What Is an HSA? The Triple Tax Advantage Most People Miss (2026)

Quick Verdict: It’s the Most Tax-Advantaged Account in America — And Most People Treat It Like a Pharmacy Coupon

We’ve covered 401(k)s, Roth IRAs, and the full Money Sequence. But there’s one account that feels like a glitch in the simulation: the Health Savings Account (HSA).

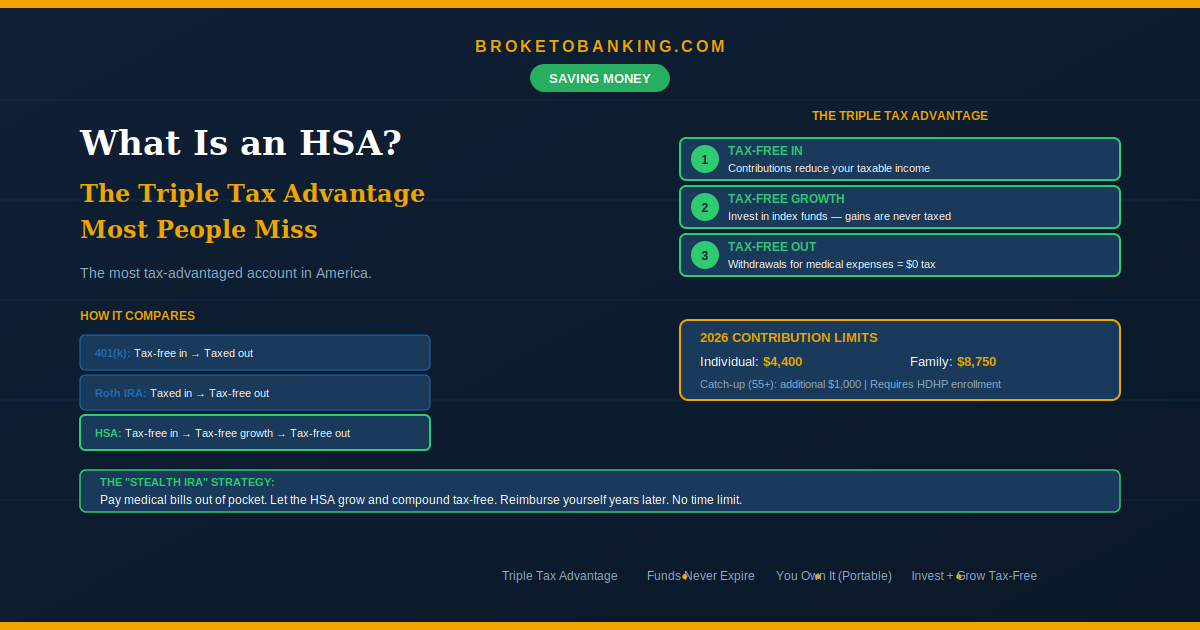

A 401(k) gives you a tax break going in but taxes you coming out. A Roth IRA taxes you going in but lets you withdraw tax-free. An HSA does all three: tax-free contributions, tax-free growth, and tax-free withdrawals for medical expenses. No other account in the U.S. tax code gets this treatment. It makes a Roth IRA look like a Runner Up.

Most people treat their HSA like a glorified coupon for the pharmacy — put money in, get a copay, spend it. That’s fine. But they’re missing the fact that the HSA is arguably the most powerful wealth-building tool in the tax code.

The Quick Verdict:

- STACK: Max your HSA if you’re eligible ✅ — The triple tax break is mathematically superior to unmatched 401(k) contributions.

- STACK: Invest the balance in index funds ✅ — If your HSA is sitting in a 0.01% cash account, you’re paying a Laziness Tax to your bank.

- RUNNER UP: Pay medical bills out of pocket and let the HSA grow — Save receipts for tax-free reimbursement years later.

- SKIP: Treating it like an FSA ❌ — FSAs are “use it or lose it.” HSAs are “keep it forever.”

How the Triple Tax Advantage Works

Tax-Free In: Every dollar you contribute lowers your taxable income. If you contribute through payroll, you also dodge Social Security and Medicare taxes (FICA) — a benefit even your 401(k) can’t match.

Tax-Free Growth: Invest in index funds inside your HSA and all gains grow completely tax-free. No capital gains tax. No dividend tax. The IRS doesn’t touch it.

Tax-Free Out: Withdrawals for qualified medical expenses — doctor visits, prescriptions, dental, vision, mental health, copays, deductibles — come out completely tax-free.

After age 65: The HSA becomes a “Super IRA.” Medical withdrawals stay tax-free. Non-medical withdrawals are taxed as regular income but with no penalty — exactly like a traditional IRA. It’s the ultimate retirement safety net.

The 2026 Numbers

| Individual | Family | |

|---|---|---|

| Contribution limit | $4,400 | $8,750 |

| Catch-up (age 55+) | +$1,000 | +$1,000 |

| HDHP min deductible | $1,700 | $3,400 |

| HDHP max out-of-pocket | $8,500 | $17,000 |

Employer contributions count toward your limit. If they put in $1,000, you can contribute up to $3,400 individually.

What’s new in 2026: All Bronze and Catastrophic plans on the Healthcare.gov marketplace are now HSA-eligible, opening the door for millions of self-employed people. Additionally, Direct Primary Care (DPC) memberships — monthly fees for unlimited doctor access — are now qualified HSA expenses.

Who’s Eligible?

You need to be enrolled in a High Deductible Health Plan (HDHP) — in 2026, that means a plan with at least a $1,700 individual or $3,400 family deductible. You also can’t be on Medicare, can’t be claimed as a dependent, and can’t have other non-HDHP health coverage (a limited-purpose FSA for dental/vision is okay).

Don’t let the “high deductible” name scare you. Many people come out ahead because of lower premiums + the HSA’s triple tax advantage + potential employer contributions. Run the actual math during open enrollment.

The “Stealth IRA” Strategy (Why Most People Use Their HSA Wrong)

The common mistake: treating it like a checking account for current medical bills. You get the upfront tax break, but you miss years of tax-free compounding.

The smarter play: Once you have your Financial Armor ($1,000 emergency fund) and high-interest debt is gone, stop spending your HSA. Pay your doctor visits and prescriptions from your regular checking account. Save every receipt — digitize everything, photo every EOB.

Let the HSA sit in a Total Market Index Fund for 20 years. In 2046, you can reimburse yourself for that 2026 doctor visit tax-free — while the original $200 has compounded into roughly $800. There’s no time limit on reimbursement. That’s tax-free cash you’re storing for the future.

If money is tight right now: Use your HSA for what it’s designed for — tax-free medical spending. The Stealth IRA strategy works best once your financial foundation is solid.

HSA vs. FSA — Don’t Mix Them Up

| Feature | HSA | FSA |

|---|---|---|

| Rollover | Never expires — stays for life | Use it or lose it |

| Ownership | You own it — portable if you change jobs | Employer-owned — you lose it if you leave |

| Investing | Yes — buy index funds | No — sits in cash |

| Eligibility | Requires HDHP | Available with most employer plans |

| Best for | Long-term wealth building | Short-term medical spending |

If you have access to both, the HSA is almost always the stronger long-term choice.

Where the HSA Fits in the Money Sequence

- 401(k) match (guaranteed return)

- Emergency fund ($1,000 buffer)

- High-interest debt payoff

- HSA (if eligible) — triple tax advantage beats unmatched 401(k) contributions

- Roth IRA ($7,500 limit)

- Additional 401(k) contributions toward 10–15%

How to Get Started

1. Check your plan. If your deductible is at least $1,700 (self) or $3,400 (family), you likely qualify.

2. Open an account. Your employer may offer one. If not, Fidelity has $0 fees and excellent index fund investing options.

3. Automate contributions. Payroll deductions or a recurring monthly transfer.

4. The Sweep. Once your balance hits the custodian’s investment threshold (usually $1,000–$2,000), sweep every dollar above that into a broad index fund — the same VTI, VOO, or FZROX approach from every other investing guide on this site.

5. Digitize everything. Photo every receipt and EOB. Even if you don’t reimburse yourself for a decade, that’s tax-free cash stored for your future self.

The HSA is a wealth-building machine disguised as a boring insurance benefit. If you’re eligible and you aren’t using it, you’re leaving the Triple Tax Advantage on the table.

FAQ

Can I open an HSA without an employer?

Yes — as long as you have a qualifying HDHP. Fidelity and Lively both offer individual HSAs with investing options.

What counts as a qualified medical expense?

Doctor visits, prescriptions, dental, vision, mental health, copays, deductibles, and many OTC medications. Full list in IRS Publication 502.

What if I withdraw for non-medical stuff?

Before 65: income tax + 20% penalty. After 65: income tax only (no penalty) — making it work like a traditional IRA.

Should I invest or keep it in cash?

Invest it — especially if you’re young. Letting HSA funds sit in cash is the same Cash Drag Warning from our Roth IRA guide. Let the money work.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: