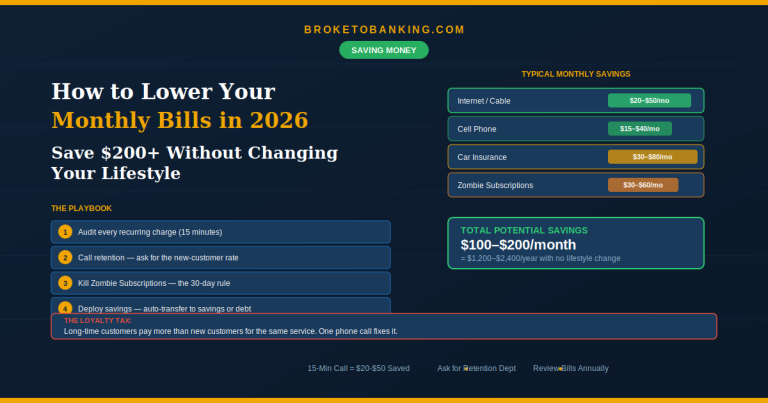

What Is Your Net Worth? (How to Calculate the Number That Actually Matters)

Quick Verdict: It’s the Scoreboard for Everything We’ve Taught You

Your salary tells you how much money flows through your life. Your credit score tells lenders how much to charge you. Your net worth tells you where you actually stand. It’s the single most important number in personal finance — and most people have never calculated it.

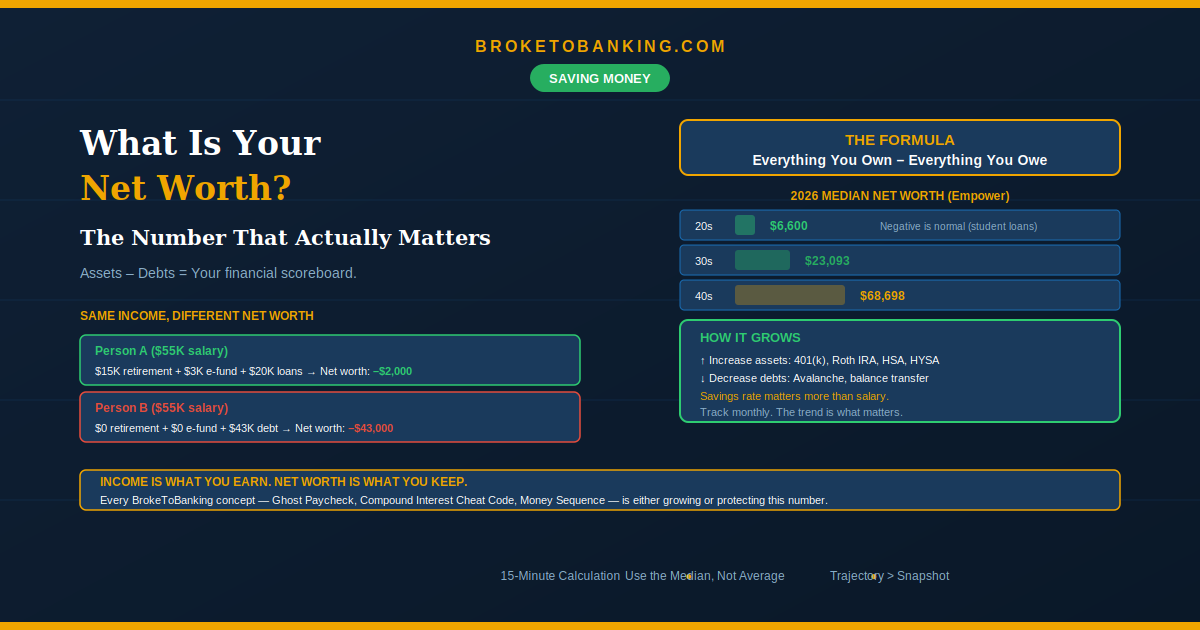

Net worth = everything you own (assets) minus everything you owe (debts)

Every dollar in your HYSA, every share in your Roth IRA, every dollar of equity in your car — minus your credit card balance, student loans, and any other debt. One number that captures the combined effect of your income, spending, saving, investing, and debt over your entire life. It’s your financial autobiography.

If your net worth is negative — and for many people under 30, it is — that’s normal. It’s also temporary, as long as the trajectory is pointing up. Don’t sweat the snapshot. Sweat the slope.

The Quick Verdict:

- STACK: Calculate your net worth today — it takes 15 minutes ✅ — You can’t improve what you don’t measure.

- STACK: Track it monthly or quarterly ✅ — The trend matters more than any single number.

- RUNNER UP: Use the median, not the average — Averages are skewed by billionaires.

- SKIP: Panicking over a negative number ❌ — Student loans make negative net worth in your 20s statistically normal.

- SKIP: Counting “Vanity Assets” ❌ — Your furniture, clothes, and tech aren’t assets. If you can’t sell it for real cash today, it’s not on the list.

How to Calculate It (15 Minutes)

Add Up Your Assets (What You Own)

| Asset | Example Value |

|---|---|

| Checking account(s) | $2,400 |

| High-yield savings | $3,200 |

| 401(k) balance | $8,500 |

| Roth IRA balance | $2,100 |

| HSA balance | $1,800 |

| Car (current market value) | $12,000 |

| Other (brokerage, crypto, etc.) | $500 |

| Total Assets | $30,500 |

Subtract Your Liabilities (What You Owe)

| Debt | Balance |

|---|---|

| Credit card debt | $2,800 |

| Student loans | $28,000 |

| Auto loan | $9,500 |

| Other | $0 |

| Total Liabilities | $40,300 |

The Math

$30,500 – $40,300 = –$9,800

This person’s net worth is negative $9,800. Does that mean they’re failing? Not at all. It means they’re 27 with student loans — like millions of other Americans. The number is a starting point, not a verdict.

Where Do You Stand? (2026 Benchmarks)

Don’t compare yourself to the average — those numbers get distorted by a small number of extremely wealthy people. The median (the true midpoint) gives you a realistic benchmark.

| Age | Average Net Worth | Median Net Worth |

|---|---|---|

| 20s | $139,243 | $6,600 |

| 30s | $325,952 | $23,093 |

| 40s | $750,578 | $68,698 |

| 50s | $1,364,050 | $180,227 |

| 60s | $1,577,907 | $274,564 |

Source: Empower Personal Dashboard, January 2026

A 27-year-old with a net worth of $6,600 is right at the median — literally the middle of the pack. If you’re at $25,000 in your late 20s, you’re significantly ahead of most peers. Negative net worth is common in your 20s because student loans dominate the equation. What matters is direction: are you making it less negative each month?

Why Net Worth Matters More Than Income

Two people earning $55,000/year can live in completely different financial realities:

Person A: $15K retirement, $3K emergency fund, $0 credit card debt, $20K student loans → Net worth: –$2,000

Person B: $0 retirement, $0 emergency fund, $8K credit card debt, $35K student loans → Net worth: –$43,000

Same income. A $41,000 gap. The difference is how they managed the money that flowed through their lives.

If your income goes up but your net worth stays flat, you’re running faster on a treadmill that isn’t moving. Income is what you earn. Net worth is what you keep. Every concept on this site — the Ghost Paycheck, Checking Account Gravity, Interest Gravity, the Compound Interest Cheat Code — is either growing or protecting this number.

How to Increase Your Net Worth (The BrokeToBanking Playbook)

Net worth grows two ways: increase assets or decrease debts. Here’s how it maps:

Reduce liabilities (kill debt):

- Pay off credit card debt — stops Interest Gravity at 22%

- Attack student loans above 6% — Avalanche method

- Balance transfer — 0% pause on interest

Grow assets (build wealth):

- Build your emergency fund in a HYSA

- Max your 401(k) match + Roth IRA + HSA

- Invest in index funds via DCA — being on the sidelines is a Laziness Tax you can’t afford

Protect net worth:

- Automate everything — willpower fails, systems don’t

- Budget your margin — deploy every dollar intentionally

- Negotiate your salary — the biggest single lever

How to Track It (Simple and Free)

Option 1: A spreadsheet. Google Sheets. Two columns: Assets and Liabilities. Update on the 1st of every month. Takes 5 minutes once set up.

Option 2: An app. Empower (free) links your accounts and calculates automatically. YNAB tracks it too.

Set a recurring calendar reminder — monthly or quarterly. The act of seeing the number changes your behavior. When it goes up $500 in a month, every good decision feels worth it. When it dips, you investigate and correct. Your savings rate matters more than your salary. The decisions you make in your late 20s and 30s compound into enormous gaps by your 50s.

Your net worth is your financial autobiography. It tells the story of your discipline, your risks, and your recovery. Whether you’re at –$50K or +$500K, the goal is the same: make next month’s number better than this one.

FAQ

What if my net worth is negative?

If you’re under 35 with student loans, that’s statistically normal. The median for 20-somethings is just $6,600. Focus on the slope: are you making it less negative each month?

Should I include my car?

Yes — at current market value (KBB or Carvana), minus the remaining loan. If you owe more than it’s worth, it’s a net negative.

Should I include my home?

Yes — estimated value minus mortgage. But also calculate it without the house to see your liquid picture. You can’t easily spend home equity on retirement.

How often should I check?

Monthly or quarterly. More frequent = stress over market noise. Less frequent = lost behavioral benefit.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: