How to Lower Your Monthly Bills in 2026 (Save $200+ Without Changing Your Lifestyle)

Quick Verdict: You’re Overpaying Because You Haven’t Asked

Most service providers — internet, phone, insurance, even your gym — count on one thing: that you’ll never call. They rely on Consumer Inertia, the quiet habit of paying every month without questioning the price. Meanwhile they quietly sunset your promotional rate and replace it with a “standard” one that’s 30% higher. The new customer signing up next to you? Still getting that promo rate for the exact same service.

This is the Loyalty Tax we introduced in Post #3 — the surcharge you pay for being a long-time customer who never complains. Every provider has retention pricing available for people who ask. Most people never ask.

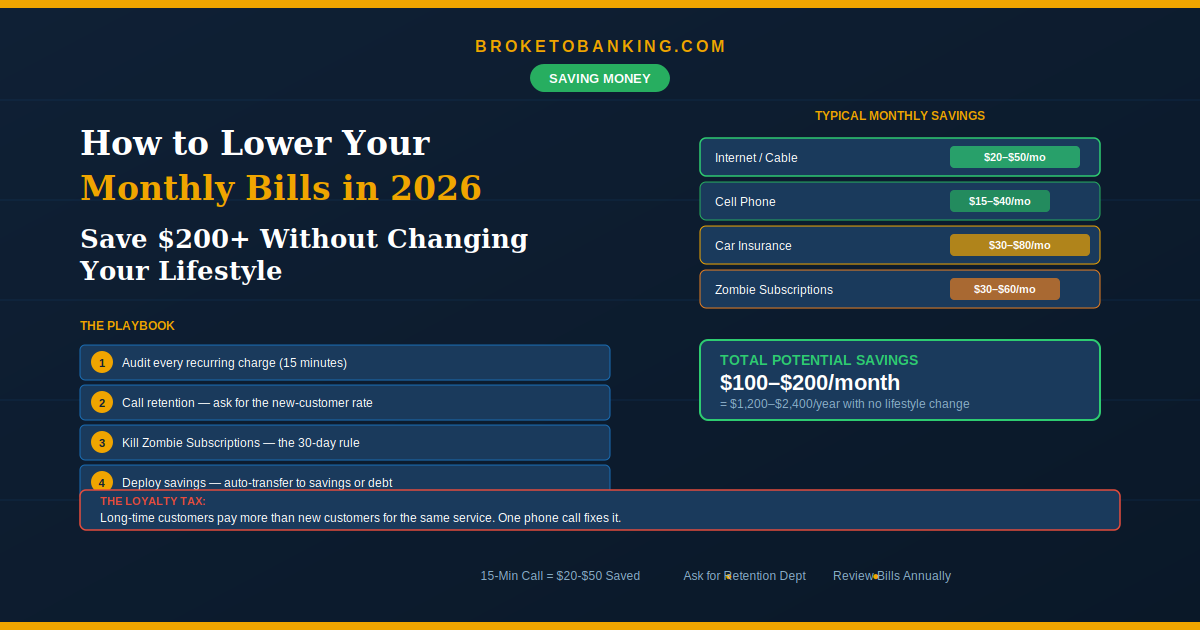

A single 15–20 minute phone call to your internet provider can save you $20–$50/month. Do that across 3–4 recurring bills, and you’re looking at $100–$200/month — or $1,200–$2,400/year — without cutting a single thing you actually use. If you value your time at $30/hour, spending one hour to save $1,200/year is like getting paid $1,200/hour for that one hour of work. It’s the highest-ROI activity in your financial life.

The Quick Verdict:

- STACK: Negotiate internet, phone, and insurance — these have the most margin to give ✅

- STACK: Kill Zombie Subscriptions — the ones you forgot about ✅

- RUNNER UP: Switch to lower-tier plans or MVNOs where you’re paying for a brand name, not better service

- RUNNER UP: Stop renting equipment — buy your own modem/router

- SKIP: Paying a bill negotiation service 40% of your savings for a conversation you can have yourself ❌

The Bill Audit: Start Here (15 Minutes)

You can’t fix a leak you can’t find. Pull up your bank app and list every recurring charge from the last 30 days.

| Bill | Current Monthly Cost | Last Time You Reviewed It |

|---|---|---|

| Internet | $85 | Never? |

| Cell Phone | $75 | 2 years ago? |

| Car Insurance | $160 | At renewal? |

| Streaming (all) | $45 | When you signed up? |

| Gym | $30 | Years ago? |

| Other subscriptions | $?? | $?? |

Most people discover $150–$300/month in recurring charges they’ve never questioned. That’s your starting point.

The Big Three: Where the Real Savings Live

Internet / Cable — The Easiest Win

Typical savings: $20–$50/month

Internet providers raise rates every year, counting on the fact that you won’t notice. Your $59 promo plan is probably $85–$100 now. In 2026, with 5G home internet emerging as a real competitor, cable providers are more willing to negotiate than ever.

The move: Call and ask for the retention or cancellations department — front-line reps can’t give you the best deals. Use this:

“Hi, I’ve been a customer for [X years] and I’ve always paid on time. My bill has gone up to [$X] and I see [competitor] offering 500Mbps for [$Y] in my area. I’d like to stay, but I need my rate brought closer to the new-customer price. What can you do?”

If they offer nothing, say you’d like to cancel. This usually triggers a real retention offer.

Bonus: If you’re renting a modem or router ($10–$15/month), buy your own for $80–$100. Pays for itself in 7 months and saves $120–$180/year forever.

Cell Phone — The MVNO Pivot

Typical savings: $15–$50/month

If you’re on a Big Three carrier (AT&T, Verizon, T-Mobile) paying $75+/month for a single line, you’re paying for Premium Brand Anxiety — the carrier’s name, not better service. MVNOs (Mobile Virtual Network Operators) use the exact same towers for a fraction of the cost.

The 2026 winners: Visible ($25/month, Verizon’s network), Mint Mobile ($15/month, T-Mobile’s network), US Mobile ($10–$25/month, choose your network). Switching one line can save $600–$1,200/year.

The move: Check your actual data usage over the last 3 months. If you’re consistently under 10GB and mostly on WiFi, you’re overpaying for unlimited. A 5GB MVNO plan at $15–$25/month delivers the same experience for most people.

Car Insurance — The Annual Shopping Ritual

Typical savings: $30–$80/month

Insurance premiums are wildly inconsistent between companies. Two insurers can offer the exact same coverage at dramatically different prices. And drivers with poor credit pay up to 105% more (another reason your credit score matters).

The move: Get 3–4 quotes from competitors at least once a year. Bring the lowest to your current provider and ask them to match it. If they won’t, switch. Also review your coverage — if you’re driving a car worth less than $5,000, dropping comprehensive and collision can save $50+/month.

Low-mileage tip: If you drive under 7,000 miles a year, look into pay-per-mile insurance. You could save roughly 40% simply by not paying for miles you don’t drive.

The Subscription Purge: Kill the Zombies

We’ve talked about Zombie Subscriptions across multiple posts. Here’s the systematic kill:

Check your phone’s subscription settings. On iPhone: Settings → Apple ID → Subscriptions. On Android: Play Store → Payments & Subscriptions. Most people find at least one app charging $9.99/month for something they haven’t opened in a year.

The 30-Day Rule: If you haven’t used a subscription in 30 days, cancel it. You can always re-subscribe.

The Seasonality Rule: Stop paying for 5 streaming services simultaneously. Rotate them — Netflix for winter binge season, cancel, HBO for spring premieres, cancel, etc. You’ll watch everything you want and save roughly $400/year without missing a single show.

Common zombies: secondary streaming services ($8–$17/month each), unused gym memberships ($20–$50/month), app auto-renewals ($5–$15/month each), expired free trials ($10–$30/month). Most people find $30–$60/month — that’s $360–$720/year delivering zero value.

The Downgrade Strategy: Pay for What You Actually Use

Streaming: Do you need 4K Premium Netflix at $23/month, or would the $7 ad-supported tier work? That’s $192/year saved for a few more ads.

Insurance deductibles: Raising your deductible from $250 to $1,000 usually lowers your premium — but only do this if you have the Financial Armor to cover it.

The Savings Deployment Plan (The Most Important Step)

If you save $200/month and leave it in your checking account, it’ll vanish into lifestyle creep. That’s Checking Account Gravity from Post #12.

The moment you confirm a bill reduction, set up an automatic transfer for that exact amount to your HYSA or debt payoff account. $200/month saved and deployed becomes:

- $2,400/year toward your emergency fund or debt payoff

- $2,400/year invested in a Roth IRA at historical market returns could grow to $35,000+ over 10 years

You “found” that money just by making a few phone calls. The savings only count if they go somewhere.

FAQ

Which bills are easiest to negotiate?

Internet/cable is the easiest — most competition, widest pricing gap between new and loyal customers. Car insurance is second. Cell phone is more about switching plans than negotiating. Utilities are generally non-negotiable but can be reduced by lowering usage.

Should I use a bill negotiation service?

Services like Billshark and Rocket Money take 30–60% of your first year’s savings. Everything they do — calling retention, citing competitors, asking for loyalty discounts — you can do yourself in 20 minutes for free. These companies are not your friends. They’re businesses designed to take a cut of savings you could keep entirely. If you have a phone and 20 minutes, keep your money.

What if they say no?

Ask for a supervisor or the retention department specifically. If they still won’t budge, say “I’d like to cancel.” If they truly won’t negotiate, switch to the competitor whose rate you researched. The leverage only works if you’re willing to follow through.

How often should I do this?

At least once a year. Set a calendar reminder. Promotional rates expire, prices creep up, and better deals appear. Think of it as a one-hour annual checkup that pays you $1,000+.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: