How Much Emergency Fund Do You Actually Need? (The Real Number, Not the Generic Advice)

Quick Verdict: It Depends on Your Life — Not a One-Size-Fits-All Slogan

“Save 3–6 months of expenses” is the most repeated advice in personal finance — and also the least useful. A dual-income couple with stable jobs and no kids doesn’t need the same safety net as a single parent freelancing with a mortgage. Telling both groups the same number is like handing everyone a medium t-shirt and calling it a day.

We built the $1,000 Financial Armor starter in Post #4 — that was Step 2 of the Money Sequence. This guide is about calculating your real number and building toward it without getting paralyzed by the size of the goal.

The Quick Verdict:

- STACK: Calculate your actual Survival Number — essentials only ✅ — Not your full spending. The bare minimum to keep the lights on.

- STACK: Match months to your real risk profile ✅ — Stable dual income = 3 months. Single income = 6. Freelance = 9.

- RUNNER UP: Keep it in a HYSA earning 4%+ — Boring money is finally getting paid in 2026.

- SKIP: Investing your emergency fund in stocks ❌ — Don’t gamble with your foundation.

Step 1: Calculate Your Survival Number

Your emergency fund isn’t based on your full monthly spending. It’s based on your Survival Number — the bare-minimum essentials you’d still pay if income stopped tomorrow. Strip your budget down to the studs.

Include: Rent/mortgage, utilities, groceries (the beans-and-rice version, not the Whole Foods version), insurance, minimum debt payments, transportation, phone, prescriptions, childcare.

Exclude: Dining out, subscriptions, entertainment, shopping, hobbies, travel — anything you’d cut immediately in a real crisis.

Example:

| Essential Expense | Monthly Cost |

|---|---|

| Rent | $1,200 |

| Utilities | $150 |

| Groceries | $300 |

| Car payment + insurance | $450 |

| Health insurance | $200 |

| Phone | $75 |

| Minimum debt payments | $116 |

| Gas | $100 |

| Survival Number | $2,591 |

If your total spending is $3,400 but your Survival Number is $2,591, that $800 gap is your Efficiency Margin — proof that your emergency fund target is smaller and more achievable than you thought.

Step 2: Choose Your Months (Based on Risk, Not a Guess)

| Your Situation | Target Months | Why |

|---|---|---|

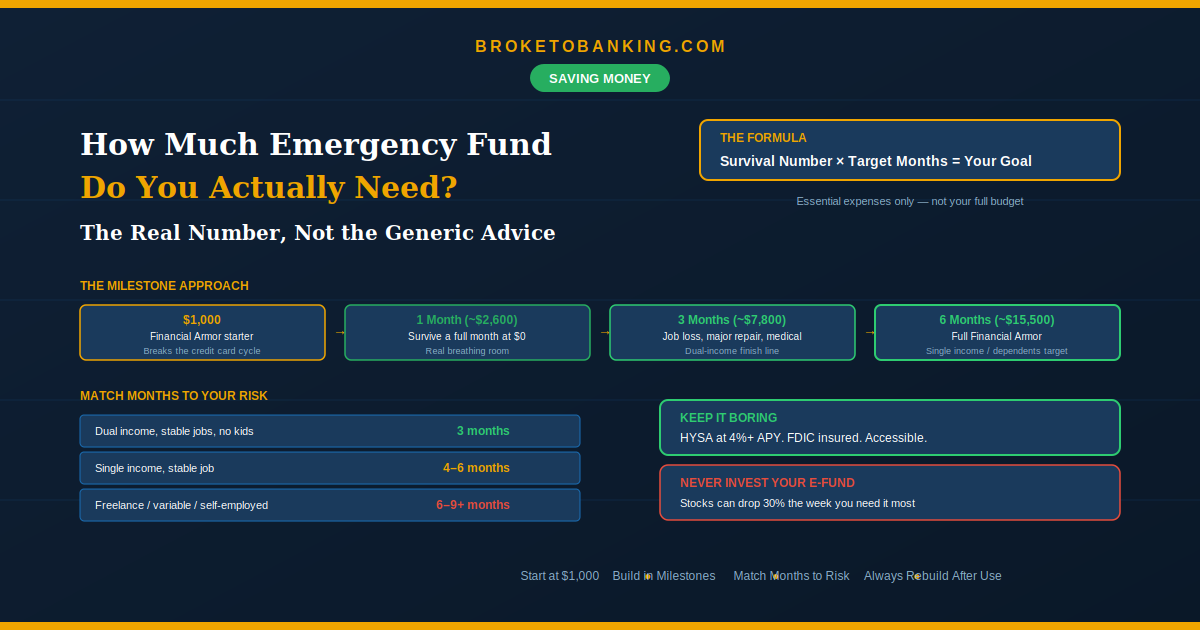

| Dual income, stable jobs, no kids | 3 months | Natural hedge — one income can carry temporarily |

| Single income, stable job | 4–6 months | You’re the only engine. If it stalls, you need time for a full reboot. |

| Single income with dependents | 6 months | More people depending on you = higher stakes |

| Freelance / variable income | 6–9 months | Income gaps are a feature, not a bug |

| High fixed costs / kids / self-employed | 9–12 months | Longest recovery time + quarterly tax obligations |

The 2026 reality: The average professional job search runs 3–5 months. For workers over 45 or in specialized fields, it often exceeds 6–8 months. Your target should cover how long it would realistically take to replace your income, not the best-case scenario.

Step 3: Do the Math

Emergency Fund Target = Survival Number × Target Months

Using the $2,591 example:

- 3 months: $7,773

- 6 months: $15,546

- 9 months: $23,319

For our target reader (single income, stable job), a 4–6 month fund of roughly $10,000–$15,500 is the realistic goal.

The Milestone Strategy (Don’t Stare at the Mountain)

Big numbers paralyze people into doing nothing. Look at the trail markers instead:

Milestone 1: $1,000 — “The Buffer” The Financial Armor starter. Covers most small emergencies and breaks the cycle of putting surprises on a 22% credit card.

Milestone 2: 1 Month (~$2,600) — “Breathing Room” You can survive a full month with zero income. That’s real stability.

Milestone 3: 3 Months (~$7,800) — “Security” You can weather a standard job transition, a major car repair, or a medical emergency without touching a credit card. For stable dual-income households, this may be your finish line.

Milestone 4: 6 Months (~$15,500) — “Freedom” Full Financial Armor. You can walk away from a toxic job, handle a serious medical event, or survive a layoff without financial panic. For single-income and dependent-supporting households, this is the target.

Every milestone is a win. Celebrate it, then keep building.

Where to Keep It (Boring = Correct)

High-yield savings account. Separate from checking, FDIC insured, accessible in 1–2 business days. In May 2026, top HYSAs are paying 4.0–4.5% APY. A $15,000 emergency fund at 4.5% earns roughly $675/year in interest — a “safety bonus” just for being responsible. We covered the best options in our HYSA guide.

Why not invest it? Because emergencies don’t wait for the market to recover. A 30% drop the same week you lose your job turns your safety net into a financial trap — and the rest goes on a credit card at 22% APR.

How to Build It (Without Pausing Everything Else)

The Money Sequence handles the timing:

Phase 1 (during debt payoff): Build to $1,000 first — before attacking credit cards. Without this buffer, every emergency resets your progress.

Phase 2 (after high-interest debt is gone): Redirect former debt payments to the emergency fund. $300/month builds from $1,000 to $7,800 in about 23 months.

Phase 3 (simultaneous with investing): Once you hit 3 months, split savings between finishing the fund and funding your Roth IRA.

Accelerators: Tax refunds (~$3,100 average in 2026), bonuses, Liquidation Sprint income, side hustle cash. And automate it — willpower is a lie. If you try to manually save, you’ll spend it on a “great deal” at the mall. Use the Ghost Paycheck: move it to a separate HYSA the day you get paid. If you don’t see it, you don’t spend it.

The Replacement Rule (Non-Negotiable)

When you use the fund — and you will — rebuild it immediately. The Replacement Protocol from our earlier posts applies: next available dollars go to replenishing before returning to normal spending or investing. An emergency fund that gets used and never rebuilt is a one-time trick. One that gets rebuilt every time is a permanent system. When the emergency inevitably hits, you won’t even flinch.

FAQ

Emergency fund or debt first?

Both. $1,000 first (Financial Armor), then attack high-interest debt. The buffer stops emergencies from becoming new credit card debt during your payoff.

Does it include sinking funds?

No. Emergency fund = genuine surprises (job loss, medical, essential repairs). Predictable irregular expenses (holidays, car maintenance) get their own Sinking Fund.

What counts as an emergency?

Job loss, unexpected medical bills, essential car/home repairs. Not vacations, sales, or “opportunities.” Be strict.

I can’t save 6 months. Is it pointless?

$1,000 covers most small emergencies. One month covers a lot more. Every dollar in the fund is a dollar that doesn’t go on a 22% credit card. Partial protection is infinitely better than zero.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: