep dipping into the fund? Your regular budget has gaps. Return to the expense audit and income layer steps. The emergency fund can’t fix a structural budget shortfall — it can only absorb genuine surprises.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: