How to Set Financial Goals That Actually Stick (The 2026 Framework)

Quick Verdict: “Save More Money” Is Not a Goal — It’s a Wish

“I want to save more money.” “I want to get out of debt.” “I want to start investing.” These sound like goals but they’re wishes — no number, no deadline, no plan. That’s why they dissolve by February.

A real financial goal has three parts: a specific dollar amount, a specific deadline, and a system that makes it happen automatically. “Save $6,000 by December 31 by automating $500/month into my HYSA” is a goal. It’s concrete, trackable, and tied to a Ghost Paycheck instead of willpower.

We’ve spent 48 articles giving you every tool — budgets, debt strategies, automation, investment accounts, salary negotiation. This post is the roadmap that tells you which tools to use and in what order, based on where you actually are right now.

The Quick Verdict:

- STACK: Write down 2–3 specific goals with dollar amounts and deadlines ✅ — Written goals are 42% more likely to be achieved (Dominican University study).

- STACK: Attach every goal to an automated system ✅ — Willpower is a battery that drains. A system is a solar panel that recharges itself.

- RUNNER UP: Review quarterly — not daily — Check progress every 3 months. Adjust the timeline, not the goal.

- SKIP: Setting 10 goals at once ❌ — Focus on 2–3. Everything else gets minimum payments and waits its turn.

The BrokeToBanking Goal Framework (3 Steps)

Step 1: Know Where You Stand

Before setting goals, spend 15 minutes calculating your starting position:

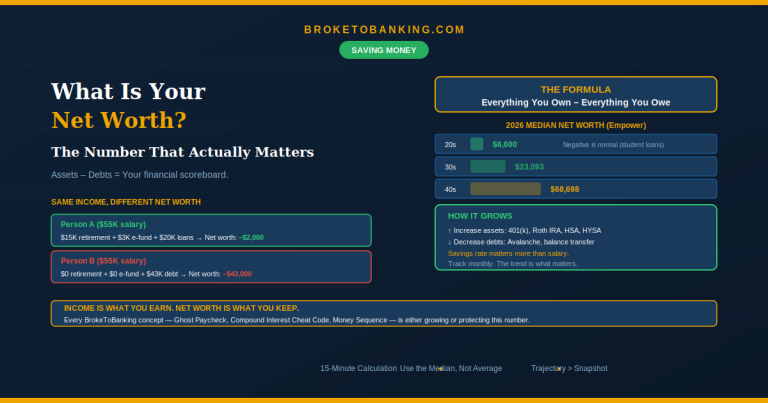

- Net worth: Everything you own minus everything you owe. Your credit score tells you how good you are at borrowing money. Your net worth tells you how good you are at keeping it.

- Monthly margin: Income minus essential expenses. This is what you have to deploy.

- Debt list: Every balance, rate, and minimum payment. Rank by interest rate.

- Current savings/investments: Emergency fund, retirement accounts, HYSA balance.

You can’t plot a route without knowing the starting point.

Step 2: Pick 2–3 Goals From Your Phase

Your goals map directly to wherever you are in the Money Sequence. Don’t jump around.

Phase 1 — Build the Foundation:

| Goal | Example | System |

|---|---|---|

| Build $1,000 Starter Buffer | “Save $1,000 by August 31” | Ghost Paycheck + Liquidation Sprint |

| Get the full 401(k) match | “Contribute 4% starting next paycheck” | One-time HR portal change |

| Kill credit card debt | “Pay off $2,800 Card A by March” | Debt Avalanche + autopay |

Note: In 2026, $1,000 is a Starter Buffer, not a full emergency fund. The goal should be to move from $1,000 to the One Month of Survival milestone (~$2,600) as fast as possible. Sell three things you haven’t touched in a year — use that windfall to bridge the gap.

Phase 2 — Accelerate:

| Goal | Example | System |

|---|---|---|

| Kill remaining high-interest debt | “Pay off $4,200 total by December” | Balance transfer + Avalanche |

| Build e-fund to 3 months | “Reach $7,800 by next June” | Redirect former debt payments |

| Open and fund Roth IRA | “Contribute $3,000 this year” | $250/month auto-invest into index fund |

The 6% Rule matters here: If you have a student loan at 5.2% and a Roth IRA expected to return 8–10%, aggressively paying the loan instead of investing is a Success Tax on your future self. Automate the minimum on low-interest debt and redirect the margin to the Compound Interest Cheat Code.

Phase 3 — Build Wealth:

| Goal | Example | System |

|---|---|---|

| Max Roth IRA ($7,500) | “$625/month automated” | Monthly DCA |

| Increase 401(k) to 15% | “Raise 1% per quarter” | Auto-escalation |

| Build 6-month e-fund | “Reach $15,500 by year-end” | Sinking fund approach |

| Grow net worth by $10K | Track monthly | Full automation across all accounts |

The rule: Pick 2–3 goals from your current phase. Not 10. Not from multiple phases. Focus wins.

Step 3: Make Every Goal Automatic

The difference between goals that stick and goals that fail isn’t motivation — it’s systems:

“Save $1,000 by August” → $167/month auto-transfer to HYSA on payday.

“Pay off Card A by March” → Autopay the calculated amount using Avalanche math.

“Fund Roth IRA $3,000 this year” → $250/month auto-invest into VTI or FZROX.

If achieving the goal requires you to remember something every month, it will eventually fail. If it’s automated, it happens whether you’re motivated or not. Willpower is a battery that drains. Systems are solar panels that recharge themselves.

The Review Cadence: Check, Don’t Obsess

Monthly (5 minutes): Update your net worth. Seeing the number move — even $200 — is the most powerful behavioral reinforcement available.

Quarterly (30 minutes): Review progress on each goal. If you miss a milestone, don’t lower the goal — use the Pivot Rule: increase your Ghost Paycheck by 1% or cut one Zombie Subscription you’re paying for but not using. Checking your portfolio daily in a volatile 2026 market is a recipe for panic selling. Quarterly is the sweet spot.

Annually (1 hour): Full review. Recalculate your Survival Number. Check your credit report. Reassess which phase of the Money Sequence you’re in. Set next year’s 2–3 goals. If you hit your net worth target early, don’t increase your lifestyle — increase your sinking funds for next year.

The Skeptic’s Friction Report

“I don’t have enough margin for goals.” $50/month toward one goal is $600 in a year. Our save $1,000 fast and lower bills guides create margin where none seems to exist. Start with what you have.

“What if something comes up?” That’s what your emergency fund and sinking funds handle. Real emergencies pause goals temporarily — they don’t cancel them. The Replacement Protocol rebuilds, and you resume.

“I’ve tried this before and quit.” Most goal-setting fails because it relies on willpower. “I’ll try to save more” fails. “$200 auto-transferred on the 1st” doesn’t. Attach every goal to automation and the system does the work.

FAQ

How many goals should I have?

Two to three active. More splits focus and margin too thin. Everything else gets minimum payments until a slot opens.

Debt or savings first?

Both. Money Sequence: $1,000 e-fund → high-interest debt → savings and investments together.

What if my income changes?

Adjust the monthly amount, not the goal. Slower timeline, same destination. Stopping completely is the only real failure.

How do I stay motivated?

Track net worth monthly. Celebrate every emergency fund milestone — Buffer, Breathing Room, Security, Freedom. Each one is a win.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: