What Is a Good Credit Score? (And Why It Costs You Money Every Day)

Quick Verdict: Your Score Is a Daily Price Tag

A credit score is a three-digit number between 300 and 850 that tells lenders how likely you are to pay back money you borrow. That’s the textbook answer. Here’s the real one: your credit score is a price tag that follows you everywhere, and most people have no idea how much it’s quietly costing them.

A lower score doesn’t just mean you might get denied for a credit card. It means you pay more for your mortgage, more for your car loan, more for your car insurance, and sometimes more for your apartment security deposit. We call this the Invisible Score Tax — a real-time surcharge on nearly every major financial transaction in your life. It’s completely invisible until you see what someone with a better score is paying for the exact same thing.

According to FICO data, the difference between the best and worst credit score tiers on a $400,000, 30-year mortgage is roughly $165/month — about $59,000 in extra interest over the life of the loan. Same house. Same lender. Different score. Different price. In a 2026 interest rate environment, the penalty for a low score is more brutal than it was five years ago.

The Quick Verdict:

- STACK: Know your score and check it for free ✅ — You can’t fix what you can’t see. Most banks now show your FICO score for free.

- STACK: Understand the five factors that control it ✅ — Your score isn’t random. It’s a formula, and once you know the formula, you can work it in your favor.

- RUNNER UP: Aim for 740+ for the best rates — You don’t need a perfect 850. The real savings unlock around 740.

- SKIP: Paying for credit monitoring or “score repair” services ❌ — Everything they do (disputing errors, sending letters), you can do for free. Don’t pay a monthly fee for automated letters you could write yourself.

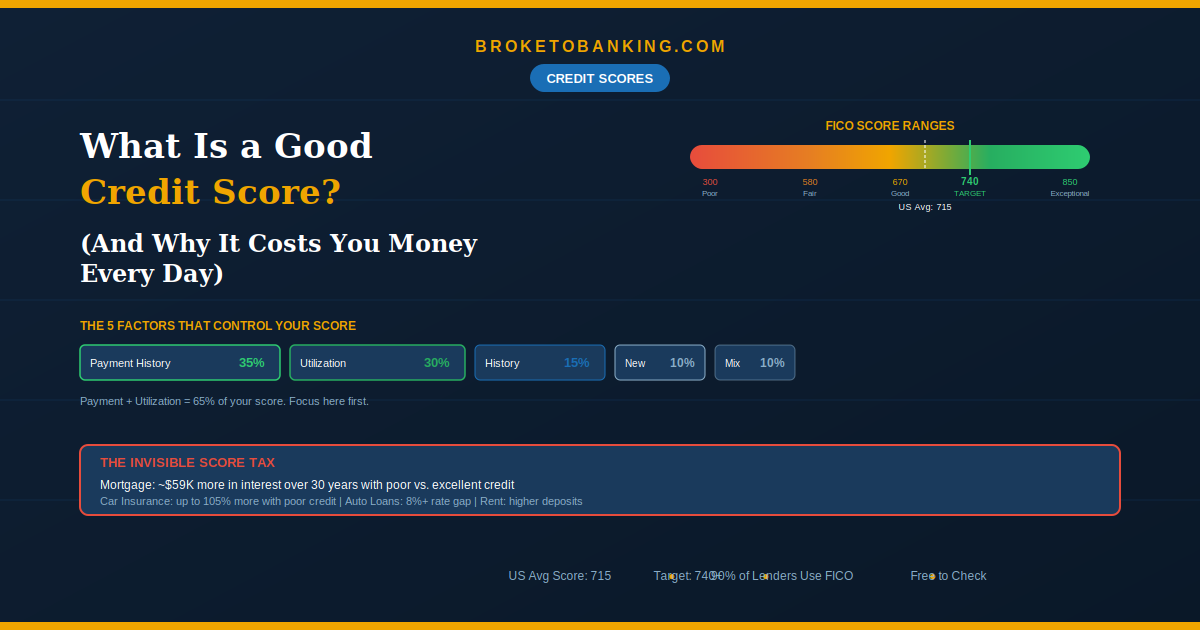

The Credit Score Ranges (Where Do You Stand?)

About 90% of top lenders use FICO scores. Here’s how they break them down:

| Range | Category | The 2026 Reality |

|---|---|---|

| 800–850 | Exceptional | Best rates on everything. You’re the lender’s dream customer. |

| 740–799 | Very Good | The practical sweet spot. You get nearly the same rates as the 800s. |

| 670–739 | Good | Above average. You’ll qualify for most things with decent terms. |

| 580–669 | Fair | Below average. You’re paying a heavy Invisible Score Tax on every loan. |

| 300–579 | Poor | Limited options. High rates. Many applications denied. Likely locked out of traditional banking. |

The average FICO score in the U.S. is approximately 715 — right in the “Good” range, but still below the 740 threshold where the best rates kick in.

The important thing to understand: you don’t need an 850. The real financial wins — lowest mortgage rates, best credit card offers, cheapest insurance — start around 740. Getting from 670 to 740 will save you far more money over your lifetime than going from 780 to 850.

The Five Levers That Control Your Score

Your credit score isn’t a mystery — it’s an algorithm. FICO weighs five factors, and knowing the weights shows you exactly where to focus.

1. Payment History (35%) — The Foundation. Have you paid your bills on time? Even one 30-day late payment is a Credit Nuke — it can drop your score dramatically and stay on your report for 7 years. Set up autopay for the minimum on every account so this never happens.

2. Credit Utilization (30%) — The Speed Lever. How much of your available credit are you using? If you have $10,000 in total limits and carry $3,000 in balances, your utilization is 30%. Under 30% is the guideline; under 10% is ideal and can boost your score within 30 days. This is the fastest lever you can pull — we detailed the Utilization Sprint Protocol in our credit score improvement guide.

3. Length of Credit History (15%) — The Old Growth Bonus. How long have your accounts been open? This is why you generally shouldn’t close old credit cards, even if you don’t use them. The age of that account is a pillar of your score.

4. New Credit (10%) — The Inquiry Tax. Every time you apply for new credit, you lose roughly 3–5 points from the hard inquiry. Space applications out by at least 6 months when possible.

5. Credit Mix (10%) — Do you have different types of credit (credit cards, auto loan, student loan)? A healthy mix helps slightly, but don’t open accounts just to check this box.

The takeaway: Payment history and utilization together make up 65% of your score. If you pay on time and keep balances low, you’re covering the vast majority of what matters.

The Invisible Score Tax: What Your Score Actually Costs You

Mortgages: The spread between a 620 score and a 760+ on a $350,000, 30-year mortgage can mean roughly $50,000 in extra interest over the life of the loan. Same house, same neighborhood — just a different three-digit number.

Auto Loans: Superprime borrowers (780+) get rates around 4–5%. Deep subprime (below 580) can see rates above 16%. On a $30,000, 60-month car loan, that gap means roughly $175 more per month — enough to have bought a second car with the money wasted on interest.

Car Insurance: In most states, insurers use credit-based insurance scores to set premiums. Drivers with poor credit pay on average 105% more than those with excellent credit. Same car. Same driving record. Different score. Different price.

Renting: Landlords routinely check credit. A low score can mean a denied application, a higher security deposit, or both.

Credit Cards: Lower scores mean higher APRs, lower limits, and fewer rewards — which feeds right back into higher utilization and makes the problem worse.

This is why we call it a tax. You pay it every day, whether you realize it or not.

The 2026 Trended Data Shift

One thing most credit score articles won’t tell you: lenders are increasingly moving to newer scoring models — FICO 10T and VantageScore 4.0 — that don’t just look at what you owe today. They look at your trend over the last 24 months.

If you only pay the minimum every month, these models see Debt Persistence — a pattern we flagged in our minimum payments article — and flag you as a higher risk even if you’re never late. Start paying even $20 above the minimum to show a downward balance trend. The algorithm rewards direction, not just current position.

How to Check Your Score (For Free)

Most banks and credit card issuers now show your FICO score in your online account or on your statement. Check there first.

Get free credit reports from all three bureaus at AnnualCreditReport.com. According to FTC research, roughly 1 in 5 credit reports contains an error that could affect your score. Review yours at least once a year and dispute any mistakes — it’s free.

Checking your own score is a “soft pull” with zero effect. Applying for new credit is a “hard pull” that can temporarily lower your score.

The Action Plan: Where to Go From Here

Below 580: Focus on payment history. Autopay everything. Get a secured credit card. See our credit building guide.

580–669: Attack utilization. Pay down balances aggressively. See our credit card debt payoff plan.

670–739: You’re close to the 740 sweet spot. Run the Utilization Sprint Protocol from our 100-point guide. Getting under 10% utilization can push you over.

740+: Maintain. Don’t close old accounts, keep utilization low, and don’t apply for unnecessary credit. You’re already getting the best rates.

Stop letting the Invisible Score Tax drain your bank account. The levers are right in front of you.

FAQ

What’s a “good enough” credit score?

740 is the practical target. Above that, you qualify for the lowest mortgage rates, best cards, and cheapest insurance. The difference between 740 and 850 is minimal in real-world cost.

How long does it take to improve?

Lowering utilization can boost your score within 30 days. Late payments take longer (7 years on your report, but impact fades). See our full plan.

Does checking my own score hurt it?

No. Soft inquiry. Zero effect.

Is a credit score the same as a credit report?

No. The report is the detailed record. The score is a number calculated from it. You can have a clean report with no score (too new) or a mediocre score despite a decent report (if utilization is temporarily high).

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: