Debt Snowball vs Debt Avalanche: Which Payoff Method Actually Works?

Quick Verdict: Most People Are Asking the Wrong Question

Everyone wants to know: “Which one saves more money?”

The honest answer? That’s the wrong question.

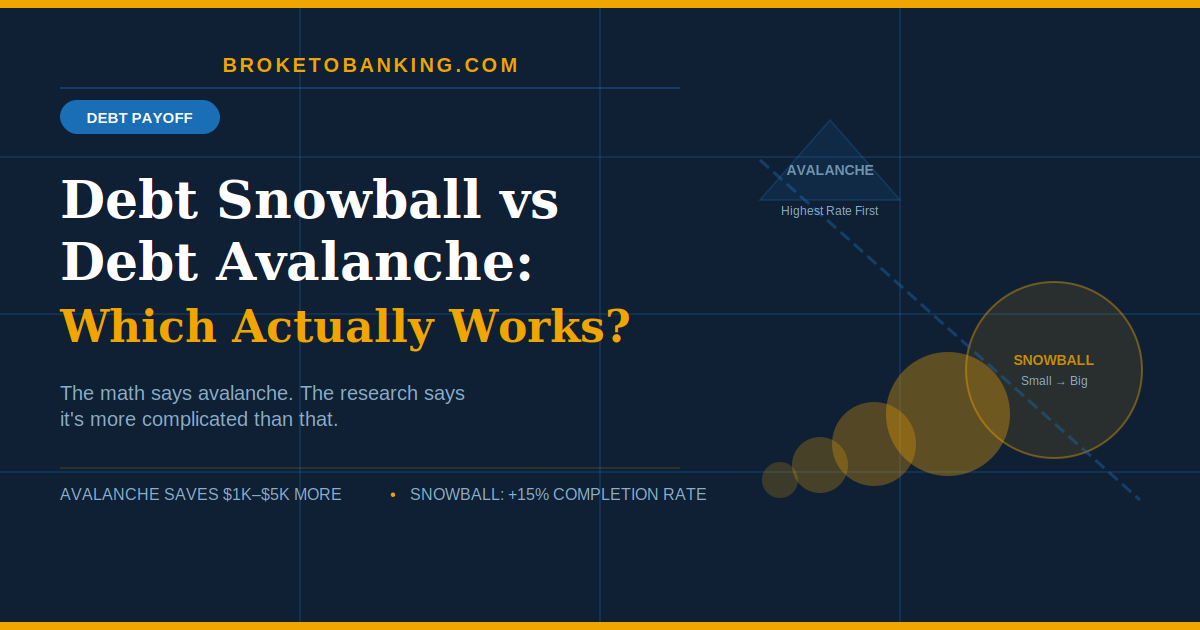

The Debt Avalanche (highest interest first) wins on pure math. In most real-life scenarios with different interest rates, it saves $1,000–$5,000 in total interest compared to the Snowball. If math were the only thing that mattered, everyone would use Avalanche and we could stop arguing.

But math isn’t the only thing that matters. Behavior is.

A 2016 study in the Journal of Consumer Research showed that people using the Snowball method were more likely to stick with their plan than those using mathematically optimal methods. Harvard Business Review analysis found the Snowball gives you about a 15% better chance of actually becoming debt-free — because those quick early wins keep you motivated long enough to finish.

So the real question isn’t “Which method saves the most on paper?” It’s “Which method will I actually stick with until the end?”

Best for most people who just want to win: Debt Avalanche — if you can stay consistent, it saves the most cash. Best for people who’ve quit before: Debt Snowball — the psychological boost is worth the small extra cost. Absolute skip: Jumping back and forth between methods every few months. Pick one, commit, finish.

What Each Method Actually Does

The Debt Avalanche — Killing “Interest Gravity”

The Verdict: STACK ✅ (If you hate banks)

List all your debts from highest interest rate down to lowest. Pay minimums on everything. Throw every extra dollar at the highest-rate debt first. When it’s gone, roll that full payment to the next highest rate. Repeat.

Why it makes sense: Interest is the real enemy. In 2026, with the average credit card APR at 22.8%, your highest-rate debt is a financial house fire. The Avalanche puts out the biggest fire first before touching anything else.

Example order:

- Credit card at 26.99% → attack this first

- Personal loan at 18.5%

- Car loan at 7.9%

- Student loan at 5.5% — last

The Skeptic’s Friction Report:

The “Slog” Problem: The Avalanche feels like a grind. If your highest-interest debt is also your largest balance — say, a $10,000 card at 24% — you might work for 12 months without completing a single payoff. No wins. No crossed-out names. This is exactly where most people quit. If that’s you, read the Snowball section carefully.

The Debt Snowball — Paying the “Motivation Tax”

The Verdict: STACK ✅ (If you need a win)

List your debts from smallest balance to largest. Ignore the interest rates entirely. Pay minimums on everything. Throw every extra dollar at the smallest balance. When it’s paid off, roll that payment to the next smallest. Keep going.

Why it makes sense: Humans are not spreadsheets. Harvard Business Review researchers found that the “small win” effect is one of the strongest predictors of debt payoff success. Eliminating a $400 medical bill in month one gives you the mental fuel to tackle a $5,000 card in month six.

Example order:

- Medical bill for $400 → knock it out first

- Store card for $900

- Credit card for $3,200

- Car loan for $8,500 — last

Notice: interest rates don’t factor into the Snowball order at all. A 0% medical bill might get paid before a 26% credit card if the balance is smaller.

The Motivation Tax: By ignoring a high-interest card to pay off a 0% medical bill first, you’re voluntarily paying the bank more interest. This is the Motivation Tax — the premium you pay for the psychological wins that keep you in the game. For many people, that tax is worth every penny. Especially if it’s the only thing standing between them and quitting.

The Skeptic’s Friction Report:

The Math Cost: The Motivation Tax is real money. On a typical $15,000 debt portfolio with varied rates, the Snowball costs $1,200–$4,500 more in total interest than the Avalanche. If you’re highly disciplined and can stay motivated without early wins, that gap goes straight into your pocket by using Avalanche instead.

The Completion Gap — The Number That Settles It

Here’s the stat that changes the whole conversation:

Harvard Business Review analysis found the Snowball method improves the likelihood of becoming debt-free by approximately 15% compared to unstructured repayment — specifically because of psychological momentum from early wins.

15% is not a small number when we’re talking about something as difficult as sustaining a debt payoff plan for 18–24 months.

Avalanche wins on math. Snowball wins on completion rates. Both are true simultaneously — which is why the “correct” answer depends entirely on knowing yourself honestly.

Quick self-check:

- Have you tried debt payoff before and given up? → Snowball

- Do you love spreadsheets and optimizing every penny? → Avalanche

- Got one massive, expensive debt dominating everything? → Avalanche

- Got a bunch of small annoying debts that feel overwhelming? → Snowball

The 10-Point Rule — Your Simple Decision Tool

As researchers, we don’t like vague feelings. Here’s a concrete framework:

Step 1: List every debt with its interest rate. Step 2: Find the spread between your highest and lowest rate. Step 3: Apply the rule:

| Rate spread between highest and lowest | Recommended method | Why |

|---|---|---|

| Less than 5 points | Snowball | Interest savings are too small — take the psychological wins |

| 5–10 points | Dealer’s choice | Depends on your personality — spreadsheet lover or stressed? |

| More than 10 points | Avalanche | The math gap is too wide to ignore. The Motivation Tax becomes too high. |

Real example where Snowball wins: 22% credit card ($1,800), 0% medical bill ($600), 8% car loan ($6,200). Knocking out the $600 medical bill first costs almost nothing in extra interest and gives instant momentum. Snowball is the right call.

Real example where Avalanche wins: 27.99% card ($4,200), 19.99% card ($1,800), 12% personal loan ($3,000). A 16-point spread. Ignoring that 28% card to pay a 12% loan is financially reckless. Avalanche is the clear winner.

The 2026 Reality — Why Most Plans Fail Before the Method Even Matters

Neither method works if you ignore the friction points that derail most debt payoff attempts:

The Safety Buffer Gap: If you start either method without a $500 emergency fund, the first flat tire goes back on the credit card — resetting your progress and killing your momentum. Build the buffer before you start the plan.

The Zombie Subscription Problem: Trying to pay off debt while still paying $60–$80/month in forgotten subscriptions is handing that money to corporations while your debt compounds at 22.8%. Run the subscription audit first. Every dollar recovered goes directly to the payoff plan.

The Points Delusion: If you’re keeping a card active to earn 1% cash back while paying 22.8% interest, you’re a victim of marketing, not a savvy consumer. Freeze the cards you’re targeting. You cannot run up a down escalator.

The Hybrid Approach — If You Want Both

Some people start with Snowball to eliminate 1–2 small debts and build momentum, then switch to Avalanche once they’ve proven to themselves they can stick with a plan.

This works — but only if you switch after completing at least one payoff, not mid-plan out of restlessness. Switching too early just creates confusion and resets the momentum you were building.

Side-by-Side Comparison

| Factor | Debt Snowball | Debt Avalanche |

|---|---|---|

| Order of attack | Smallest balance first | Highest interest rate first |

| Total interest paid | More — the Motivation Tax | The least possible |

| Time to debt-free | Slightly longer | Slightly faster |

| First win | Comes fast | Takes much longer |

| Completion rate | Higher (15% edge) | Lower |

| Best for | People who need momentum | People who love the math |

| Rate gap matters? | No | Yes — the bigger the gap, the more Avalanche wins |

| Use when | Rates are similar OR you’ve quit before | Rate spread exceeds 10 points |

What Actually Matters More Than the Method

Both methods only work with the right foundation:

- Stop adding to the balances. Freeze the cards you’re targeting. You cannot pay off a debt that keeps growing.

- Find extra dollars to redirect. Even $50–$100/month extra makes a dramatic difference in the timeline.

- Build a $500 buffer first. Without it, every surprise expense resets your progress to zero.

- Pick one method and finish it. An imperfect Snowball that gets completed is worth infinitely more than a perfect Avalanche you quit in July.

If you have one massive credit card at 26% and several small loans at 8%, Avalanche is your only sane choice — you’re bleeding out and need to stop the main wound first. If you have six small debts at similar rates, the Snowball is a masterstroke. The psychological high of crossing names off the list will turn you into a debt-eliminating machine.

FAQ

Which method actually saves more money? Avalanche — typically $1,000–$5,000 less interest in real-world debt scenarios. But only if you finish the plan. An abandoned Avalanche saves nothing.

Is the Debt Snowball actually effective? Yes. Published research shows it keeps more people engaged because of early wins. Harvard Business Review analysis found a 15% higher completion rate versus unstructured repayment.

What if my rates are all pretty similar? Snowball. When the rate spread is under 5 points, the interest savings from Avalanche are minimal. Take the psychological wins.

Can I switch methods partway through? You can, but stay consistent until you’ve completed at least one payoff. Switching too early loses the momentum you’ve built and extends your timeline.

Should I pay off debt or invest at the same time? Grab any 401(k) employer match first — that’s a 50–100% guaranteed return that beats even 27% APR debt mathematically. After the match, attack high-interest debt before investing. Once the expensive debt is gone, investing becomes dramatically more powerful.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: