How to Budget When Your Income Changes Every Month (2026)

Quick Verdict: The Baseline Budget System

Most budgeting advice assumes one big thing: you get the same paycheck on the same day every month. If you’re a freelancer, gig worker, server, commission salesperson, or anyone whose income looks like a mountain range — $6,000 one month, $2,800 the next — that advice falls apart the moment your deposit doesn’t match the plan. A static budget isn’t just useless for variable income; it’s a recipe for credit card debt.

The fix isn’t a better spreadsheet. It’s a completely different way of thinking we call the Baseline Budget System. Instead of building your budget around what you hope you’ll make, you build it around the worst month you’ve actually had. When you plan from the floor instead of the middle, the good months become opportunities instead of excuses to overspend.

Roughly 73 million Americans work as freelancers or independent contractors. If you’re one of them — or your income just isn’t steady — this system is built exactly for how your money actually works.

The Quick Verdict:

- STACK: Budget from your lowest month, not your average ✅ — If your worst month in the last six was $3,200, that’s your budget. Everything above it is bonus money with a job to do.

- STACK: Build an Income Buffer account ✅ — The single most important tool for turning unpredictable income into a predictable life.

- RUNNER UP: Use YNAB or a zero-based app — Apps built for variable income (especially YNAB) beat traditional budgeting tools for irregular earners.

- SKIP: Budgeting from your “expected” income ❌ — Forecasting is just a fancy word for gambling with your rent money.

Step 1: Find Your Baseline Number

The whole system starts with one number: your Baseline — the minimum monthly income you can realistically expect, based on real history.

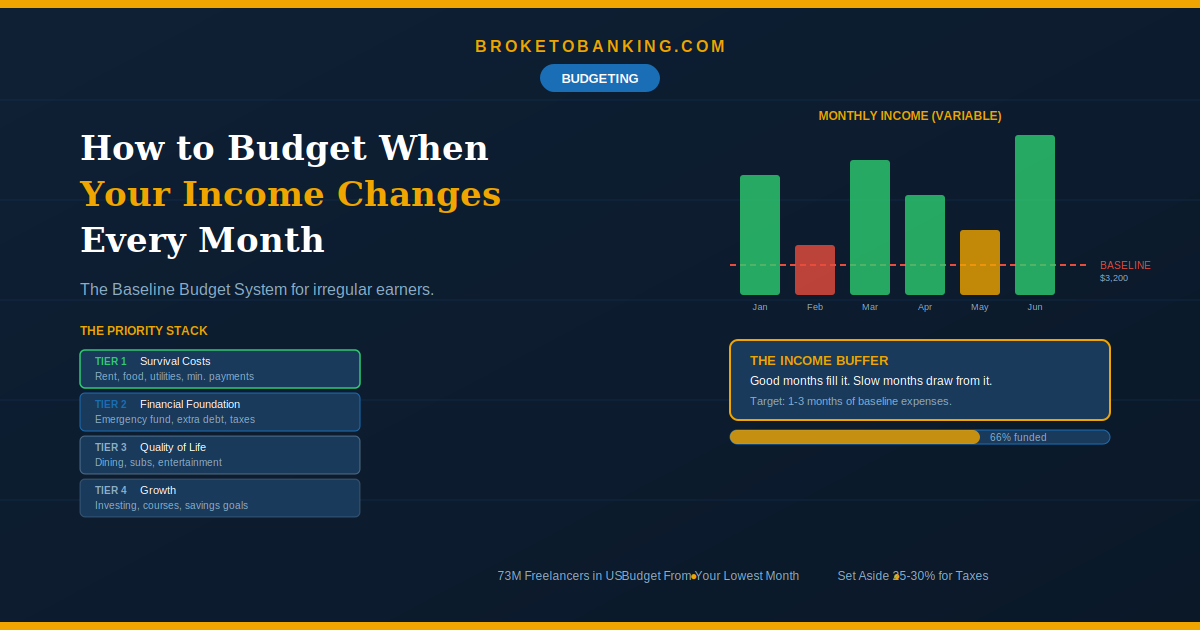

Pull up your last 6–12 months of income. Find the lowest month. That’s your Baseline. Not the average, not the “typical” month — the worst one. This is your Safe Zone.

Example: If your last six months looked like $4,800, $3,200, $5,100, $4,400, $3,700, and $6,200 — your Baseline is $3,200. That’s the number your entire budget is built on.

Why the lowest instead of the average? Because the average ($4,567 in this example) includes the good months. If you spend like you make $4,567 and then hit a $3,200 month, you’re suddenly $1,367 short. That gap is where credit card debt at ~22% APR lives. We call this the Average Income Trap — budgeting to the middle when you should be budgeting to the floor. If you can’t pay your bills on your Baseline number, you don’t have a budgeting problem; you have an income problem.

Step 2: Build Your Priority Stack

Once you have your Baseline, organize your expenses into tiers. When money comes in, you fund from the top down. If it runs out before you reach the bottom, the lower tiers wait.

Tier 1 — The Four Walls (non-negotiable): Rent/mortgage, utilities, groceries, transportation, insurance, minimum debt payments. These get funded first, every time, no exceptions. This is your Survival Number — a concept we introduced in our low-income savings guide.

Tier 2 — Financial Foundation: Emergency fund contribution, extra debt payments above the minimum, tax set-aside (if self-employed — aim for 25–30% of every payment into a separate tax account).

Tier 3 — Quality of Life: Subscriptions, dining out, entertainment, personal spending. These are the first things that flex down during a slow month.

Tier 4 — Growth: Extra investing contributions, business development, skill-building courses, savings goals beyond the emergency fund.

The key rule: Tier 1 is untouchable. Everything else flexes based on what actually came in — not what you hoped would come in. During a $3,200 month, you might only cover Tiers 1 and 2. During a $6,200 month, you fund everything and stack the surplus. If you’re funding Tier 4 while Tier 3 is empty, you’re stealing from your future self to pay for a temporary dopamine hit.

Step 3: The Income Buffer (Your Shock Absorber)

This is the single most important piece of the whole system. An Income Buffer is a separate savings account that holds 1–3 months of your Baseline expenses. Its only job is to act as a middleman between your chaotic clients and your boring bills — turning irregular income into a regular “paycheck.”

How it works:

All your income flows into the Buffer first. You then pay yourself a fixed “salary” (your Baseline Number) into your checking account every month. When you earn more than your Baseline, the surplus stays in the Buffer. When you earn less, you pull from the Buffer to cover the gap. Your checking account never knows the difference.

Example: Your Baseline is $3,200/month. In March you earn $5,100 — the extra $1,900 stays in the Buffer. In April you earn $2,800 — you pull $400 from the Buffer to hit your $3,200. Your spending stays the same both months. No panic, no credit cards, no scramble.

You aren’t “saving” this money in the traditional sense — you’re smoothing it. Think of the Buffer as a bridge across the valleys of your income. It’s different from your emergency fund. The emergency fund is for if the engine dies. The Buffer is for the normal bumps in the road.

The Skeptic’s Friction Report:

Building the Buffer takes time. If you’re living right on the edge of your Baseline already, there’s not much surplus to capture. Start small — even $200 is better than $0 when a slow week hits. The goal is eventually 1–3 months of Baseline expenses, but don’t let the perfect number stop you from starting with whatever you’ve got.

Step 4: The Payday Protocol for Variable Income

With a fixed salary, money arrives on a predictable schedule. With variable income, you need a ritual for every time money comes in. We call this the Irregular Payday Protocol.

Every time money hits your account:

1. Set aside taxes first (if self-employed). Transfer 25–30% immediately to a separate tax-only account. Do not touch this money. This is the Tax Trap Shield — and it’s non-negotiable. The IRS is your most dangerous “creditor” because they have the most enforcement power. With the 1099-K reporting threshold now at $600, the IRS has more visibility into gig and freelance income than ever. Quarterly estimated payments are due April 15, June 15, September 15, and January 15. If you wait until April to “figure it out,” you’re playing a game of chicken you will lose.

2. Fund Tier 1 (The Four Walls). Cover any upcoming bills from the Survival Number list.

3. Top off the Income Buffer. If the Buffer is below your target, send money there before anything else.

4. Fund Tiers 2–4 in order. Whatever remains flows down through the priority tiers until the money runs out for that pay period.

5. Stop. Do not fund Tier 3 or 4 expenses with money that should be covering next week’s Tier 1.

This replaces the “I’ll figure it out at the end of the month” approach. You make allocation decisions in real time, every time money arrives.

The Best Budgeting Tools for Irregular Income

| Tool | The Verdict | The Reality |

|---|---|---|

| YNAB | The master class. Only lets you budget money you actually have. | Steep learning curve — expect what we’ve called First Month Fog. $109/year (Success Tax) that pays for itself. |

| Goodbudget | Digital envelope system. Free. | Great for simplicity, but lacks deep bank automation. |

| Spreadsheet | Total control. $0 cost. | High manual friction — if you don’t update it regularly, it becomes a paperweight. |

The Surplus Protocol: What to Do With Good Months

This is where most variable-income earners get into trouble. A $6,200 month after two $3,500 months feels like a lottery win — but windfall months aren’t a lottery win. They’re fuel for your next dry spell.

When income exceeds your Baseline, run the surplus through this order:

- Fill the Income Buffer to your target level (1–3 months of Baseline)

- Catch up on Tier 2 — extra debt payments, emergency fund contributions

- Apply the Windfall Rule (from our emergency fund guide) — unexpected money goes to financial goals before discretionary spending

- Then and only then — fund Tier 3 and 4 with whatever remains

The discipline of good months is what makes bad months survivable. Every dollar you send to the Buffer or to debt during a high-income month is a dollar you don’t have to put on a credit card during a low one.

The bottom line: In 2026, stability is a luxury you build — not something your income gives you automatically. You can’t control when a client pays, but you can control the friction between that payment and your lifestyle. Build the Buffer, respect the Baseline, and stop treating good months like found money. They’re just the fuel for your next dry spell.

FAQ

Should I budget based on my average income or my lowest month?

Your lowest month. The average includes high months that may not repeat. Budgeting to your lowest month means every month works — and high months become surplus you deploy strategically.

How big should my Income Buffer be?

Aim for 1–3 months of your Baseline expenses. Start with whatever you can. This is separate from your emergency fund, which should eventually cover 3–6 months of full expenses.

I’m self-employed. How much should I set aside for taxes?

25–30% of every payment, transferred immediately to a separate account. Quarterly estimated payments are due April 15, June 15, September 15, and January 15. If you’re unsure about your exact rate, 30% is the safer default.

What if my income is so low I can barely cover Tier 1?

That’s a signal that the income itself is the problem, not the budget. A budget can only organize money that exists. If your Baseline doesn’t cover survival costs, the priority becomes increasing income — adding clients, switching gig platforms, or taking on temporary work. Our savings guide has practical starting points.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: