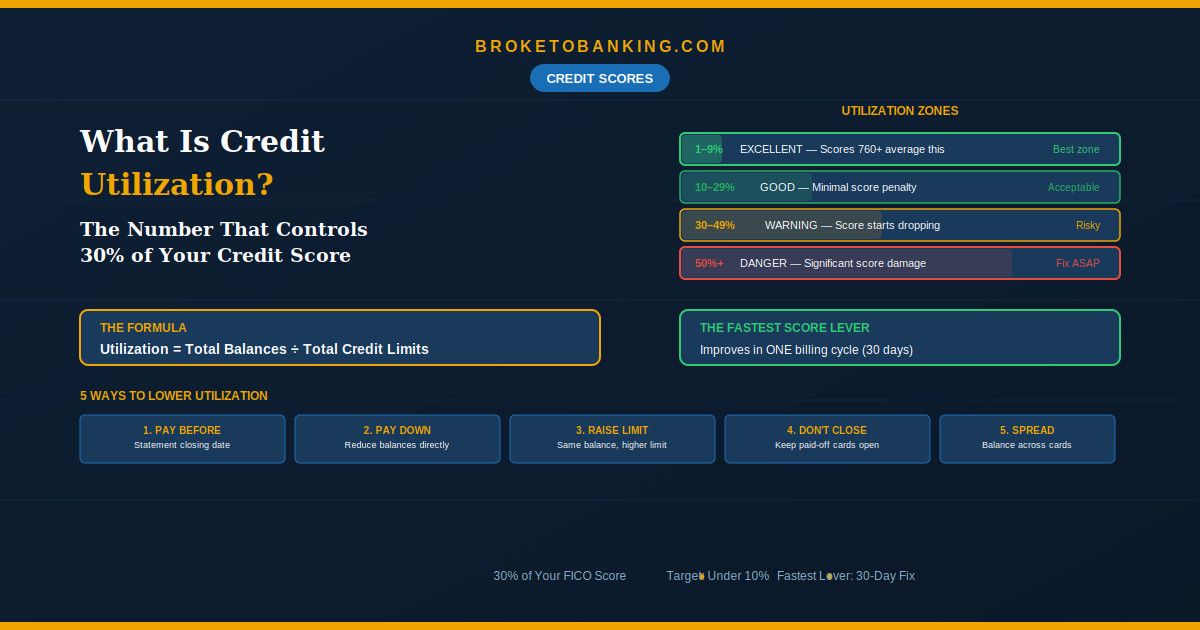

What Is Credit Utilization? (The Number That Controls 30% of Your Credit Score)

Quick Verdict: It’s How Much Credit You’re Using — And It Moves Your Score Faster Than Anything Else

If payment history is the foundation of your credit house, credit utilization is the thermostat. It controls the “temperature” of your score — roughly 30% of your FICO calculation — and unlike a late payment that haunts you for 7 years, utilization is recalculated every billing cycle. Fix it today, and your score can jump in 30 days.

Here’s the formula:

Credit Utilization = Total Credit Card Balances ÷ Total Credit Limits

$2,000 balance on $10,000 total limits = 20% utilization. $8,000 on that same $10,000 = 80% — and your score is paying for it.

The common advice is “keep it under 30%.” That’s the floor, not the target. People with scores above 760 typically stay under 10%. Those with perfect 850s hover around 4–7%. Lower is always better — though 0% across every card can be slightly less favorable than 1–9%, because scoring models like to see some responsible usage.

The Quick Verdict:

- STACK: Keep utilization under 10% ✅ — The fastest way to break into the 740+ club.

- STACK: Pay before the statement closing date, not just the due date ✅ — The reported balance is what the bureau sees.

- RUNNER UP: Request a credit limit increase without spending more — Instant math improvement.

- SKIP: Closing paid-off credit cards ❌ — A self-inflicted wound that spikes your utilization overnight.

Why It Matters So Much (The 2026 Update)

High utilization signals financial stress to lenders. Even if you plan to pay it off next month, a high percentage makes you look overextended. That feeds the Invisible Score Tax from our credit score guide — lower scores → higher interest rates on everything.

The 2026 reality: Major lenders are increasingly adopting FICO 10T and VantageScore 4.0, which use Trended Data — they look at your utilization behavior over the last 24 months, not just a single snapshot. The algorithm now distinguishes between a “Transactor” (charges $3,000 and pays in full every month) and a “Revolver” (carries a $3,000 balance month after month). If you’re a Revolver, the newer models view you as higher risk even if your utilization is technically under 30%.

This is the Trended Data Strategy we mentioned in our credit building guide: consistent full-payment patterns signal lower risk to FICO 10T. Paying in full every month builds a track record that the old models couldn’t see.

The 2026 Benchmarks

| Score Range | Average Utilization |

|---|---|

| Exceptional (800+) | ~7% |

| Very Good (740–799) | ~14% |

| Good (670–739) | ~28% |

| Fair (580–669) | ~45% |

The national average is roughly 28%. If you’re above that, you have the most room for improvement — and it’s the fastest lever available.

Both Numbers Matter: Overall and Per-Card

FICO looks at your overall utilization (total balances ÷ total limits) and per-card utilization on each individual account. One maxed-out card hurts you even if the overall number looks fine.

| Card | Balance | Limit | Per-Card Utilization |

|---|---|---|---|

| Card A | $2,800 | $3,000 | 93% — score damage |

| Card B | $200 | $5,000 | 4% |

| Card C | $0 | $2,000 | 0% |

| Total | $3,000 | $10,000 | 30% overall |

30% overall seems okay. But Card A at 93% is a red flag. Spreading balances across cards — rather than maxing one — reduces per-card utilization even if the total stays the same.

5 Ways to Lower Your Utilization

1. Pay Before the Statement Closing Date

This is the trick most people miss. Your issuer reports the balance on your statement closing date — not your due date. You could charge $3,000 and pay it all by the due date, but if the statement already closed, the bureau sees a $3,000 balance.

The fix: Pay down your balance a few days before your statement closes. Even better: pay twice a month — once mid-cycle and once before closing. This keeps your trended data looking pristine under the newer scoring models.

2. Pay Down Existing Balances

Every dollar paid reduces the numerator. Dropping from 30% to 5% on a card can add 20–40 points in the next reporting cycle. This connects directly to our debt payoff strategy — killing credit card debt improves both Interest Gravity and utilization simultaneously.

3. Request a Credit Limit Increase

Same balance ÷ higher limit = lower utilization instantly. $1,000 balance on a $2,000 limit is 50%. Get that limit raised to $5,000 and it drops to 20% without paying a penny.

Many issuers in 2026 use soft pulls for limit increase requests — no score impact. Always ask whether it’s a soft or hard pull before requesting. Most allow a request every 6–12 months through the app.

Critical: A higher limit is a tool, not an invitation to spend more.

4. Don’t Kill the Old Growth

When you pay off a card, don’t close it. Closing an account nukes that available credit from your total limit, spiking your utilization. Unless it has a predatory annual fee, keep it in a drawer and put one small subscription on it to stay active. This is the Old Growth Bonus from our credit score guide — it helps both utilization and credit age.

5. Audit Your BNPL Usage

As of 2026, Buy Now Pay Later plans from Affirm, Klarna, and others are being reported to major bureaus. While they don’t always count toward revolving utilization, they do count toward your total “Amounts Owed” — and too many active BNPL plans can signal financial stress to FICO 10T. If you have BNPL activity, check your credit report to see how it’s showing up.

The Timing Trick for Major Applications

Planning to buy a house or car in the next 2–3 months?

30 days before applying: Pay all balances down to under 10%. Ideally near zero, except one card with a small balance (1–5%).

Let the new balance get reported — wait for your next statement to close.

Pull your credit report to confirm the updated numbers.

Then apply.

This one-cycle move can boost your score 20–50 points and save you thousands on a mortgage rate. Totally free.

FAQ

What’s the ideal utilization?

Under 10% for the best impact. Under 30% avoids major damage. Exceptional scores average around 7%.

Does it matter if I pay in full every month?

Yes — because of the statement closing date. Charge what you want, but pay before the statement closes so the bureau sees a low balance. Under the newer FICO 10T model, your consistent pay-in-full pattern (Transactor behavior) is also tracked and rewarded.

Should I carry a balance for “momentum”?

No. This is a myth. You never need to pay interest to build credit. A small reported balance (1–9%) is fine, and you can achieve it by letting a small charge hit your statement and paying in full by the due date.

How fast will I see improvement?

One billing cycle — typically 30 days. Utilization is the fastest-moving component of your credit score.

The bottom line: Credit utilization is a game of math and timing. By paying before your statement closes and keeping your trended data showing consistent low balances, you’re telling the algorithm exactly what it wants to hear: you have access to credit, but you don’t need it.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: