Best Investing Apps for Beginners 2026: Start With as Little as $1

Quick Verdict: You Really Can Start With $1

Investing used to feel out of reach. You needed thousands of dollars, paid high commissions, and had to deal with confusing platforms. In 2026, those barriers are basically gone. You can open an account with $0, buy a slice of Amazon for $1, and pay zero commissions on trades.

But here’s what most “beginner investing” articles won’t tell you: as the entry barriers fell, the friction points simply moved. The apps aren’t making money on your $1 trade — they’re making money on your uninvested cash, your data, and your tendency to overtrade. The real question isn’t whether you can afford to start. It’s which app actually puts your first dollar to work instead of using it as bait for a subscription fee.

The Quick Verdict:

- STACK: Fidelity ✅ — NerdWallet’s 2026 choice for best beginner broker. Zero commissions, no minimums, fractional shares from $1, and the only major broker with 0% expense ratio index funds. The app you’ll never outgrow.

- RUNNER UP: Robinhood — The simplest interface for your very first trade. Zero commissions, no minimums, and a 3% IRA match (with Gold) that’s the most aggressive free-money play in the industry.

- RUNNER UP: SoFi Invest — The ecosystem play. Great if you already bank with SoFi and want investing, banking, and loans all under one roof.

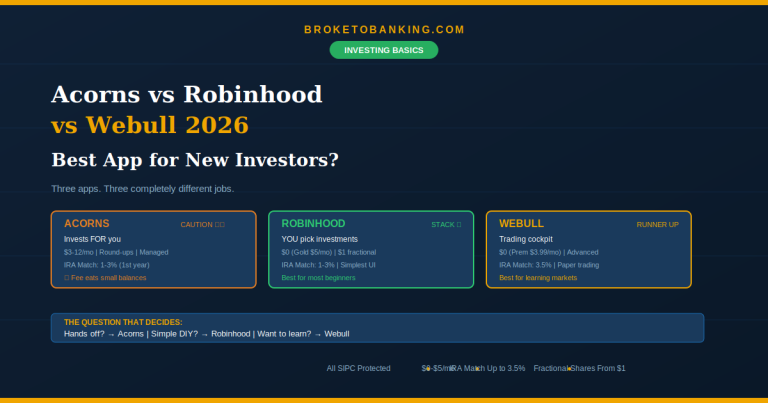

- PROCEED WITH CAUTION: Acorns ⚠️ — The round-up feature builds great habits, but $3–$12/month on a small balance is a mathematical disaster. Great concept, expensive execution.

- SKIP: Any app pushing options, crypto day-trading, or leveraged products before you’ve bought your first index fund ❌

What Actually Matters When Choosing Your First Investing App

Non-negotiable for beginners: zero or near-zero commissions on stocks and ETFs, no (or very low) account minimum, fractional shares so you can invest with $1–$5, and an interface that doesn’t make you feel dumb.

Nice to have: educational content, automated investing options, retirement accounts (Roth IRA, Traditional IRA), and a decent cash sweep for uninvested money.

Ignore: flashy stuff like crypto trading, options chains, leverage tools, or “social trading” feeds. None of that helps a beginner build real wealth. It helps the app generate revenue from your activity.

We call this the First Dollar Test: if you had exactly $1 to invest and zero experience, which app would put that dollar to work most efficiently with the least hassle and lowest cost?

Fidelity — The “Grow-Into-It” Stack

The Verdict: STACK ✅

Fidelity won NerdWallet’s 2026 award for best online broker for beginning investors, and the pick is hard to argue with. It’s one of the biggest brokerages in the country, charges zero commissions on stock and ETF trades, has no account minimum, and lets you buy fractional shares starting at $1.

| Feature | Details |

|---|---|

| Commissions | $0 on stocks and ETFs |

| Account Minimum | $0 |

| Fractional Shares | Yes, from $1 |

| Retirement Accounts | Roth IRA, Traditional IRA, SEP IRA |

| Educational Content | Extensive — articles, videos, webinars |

| SIPC Protected | Yes |

What really sets Fidelity apart is the Zero Advantage: you can buy FZROX (Fidelity ZERO Total Market Index) or FNILX (Fidelity ZERO Large Cap Index) with literally 0% management fees. Every cent of your growth stays in your pocket. No other major broker matches this. Fidelity also offers a Youth Account for teens 13–17, making it a solid family option.

The Skeptic’s Friction Report:

The app isn’t the prettiest — the interface reflects a full-service brokerage that also serves advanced traders, which can feel overwhelming at first. It won’t give you a dopamine hit when you buy a stock, which — for a long-term investor — is actually a feature, not a bug. The learning curve is steeper than Robinhood. But that trade-off gets you tools you’ll actually want as you grow. This is the app you won’t outgrow.

Robinhood — The Dopamine Trap (Use It Wisely)

The Verdict: RUNNER UP (STACK for the IRA Match)

If Fidelity is the app you grow into, Robinhood is the app that makes your first trade feel effortless. The interface is deliberately simple — almost too simple — which is exactly what a nervous beginner needs. You can download the app, open an account, and make your first trade in under five minutes.

| Feature | Details |

|---|---|

| Commissions | $0 on stocks, ETFs, options, and crypto |

| Account Minimum | $0 |

| Fractional Shares | Yes, from $1 |

| IRA Match | 1% (3% with Robinhood Gold at $5/month) |

| Educational Content | Improving — added AI-powered research tools in 2026 |

| SIPC Protected | Yes |

The IRA match is a genuine standout. With Gold ($5/month), the 3% match on up to $7,000 in Roth IRA contributions means $210 in free money annually — more than covering the $60 Gold fee. That’s the most aggressive retirement match play from any brokerage app in 2026.

The Skeptic’s Friction Report:

Here’s the honest problem: Robinhood is a Dopamine Trap. The app makes it very easy to trade frequently, buy crypto on impulse, and treat investing like a game. According to The Motley Fool, Robinhood still makes the bulk of its revenue from strategies that don’t align with proven long-term investing. The app is great for buying your first index fund. It’s dangerous if it turns you into a day trader. The skeptic’s advice: use it for the IRA match, buy a broad index fund (like VTI), and delete the app from your home screen so you aren’t tempted to “check the score” every hour.

SoFi Invest — The Ecosystem Play

The Verdict: RUNNER UP

SoFi’s pitch is simple: put your investing, banking, lending, and insurance under one roof. If you’re already using SoFi for checking and savings (which we covered in our HYSA guide), adding their investing platform is seamless.

| Feature | Details |

|---|---|

| Commissions | $0 on stocks and ETFs |

| Account Minimum | $0 (active); $50 (automated) |

| Fractional Shares | Yes, from $5 |

| Robo-Advisor | Yes, 0.25% annual fee |

| Retirement Accounts | Roth IRA, Traditional IRA, SEP IRA |

| SIPC Protected | Yes |

SoFi offers both self-directed and automated investing. The automated option builds a diversified portfolio for you based on your goals and risk tolerance — solid if you want to invest but don’t want to pick stocks yourself.

The Skeptic’s Friction Report:

SoFi’s research and educational tools are thinner than Fidelity’s. The robo-advisor fee of 0.25% is standard but not free. And the $5 minimum for fractional shares is higher than Fidelity’s or Robinhood’s $1 minimum — a small difference, but it matters when you’re starting with very little. SoFi’s strength is the ecosystem convenience, not the investing platform itself.

Acorns — The Micro-Investing Tax

The Verdict: PROCEED WITH CAUTION ⚠️

Acorns is built around one clever idea: round up every purchase to the nearest dollar and invest the spare change. Buy coffee for $4.35, and Acorns invests $0.65 automatically. It’s a smart behavioral trick that turns everyday spending into investing.

The problem is the pricing.

| Feature | Details |

|---|---|

| Commissions | None (managed portfolios) |

| Plans | Bronze $3/mo, Silver $6/mo, Gold $12/mo |

| Minimum to Invest | $5 |

| Round-Ups | Yes (signature feature) |

| IRA Match | 1% (Silver), 3% (Gold) — first year |

| SIPC Protected | Yes |

At $3/month, Acorns costs $36/year. If your balance is $500, that’s an effective fee of 7.2% — no investment on earth reliably returns 7.2% after fees. According to NerdWallet, you’d need approximately $14,400 in your account to bring the effective fee down to the industry-standard 0.25%. This is the Micro-Investing Tax: the smaller your balance, the higher the percentage that goes to fees.

The Skeptic’s Friction Report:

The Exit Fee Trap: Acorns charges $35 per ETF to transfer your portfolio to another broker. With 5–7 ETFs in a typical portfolio, that’s $175–$245 to leave. Plan your exit strategy before you enter. The only way to make the math work: deposit at least $100/month on top of your round-ups to dilute the fee impact quickly — or use Acorns to build the habit, then graduate to Fidelity once you’ve proven to yourself that investing isn’t scary.

The Priority Order for Your First Investing App

| Priority | App | Best For | Cost | Minimum |

|---|---|---|---|---|

| 1st | Fidelity | Full-featured + education | $0 | $0 |

| 2nd | Robinhood | Simplest first trade + IRA match | $0 (Gold: $5/mo) | $0 |

| 3rd | SoFi Invest | All-in-one financial platform | $0 (robo: 0.25%) | $0 |

| 4th | Acorns | Building the investing habit | $3–$12/mo | $5 |

What to Buy First: The One-Fund Start

Don’t try to find the next Nvidia. You’re a researcher, not a gambler.

Open a Roth IRA if your app offers one. We explained why in our Roth IRA guide — the tax-free growth is what we called the Compound Interest Cheat Code. Every dollar you invest in a Roth IRA at age 25 has decades to grow tax-free.

Buy a broad market index fund or ETF. VTI (Vanguard Total Stock Market) or VOO (Vanguard S&P 500) gives you instant diversification across hundreds of companies in one purchase. At Fidelity, FZROX gives you the same exposure with a 0% expense ratio.

Automate $25/month. Consistency beats intensity. Set it and forget it. This is the One-Fund Start: one fund, one automatic deposit, and time does the heavy lifting. You can add complexity later. But one well-chosen index fund is better than analysis paralysis that keeps your money in cash.

FAQ

How much money do I need to start investing?

As little as $1. All the apps on this list let you buy fractional shares. The bigger barrier isn’t the minimum — it’s deciding to start.

Is my money safe in an investing app?

Your brokerage account is protected by SIPC for up to $500,000 if the brokerage fails. This does not protect against market losses — your investments can go down. But your account itself is protected.

Should I use a robo-advisor or pick my own investments?

If you have zero investing knowledge and want to start immediately, a robo-advisor builds a diversified portfolio for you. If you’re willing to spend 20 minutes learning what an index fund is, buying one yourself at Fidelity or Robinhood costs less and gives you more control.

What’s the difference between a brokerage account and a Roth IRA?

A brokerage account has no tax advantages — you pay taxes on gains when you sell. A Roth IRA lets your investments grow tax-free, and you pay no taxes on withdrawals in retirement. If you’re under the income limit, a Roth IRA should be your first investing account. See our full Roth IRA breakdown.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: