How to Get Out of Debt on a Low Income: The Only Guide You Need

Quick Verdict: The “Interest Gravity” Problem

If you’re living on a low income, standard debt advice is insulting. Most “experts” tell you to cut the $5 latte and redirect $150 a month toward your credit cards. But in 2026, if you’re making $40k a year, that $150 doesn’t exist. It was already eaten by a 20% rent hike and a 25% jump in grocery prices.

When your income is tight, you aren’t fighting a spending problem — you’re fighting Interest Gravity. At the average 22.8% APR in 2026, your debt is growing faster than your ability to pay it. If you’re only paying minimums, you aren’t “paying off” debt. You’re paying the bank a monthly fee to keep you in a hole.

According to the Federal Reserve Bank of New York, total U.S. credit card debt hit a record $1.3 trillion in 2026. The average person now carries $6,500–$6,800 in revolving balances according to Experian and TransUnion data. A $4,000 balance at 22.8% APR on minimum payments alone takes over 7 years to clear and costs roughly $3,600 in interest — nearly doubling the original debt.

This guide isn’t about some magical 90-day miracle. It’s the skeptical, data-backed plan to break the gravity — when every single dollar you have already has a job.

The “Stack” (Do This or Don’t Bother): Freeze the cards. If you make an extra payment Tuesday and charge gas Friday, you’re running up a down escalator. You will never win. The “Runner Up”: The Debt Avalanche — highest interest first. Every dollar going toward a 10% loan while a 25% card exists is a 15% monthly loss. The “Skip”: Debt settlement companies. Predators in suits. They charge up to 25% of your debt to negotiate something you can do yourself in a 10-minute phone call — and they destroy your credit for years while doing it.

Why Getting Out of Debt Feels Different on a Low Income

Most debt advice assumes you have a few hundred extra dollars per month to redirect. On a low income, that slack often doesn’t exist. After rent, utilities, groceries, and minimum payments, you might have $50–$150 left — and that cushion is also supposed to cover the next surprise bill that always arrives before the month ends.

This is the Interest Gravity problem in action. The interest compounds faster than you can pay it down. Minimum payments keep the balance roughly flat. One car repair or medical copay and you’re sliding backward again.

The plan below was built for this reality, not for someone with $500/month of disposable income to throw at it.

Step 1: The “Down Escalator” Protocol — Freeze the Balance First

The Verdict: STACK ✅

You cannot budget your way out of a debt that is still being actively used.

The rule: The cards go in a drawer — or better yet, in a bowl of water in the freezer if you need the extra friction. Move every recurring subscription to your debit card. Gas, groceries, anything essential — cash or debit only from here.

It sounds obvious. It’s almost universally skipped. People make an extra payment on Tuesday and charge $80 on Friday, and suddenly they’re going backward. The payoff plan is worthless if the balance keeps growing.

The honest reality: If you genuinely cannot cover an essential expense without the card, you don’t have a debt problem yet — you have an income gap problem. The Interest Gravity is too strong at this stage. Focus on Step 3 first.

The Skeptic’s Friction Report:

The “Points” Problem: You’re not saving money with rewards. At 22.8% APR, you’re paying hundreds in interest to earn cash back worth tens of dollars. The math never works in your favor while carrying a balance.

Step 2: The “Battlefield Map” — Full Debt Inventory

The Verdict: STACK ✅

Most people carry a vague cloud of anxiety about their debt. You need a map, not a feeling.

The task: List every single debt — balance, APR, minimum payment. No judgment. Just facts.

| Debt | Balance | APR | Minimum Payment |

|---|---|---|---|

| Chase Visa | $3,200 | 24.99% | $64 |

| Discover | $1,800 | 19.99% | $36 |

| Medical bill | $600 | 0% | $25 |

| Personal loan | $2,400 | 14.5% | $78 |

Now total up your monthly minimums. For many households carrying multiple debts, that number is $300–$500 per month — almost all of it going to interest, barely touching principal.

Here’s the real number to focus on: if you owe $6,000 at 22.8% APR, you’re paying roughly $114 per month just for the privilege of owing money. That $114 is your Interest Gravity. Your first goal is to start shrinking it.

The Skeptic’s Friction Report:

The “I Already Know” Problem: You know the rough total. You almost certainly don’t know every APR and which debt is costing you the most per month. The inventory is about ranking the damage, not confirming the number.

Step 3: Finding the “War Chest” — The $50 That Changes Everything

The Verdict: STACK ✅

On a low income, you don’t have slack. You have to steal money back from the corporations already taking it from you.

On the expense side:

Zombie Subscriptions: Pull your last 90 days of bank statements. Most people find $30–$60/month in charges they forgot about. Cancel anything you haven’t actively used in two weeks.

The Loyalty Tax Call: Call your car insurance and internet providers today. Tell them you’re switching to a competitor. In 2026, retention departments are under pressure. This one 20-minute move routinely recovers $40–$70 per month — or $400–$600 per year — for most households.

On the income side:

The Clutter Graveyard: Most households have $300–$400 sitting in closets in the form of an old tablet, a bike nobody rides, or clothes that no longer fit. List three things on Facebook Marketplace this weekend. That money goes directly to debt — or to a small cash buffer so the next flat tire doesn’t go back on the card.

Benefits.gov Audit: A 10-minute eligibility scan covers over 1,000 federal and state programs — SNAP, energy assistance, childcare subsidies, Medicaid. Millions of qualifying Americans never apply.

One Recurring Gig: Delivery shifts, TaskRabbit jobs, a skill on Fiverr. Even $100–$150/month extra changes the timeline significantly. At $100/month extra on a $4,000 balance at 24.99% APR, you pay it off in under 2 years instead of over 7.

The Skeptic’s Friction Report:

The Bandwidth Problem: If you’re already working full time and managing a household, a side hustle may genuinely not be possible. In that case, the expense-side wins are your primary lever. Even $50/month redirected consistently is $600 in principal reduction per year — plus the compounding interest you didn’t pay.

Step 4: The “Symmetry” Call — Negotiate Your Rate

The Verdict: STACK ✅

This is the most underused lever in personal finance. It takes 10 minutes and most people never try it.

Call each credit card company and say: “I’ve been a customer for X years and I’ve always paid on time. I’m working hard to pay down my balance — can you lower my interest rate?”

Based on published consumer finance research, roughly 70% of people who ask for a rate reduction receive one. The average reduction is 3–6 percentage points. On a $3,000 balance, a 5-point drop saves approximately $150 per year in interest — with one phone call.

If they say no, call back in 90 days. You have nothing to lose and potentially hundreds to gain.

The Skeptic’s Friction Report:

The “They’ll Say No” Fear: About 30% of callers don’t get a reduction on the first attempt. The worst outcome is the same rate you’re already paying.

Step 5: Avalanche vs. Snowball — Math vs. Mindset

The Verdict: YOUR CHOICE ⚖️

Once you have extra dollars to redirect, they all go toward one debt while you pay minimums on everything else.

The Debt Avalanche (The Skeptic’s Choice): Attack the highest interest rate first. Pure math. When it’s gone, roll that payment to the next highest rate. This is the fastest way to stop the Interest Gravity — you eliminate the biggest drain on every dollar you send in.

On a $4,000 balance at 24.99% with $100 extra/month, you save roughly $800–$1,000 in interest overall compared to minimum payments alone. These are calculations based on standard amortization at 24.99% APR.

The Debt Snowball (The Human Choice): Pay off the smallest balance first, regardless of rate. The early payoff wins create momentum and make it easier to stay in the game for the 18–24 months this realistically takes.

Our honest take: If you’re a math person and the rate difference is large — say one card at 26% and another at 12% — go Avalanche. The savings are too significant to ignore. If the rates are close or you know you get discouraged easily, go Snowball. The best method is the one you don’t quit in Month 3.

The Skeptic’s Friction Report:

The “Which Is Really Better?” Problem: Both work. Neither works if you abandon it at month four. Pick the one that keeps you in the game for the full run.

Step 6: The Consolidation Trap — Proceed With Caution

The Verdict: PROCEED WITH CAUTION ⚠️

You’ll see ads everywhere for “one low monthly payment.” This is not automatically good news.

The trap: Lowering your monthly payment almost always means extending your loan term — from 3 years to 6 years, for example. You feel better today, but you pay thousands more in total interest. Lower payments are not the goal. Faster payoff at lower total cost is the goal.

The one real exception — 0% balance transfer cards: If you can move your 24.99% debt to a 0% promotional rate for 12–21 months, this is one of the most powerful tools available. Attack the balance hard during the window. But if you use that newly empty card for even one purchase, you’ve just doubled your problem.

Personal loans at 10–14% to replace cards at 24.99% also make clear mathematical sense — as long as the old cards get closed or frozen immediately after.

The Skeptic’s Friction Report:

The Debt Settlement Warning: Settlement companies tell you to stop paying creditors, pocket the missed payments, then negotiate. Your credit score tanks for up to 7 years. You pay them up to 25% of your enrolled balance. Nonprofit credit counseling through the NFCC is a legitimate alternative if you genuinely need structured help.

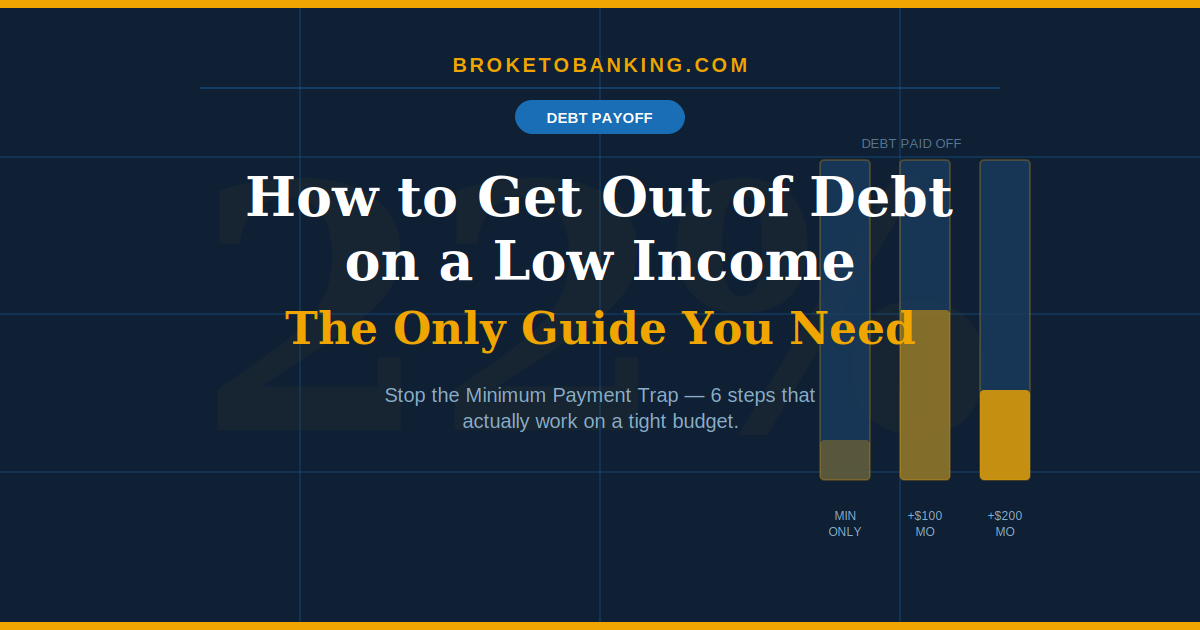

The Realistic 2026 Timeline

For $6,500 in credit card debt at 22.8% average APR:

Minimum payments only → Over 7 years to pay off → Approximately $3,600 in interest → Total cost: approximately $10,100

With $100 extra per month → About 3.5 years → Approximately $1,800 in interest saved → Total cost: approximately $8,300

With $200 extra per month → Under 2 years → Under $800 in interest → Total cost: approximately $7,300

These are straight amortization calculations at 22.8% APR — your actual results depend on your specific rates and consistency.

Your Priority Order

| Week / Month | Action | Why |

|---|---|---|

| Week 1 | Complete the Debt Inventory | You finally see the real battlefield |

| Week 1 | Freeze the cards | Stops the balance from growing |

| Week 2 | Zombie sub audit + Loyalty Tax call | Finds your first $50–$100/month |

| Week 2 | Call for rate reductions | 10 minutes, potentially hundreds saved |

| Month 1 | Pick Avalanche or Snowball and start | Momentum begins |

| Month 2+ | Every extra dollar to the target balance | Consistency beats intensity |

FAQ

Can you actually get out of debt on a low income? Yes. The timeline is longer and the margin for error is smaller, but the rules are identical at any income level: stop adding to the balance, find every extra dollar, and apply them consistently to the highest-cost debt.

Should I use a debt settlement company? For most people, no. They charge up to 25% of your enrolled balance, tell you to stop paying creditors (which destroys your credit), and take years to deliver results you could achieve faster on your own. Nonprofit credit counseling through the NFCC is a legitimate alternative.

What’s the fastest way to pay off credit card debt? Freeze new charges, find every possible extra dollar, call for a rate reduction, and redirect everything extra to the highest-APR balance. A 0% balance transfer card — if you qualify — can dramatically accelerate it.

Does paying off debt hurt my credit score? Paying off credit card balances generally helps your score by lowering your credit utilization ratio. The long-term benefit of being debt-free far outweighs any small short-term variation.

Should I build an emergency fund first or attack the debt? Build a $500 buffer first. Without it, every surprise expense adds more debt and resets your progress. With it, you can pay down debt without derailing every time life happens.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: