How to Make a Budget in 2026 (A Simple Guide That Actually Works)

Quick Verdict: A Budget Is a Data Map, Not a Cage

Most people approach budgeting as an exercise in self-punishment — saying “no” to everything enjoyable and staring at a spreadsheet. That mindset is a one-way ticket to quitting. A budget isn’t a cage; it’s a Data Map. It shows you where your money is leaking and where it can be redeployed to fight Interest Gravity. If you don’t tell your money where to go, the 2026 economy will decide for you.

Everything we’ve written on this site — from the Ghost Paycheck to the Survival Number to the Money Sequence — is built on one idea: every dollar needs a job. A budget doesn’t tell you that you can’t have fun. It tells you how much fun you can have without ruining your 2030.

The Quick Verdict:

- STACK: The 50/30/20 framework as your starting point ✅ — The Honda Civic of budgeting. Reliable, efficient, gets you where you need to go.

- STACK: Track every dollar for one full month ✅ — You can’t fix what you can’t see. The first month is a diagnostic, not a grade.

- RUNNER UP: Use YNAB or a simple spreadsheet — The tool matters less than the habit.

- SKIP: “Mental budgeting” — having “a general idea” of what you spend ❌ — If you’re estimating, you’re underestimating by 25–30%. The bank statement is the only source of truth.

Step 1: Find Your Net Reality (5 Minutes)

Your salary is a vanity metric. The only number that builds wealth is your net income — the amount that actually hits your bank account after taxes, insurance, and retirement contributions are taken out.

If you have a regular paycheck, check your most recent pay stub. Multiply the deposit by how often you’re paid (biweekly = ×26, then ÷12 for monthly).

If your income is irregular, use the Baseline from our irregular income guide — your lowest month over the last 6–12 months. Budgeting from your average is how people end up in credit card debt during low months.

Example: Take-home pay of $3,400/month. That’s our working number.

Step 2: List Every Expense (30 Minutes)

Pull up your bank statements from the last 2–3 months. Categorize every transaction into two lists:

Fixed expenses (the “Must-Pays”): Rent, car payment, insurance, minimum debt payments, phone, subscriptions.

Variable expenses (the “Leaks”): Groceries, gas, dining out, entertainment, personal care, clothing.

Don’t estimate from memory — use actual transactions. Pull your “dining out” average from the last 90 days. It will almost certainly be higher than you think. That’s not a reason to feel guilty. It’s a reason to get accurate.

Example on $3,400/month:

| Category | Monthly Amount |

|---|---|

| Rent | $1,200 |

| Car payment + insurance | $450 |

| Utilities | $150 |

| Phone | $75 |

| Minimum debt payments | $116 |

| Groceries | $350 |

| Gas/transportation | $120 |

| Dining out | $150 |

| Subscriptions | $55 |

| Personal/misc | $100 |

| Total | $2,766 |

| Margin | $634 |

That $634 is your margin — and without a budget, it vanishes into Checking Account Gravity (Post #12). Leaving savings in your checking account is how margin turns into lifestyle creep. Automate it out on payday.

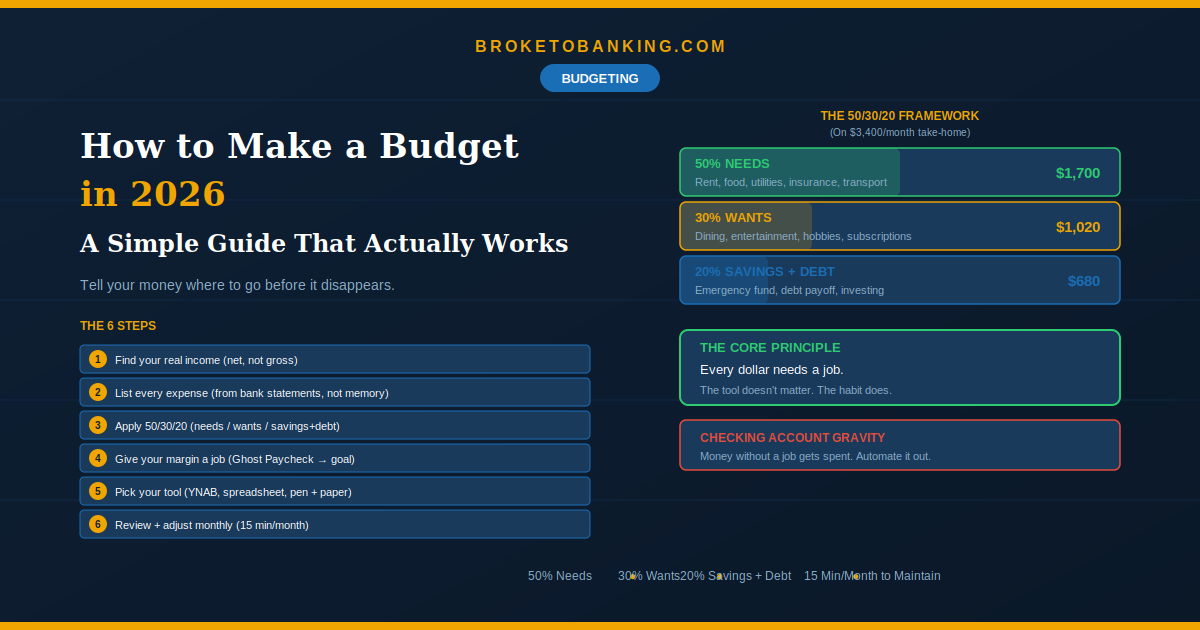

Step 3: Apply the 50/30/20 Framework

50% → Needs ($1,700): Rent, utilities, groceries, insurance, transportation, minimum debt payments. This is your Survival Number. If this hits 60% in 2026, don’t panic — pull from Wants to balance it.

30% → Wants ($1,020): Dining, entertainment, subscriptions, hobbies. This is the first lever you pull when things get tight.

20% → Savings & Debt Payoff ($680): Emergency fund, extra debt payments, retirement investing. This is where the Money Sequence lives. This 20% is the most important money in your financial life. Your future self is waiting for it to land in a Roth IRA.

Reality check: If your needs exceed 50%, that’s normal — especially in high-cost areas. Adjust the percentages to fit your life. 60/20/20 or 65/15/20 is fine right now. The goal is a conscious split, not a perfect one.

Step 4: Give Your Margin a Job (The Money Sequence)

That $634? It gets deployed in this exact order:

1. Capture the 401(k) match. The guaranteed 100% return.

2. Build $1,000 in Financial Armor. Set up as a Ghost Paycheck — automatic, on payday, before you see it.

3. Kill credit card debt using Avalanche or Snowball.

4. Fund your Roth IRA ($625/month maxes it out at $7,500/year).

The budget isn’t just tracking — it’s deploying your margin toward the next step.

Step 5: Pick Your Tool

YNAB: The gold standard. Only lets you budget money you actually have. $109/year — the Success Tax from our YNAB vs EveryDollar review. Worth it if you commit.

Free spreadsheet: Google Sheets or Excel. $0. Total control. Works great if you update it — becomes a paperweight if you don’t.

Your bank app: Most now categorize transactions automatically. Good for the “I just need to see where it goes” stage.

Pen and paper: It works. The tool doesn’t matter. The habit does. If you know you won’t log every coffee manually, use an app that automates the visibility. The best budget is the one you actually look at.

Step 6: Review and Adjust Monthly (15 Minutes)

Your first budget is a draft. Expect it to be wrong. Adjust and keep going.

Compare planned vs. actual spending monthly. Are you consistently over in one category? That’s either a budget problem (unrealistic number) or a spending problem (behavior to address). Knowing the difference is the point.

The Skeptic’s Friction Report:

Budgets fail from rigidity, not indulgence. Build in a Sinking Fund for irregular but predictable costs — tires, birthday gifts, medical co-pays. If your budget doesn’t account for these, it’ll break the first time reality hits. And if you have a category for “Cat Toys” and another for “Cat Food,” you will quit. Keep it simple. Broad buckets. Fewer categories. The goal is progress over 12 months, not perfection in any single month.

FAQ

What if I’m spending more than I make?

That’s the most important thing a budget can reveal. Start with our lower your bills guide for painless wins, then audit the Zombie Subscriptions delivering zero value.

What’s the best method for beginners?

50/30/20. Simplest framework. If you want more control later, move to zero-based (YNAB). If income varies, use the Baseline Budget System. The method matters less than starting.

How long does it take each month?

After setup (~1 hour), monthly maintenance is 15–30 minutes. If it takes longer, it’s too complicated.

I’ve tried budgeting before and quit.

Most people quit because the budget was too rigid, had too many categories, or felt like punishment. Start simpler. More flexibility. Give your margin a specific job (emergency fund, debt, Roth IRA) so you can see the progress. Progress is the best motivator.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: