Should You Invest While You’re in Debt? (The 2026 Decision Framework)

Quick Verdict: It’s Not Either/Or — It’s a Sequence

“Should I invest or pay off debt?” is the most common question we get — usually from someone in their late 20s with a credit card balance, student loans, and a growing panic that they’re falling behind on retirement. The advice in 2026 is more polarized than ever: the “Debt-Free or Die” crowd says never invest until you owe zero; the “Leverage Everything” crowd says always invest because compound interest. Both are dangerous because they ignore the math of Interest Gravity.

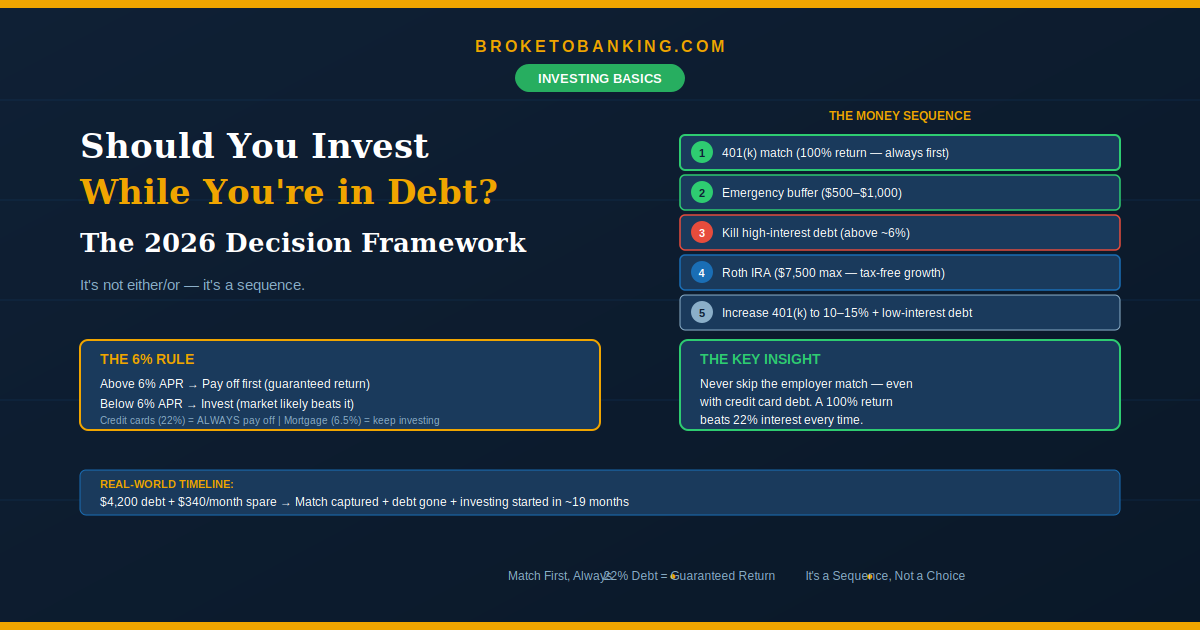

The real answer is a sequence — a specific order of operations that captures guaranteed returns first, attacks high-interest debt, then builds long-term wealth. We call this the Money Sequence, and it ties together almost everything we’ve published on this site.

The Quick Verdict:

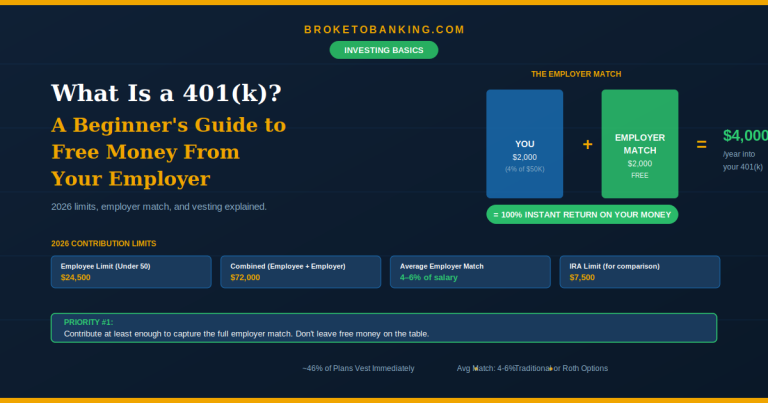

- STACK: Always capture your full 401(k) employer match — even while in debt ✅ — A 50–100% guaranteed return beats any credit card APR. It’s the only “sure thing” in the market. See our 401(k) guide.

- STACK: Pay off all credit card debt before investing beyond the match ✅ — No investment reliably returns 22%. Debt payoff is a guaranteed, risk-free return.

- RUNNER UP: After high-interest debt is gone, use the 6% Rule — Below 6% APR, investing wins. Above 6%, debt payoff wins.

- SKIP: Buying individual stocks or crypto while carrying 22% credit card debt ❌ — You’re borrowing at 22% to try and earn 10%. That’s a Success Tax that will keep you broke.

The Money Sequence (The Exact Order)

Step 1: Capture the full 401(k) match. If your employer matches 100% up to 4%, you contribute 4%. Period. This is a guaranteed 100% return — it beats every credit card APR in existence. Even Fidelity’s analysis confirms: never skip the match, regardless of your debt situation.

Step 2: Build a $1,000 Financial Armor buffer. Before you attack debt, you need a shield. If you have $0 in savings, the next flat tire or ER visit goes straight onto your credit card, resetting all your progress. Build $1,000 in a high-yield savings account first. We detailed this in our emergency fund guide.

Step 3: Kill all high-interest debt — the 22% Wall. As of early 2026, the average credit card APR is roughly 22%. Paying off a $5,000 balance at 22% is the mathematical equivalent of earning a guaranteed, tax-free 22% return on your money. Use the Debt Avalanche to escape Interest Gravity as fast as possible.

Step 4: Fund a Roth IRA ($7,500 in 2026). Once the credit cards are dead, redirect that “debt payment” into a Roth IRA. Tax-free growth for decades — the Compound Interest Cheat Code from Post #9. Any remaining low-interest debt (student loans under 6%, auto loans) is cheap enough that investing alongside minimum payments makes mathematical sense.

Step 5: Increase 401(k) contributions toward 10–15% of income and tackle remaining low-interest debt.

The 6% Rule: Where the Line Lives

Not all debt is expensive. According to Fidelity’s research, the breakeven between paying off debt and investing is roughly 6% APR. Here’s what that looks like in 2026:

| Debt Type | Typical 2026 APR | Action |

|---|---|---|

| Credit cards | 21–24% | Pay off immediately — nothing beats this guaranteed return |

| Personal loans | 10–18% | Pay off before investing beyond the match |

| Grad/PLUS student loans | ~7–9% | Pay off before extra investing — above the line |

| Undergrad federal loans | ~5.5–6.5% | The gray zone — 50/50 split between payoff and investing |

| Auto loans | ~5–6% (good credit) | Minimum payments while investing — rate is near or below the line |

| Mortgage | ~6–7% | Minimum payments — longest term, potential tax benefits |

Above the 6% line, pay it off. Below, invest. In the gray zone, a 50/50 split is a reasonable compromise.

Why “Pay Off Everything Before Investing” Is Wrong

1. The employer match is free money. Skipping your 401(k) match to pay extra on your credit card means forfeiting a guaranteed 50–100% return to save 22% on interest. The match wins every time.

2. Compound Interest Time is your most valuable asset. Every year you delay investing costs you growth you can never recover. A 25-year-old who invests $200/month for 10 years and stops will have more at 65 than a 35-year-old who invests $200/month for 30 years. Waiting for “zero debt” to start investing can cost decades of compounding.

3. Not all debt is expensive. A 5% auto loan and a 22% credit card are not the same animal. Treating all debt identically costs you growth on money that would have earned far more than 5% in the market.

Why “Just Invest, Debt Doesn’t Matter” Is Also Wrong

1. 10% is an average, not a guarantee. Historical market returns average ~10% over decades, but in any given year, you could lose 20%. Paying off 22% credit card debt is a guaranteed, risk-free 22% return. Guaranteed beats hopeful.

2. The Psychological ROI is real. Mathematically, a 5% student loan is “cheap.” But if that loan is causing you daily anxiety, the peace of mind from paying it off has real value that doesn’t show up in a spreadsheet. According to NIH research, heavy debt is linked to significantly higher rates of stress, anxiety, and depression.

3. Risk for zero net gain. If you invest at 8% while owing 8%, you’re taking on market risk for a 0% net advantage. The debt payoff is the same return with zero risk. Why gamble for nothing?

The Real-World Example (Our Target Reader)

Let’s map the Money Sequence onto our actual reader: 27 years old, $4,200 in credit card debt at 22% APR, $340 left after bills, employer offers 4% 401(k) match.

Step 1: Contribute 4% to 401(k) → captures full match (~$150/month from employer on a $45K salary)

Step 2: Build $1,000 buffer → takes ~3 months at $340/month

Step 3: Attack credit card debt with everything remaining → at ~$300/month, $4,200 is gone in ~16 months

Step 4: Cards paid off → redirect $300/month into a Roth IRA at Fidelity → $3,600/year growing tax-free

Total timeline from start to investing: roughly 19 months. And the 401(k) match was growing the entire time. You weren’t “choosing” between debt and investing — you were sequencing them.

FAQ

What if I have no employer match?

Skip Step 1 and go straight to the buffer and debt payoff. Once high-interest debt is cleared, open a Roth IRA. See our investing apps guide.

Should I stop my 401(k) to pay off debt faster?

Only reduce below the match if you’re in a genuine crisis (can’t make minimum payments). Otherwise, always capture the full match. That 100% return is irreplaceable.

What about student loans?

Federal loans below 6% are generally fine to carry while investing. Make minimums and focus extra on the Roth IRA. Above 8%, prioritize payoff. In the 6–8% range, split 50/50.

I only have $50/month extra. Where does it go?

If you have high-interest debt: $50 extra toward the target card after capturing the match. If no high-interest debt: $50/month into a Roth IRA. That’s $600/year — better than $0/year. The amount matters less than the sequence.

The bottom line: You can’t out-invest a high-interest debt fire. Get the free money from your employer, build your $1,000 shield, and then hunt down your credit card debt like it’s a personal insult. Only once the high-interest chains are gone are you truly free to build wealth.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: