Best Credit Cards for Building Credit in 2026 (No Annual Fee)

Quick Verdict: Escaping the “Invisible Score Tax”

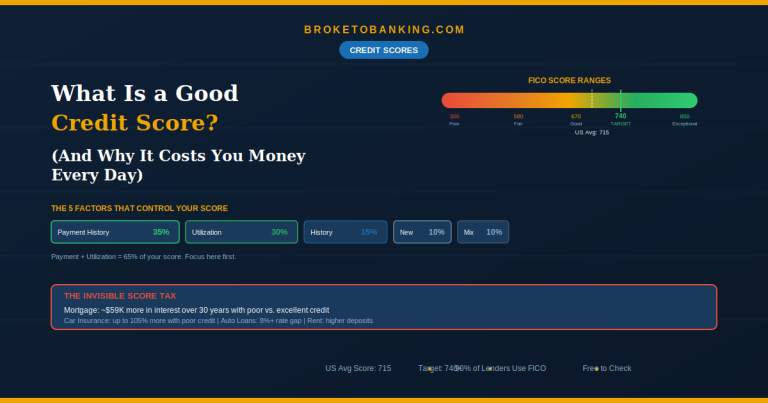

Your credit score is one of the most important numbers in your financial life — yet most people treat it like background noise until they suddenly need it.

A bad credit score quietly costs you money every single day: higher interest rates on car loans, bigger insurance premiums, apartment applications denied or requiring larger deposits. In 2026, with average credit card APRs near 22%, the difference between a 620 score and a 750 score on a car loan can easily mean paying thousands more in interest over the life of the loan. This is the Invisible Score Tax — and it runs on autopilot until you do something about it.

The fastest legitimate way to build credit from zero — or rebuild after damage — is a credit card used correctly. Not to borrow money. Not to carry a balance. Just make small purchases, pay the full balance every month, and let the positive payment history report to all three credit bureaus.

My top pick for most people: Discover it® Secured — the only credit-building card that actually pays you real cash back while you build. Automatic upgrade review at 7 months. Strong runner-up: Chime Credit Builder Visa® — no credit check, no interest, no minimum deposit, and automatic rent reporting in 2026. The best entry point for credit ghosts. Skip entirely: Any card that charges a monthly maintenance fee, account opening fee, or “program fee.” These exist and are traps. Specific examples: Indigo, Milestone, and some First Progress tiers charge fees that eat 50% of your credit limit before you buy a tank of gas. If a card “guarantees approval” and charges upfront fees, walk away.

The 2026 Credit Reality — Trended Data Changes the Rules

Before the card rankings, something that actually matters in 2026: a growing number of lenders now use scoring models like FICO 10T and VantageScore 4.0 that analyze “Trended Data” — up to 24 months of payment behavior, not just your current snapshot.

The practical implication: lenders can increasingly see how you pay, not just what you owe. Carrying a $50 balance for three months looks like “debt persistence.” Paying $500 in full every month looks like “financial stability.”

The rule this creates: Pay the full balance every month without exception. Not just for your score today — but because a growing portion of lenders are watching the pattern, not just the number.

How Credit Cards Build Credit — The Mechanics

Your credit score comes from five factors. Two of them — Payment History (35%) and Credit Utilization (30%) — make up 65% of your total score, and a credit card gives you direct control over both.

Payment History: Every on-time payment gets reported to Equifax, Experian, and TransUnion. Every one is positive data. One missed payment on a thin credit file can cause significant damage — protect this factor above everything else.

Credit Utilization: The percentage of available credit you’re actually using at statement time. If your limit is $500 and your balance is $400, that’s 80% utilization — which actively drags your score down regardless of whether you pay it off. Keep it below 30% (ideally under 10%).

The correct usage pattern:

- Use the card for 1–2 small, recurring purchases each month (one tank of gas, one subscription)

- Pay the full balance before the due date every month — not the minimum

- Never carry a balance — you are not using this card to borrow money

- Keep your balance low relative to your limit at all times

Done consistently, this produces meaningful score improvements within 3–6 months according to published consumer credit research.

Secured vs. Unsecured — Which Do You Need?

Secured cards require a refundable cash deposit (usually $200 minimum) that becomes your credit limit. Designed for people with no credit history or poor credit (below 580). Approval rates are high because your deposit protects the issuer.

Unsecured cards require no deposit but need at least fair credit (580+) or some existing history. If you’re starting from absolute zero — a “credit ghost” with no file at all — a secured card is almost always the right first step.

The secured card isn’t permanent. After 6–12 months of responsible use, most issuers automatically review you for upgrade to an unsecured card and return your full deposit. It’s a launchpad, not a destination.

The Best No-Annual-Fee Credit-Building Cards of 2026

1. Discover it® Secured — Best Overall

Annual fee: $0 | Minimum deposit: $200 (refundable) | Reports to: All three bureaus Upgrade review: Automatic starting at 7 months Rewards: 2% cash back at gas stations and restaurants (up to $1,000 combined quarterly), 1% everywhere else

Why it wins: The only credit-building card that actually pays you meaningful cash back while you build. The Cashback Match feature doubles all rewards earned in your first year — no other secured card does this. You’re getting paid to build credit.

The automatic upgrade review at 7 months is industry-leading. Most competitors take 12+. Discover’s process is truly automatic — no call, no reapplication. If you’ve been responsible, they upgrade you and return the full deposit.

My take: For most people who can swing the $200 deposit, this is the one. Real rewards and a clear path out of secured status.

The Skeptic’s Friction Report:

The APR is a house fire. Discover it Secured charges a high variable APR on balances — as does every secured card. This is irrelevant if you pay in full every month, which you must. The rule: use it for one tank of gas a month, set it on autopay for the full balance, and put the physical card in a drawer. Don’t think about it again until the upgrade notice arrives.

2. Chime Credit Builder Visa® — Best for Credit Ghosts

Annual fee: $0 | Deposit: $0 (funded from your Chime checking balance) | Reports to: All three bureaus Interest: 0% | Rewards: None | Credit check: None

Why it’s here: No credit check. No minimum deposit. No interest. You move money from your Chime checking account to your Credit Builder account — that becomes your spending limit. You literally cannot go into debt because you can only spend what you’ve already moved there.

The 2026 edge: Chime now includes automatic rent reporting. For most people on tight budgets, rent is the largest monthly expense. Getting rent reported to the bureaus is the fastest way to bulk up a thin credit file — and Chime handles it automatically.

My take: The best entry point for genuine credit ghosts — people starting from absolute zero with no file at all — or anyone recovering from recent bankruptcy who can’t get approved elsewhere. Use it to establish history and get above 650, then graduate to Discover or Capital One.

The Skeptic’s Friction Report:

No traditional upgrade path. Chime Credit Builder doesn’t have a runway to a high-limit travel rewards card. It’s a foundation tool for a specific job: getting your score above 650 so you qualify for the cards that actually pay you.

3. Capital One Platinum Secured — Lowest Entry Cost

Annual fee: $0 | Minimum deposit: $49 (for a $200 credit limit) | Reports to: All three bureaus Upgrade review: Automatic at 6 months | Rewards: None

Why it’s strong: The $49 minimum deposit makes this the most accessible secured card when $200 isn’t available. You put down $49, get a $200 limit — a 4:1 leverage ratio no other major card matches. Capital One’s 6-month automatic upgrade timeline is the fastest of any major issuer.

My take: No rewards, but the lowest cash barrier. Makes the most sense when the Discover deposit isn’t feasible. If $200 is accessible, Discover edges it out.

4. Capital One Quicksilver Secured — Best Flat-Rate Rewards

Annual fee: $0 | Minimum deposit: $200 (refundable) | Reports to: All three bureaus Upgrade review: Automatic at 6 months Rewards: 1.5% cash back on all purchases, 5% on Capital One Travel

Why it’s strong: Flat 1.5% on everything beats many unsecured cards. If your spending is spread across many categories rather than concentrated at gas stations and restaurants, this can outperform Discover’s tiered structure.

My take: The choice between this and Discover comes down to spending patterns. Concentrated at gas and restaurants → Discover. Spread across everything → Quicksilver Secured.

5. OpenSky® Plus Secured — Best When Everything Else Says No

Annual fee: $0 | Minimum deposit: $300 | Reports to: All three bureaus Upgrade review: Limited | Rewards: Limited | Credit check: None

Why it’s here: No credit check at all. No hard inquiry, no denial risk. For people with severe credit damage who keep getting rejected, this is the most accessible entry point available. According to OpenSky’s published data, 2 out of 3 cardholders see an average score increase of 47 points after 6 months.

My take: Solid safety net when other cards say no — but not the first choice if you have other options. The upgrade path is limited compared to Discover and Capital One.

6. Capital One Platinum (Unsecured) — Best for Fair Credit

Annual fee: $0 | Deposit: None | Reports to: All three bureaus Credit required: Fair (580+) | Rewards: None

Why it’s here: If you already have some credit history and your score is in the fair range (580–669), you may be able to skip the secured route entirely. The most commonly recommended unsecured starter card — no fee, no deposit, clear upgrade path to better Capital One products.

My take: If you qualify, skipping the deposit entirely is appealing. Same rule applies: pay in full every month.

The “Authorized User” Strategy — The Credit Hack Most People Miss

If someone you trust has a card that’s at least a few years old, has low utilization, and a clean payment history — ask to be added as an authorized user.

The card’s entire positive history appears on your credit report. You don’t even have to use the card. Just being listed can add years of good history to a thin file and produce meaningful score improvements. Still works effectively on Chase and Discover accounts. 100% legal — one of the most powerful tools for credit ghosts specifically.

The BNPL Warning — A 2026-Specific Risk

Buy Now, Pay Later (Klarna, Affirm, Afterpay) now reports to credit bureaus. Most people don’t know this yet.

One missed $20 payment on a pair of shoes can now appear on your credit file and damage a thin history significantly. If you’re actively building credit in 2026, treat every BNPL installment with the same seriousness as a credit card payment. Missing one is no longer a minor inconvenience — it’s a reportable derogatory mark on the file you’re working hard to build.

The Rules That Actually Move the Needle

Regardless of which card you choose:

Rule 1: Pay the full balance every month — not the minimum. Non-negotiable. Rule 2: Keep utilization below 30% at statement time — ideally under 10%. Rule 3: Never miss a payment. Set autopay for the full balance. Rule 4: Don’t apply for multiple cards at once. Each hard inquiry temporarily dips your score. Rule 5: Keep the account open. Credit age matters (15% of your score). When you upgrade, the original history typically carries over.

The Comparison Table

| Card | Annual Fee | Min. Deposit | Rewards | Upgrade Timeline | Best For |

|---|---|---|---|---|---|

| Discover it® Secured | $0 | $200 | 2%/1% cash back | 7 months (auto) | Best overall |

| Chime Credit Builder | $0 | $0 | None | N/A | Credit ghosts, 0% interest |

| Capital One Platinum Secured | $0 | $49 | None | 6 months (auto) | Lowest entry cost |

| Capital One Quicksilver Secured | $0 | $200 | 1.5% flat | 6 months (auto) | Flat-rate rewards |

| OpenSky® Plus Secured | $0 | $300 | Limited | Limited | No credit check needed |

| Capital One Platinum (unsecured) | $0 | None | None | Auto | Fair credit, no deposit |

FAQ

How long does it take to see credit improvements? Initial movement can appear within 30–60 days of the first payment reporting. Meaningful score jumps typically take 3–6 months of consistent on-time payments and low utilization.

Does opening a secured card hurt my score? A new card causes a small temporary dip from the hard inquiry (usually 2–5 points). Within a few months of responsible use, the positive payment history far outweighs it. Net effect is positive.

Can I build credit without carrying a balance? Yes — and you should. Paying in full every month avoids all interest while still building payment history.

When should I upgrade from a secured card? When the issuer automatically reviews you — typically 6–12 months. Don’t close the secured card after upgrading. Let the issuer convert it or keep it open to preserve account age.

Should I get multiple credit-building cards at once? Not initially. One card used correctly builds credit just as effectively, without extra complexity or multiple hard inquiries. After 12+ months with a score above 670, adding a second card makes more sense.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation. Credit card terms, rates, and features are subject to change — verify current terms at each issuer’s website before applying.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: