How to Read Your Credit Report (And Fix Errors That Are Costing You Money)

Quick Verdict: 1 in 5 Reports Has an Error — And You’re Paying for It

Think of your credit report as the raw data that feeds your credit score. Every detail that goes into your score — how you’ve paid your bills, how much you owe, how long you’ve had accounts — comes straight from this one document. When something’s wrong in the report, your score ends up wrong too. And that wrong score quietly jacks up the interest you pay on loans, insurance, and credit cards without you ever knowing. That’s the Accuracy Tax — and you’re paying it every day it goes unfixed.

The FTC says roughly 1 in 5 reports contains mistakes. We’re not talking about a typo in your middle name. These are things like balances that don’t match reality, accounts that aren’t even yours, payments marked “late” when you paid on time, or the same debt showing up twice. It all adds up to the Invisible Score Tax we broke down in our credit score guide. And it’s getting worse: credit bureau complaints now make up over 80% of everything landing at the CFPB, way up from 30% back in 2017.

The good news? Checking your reports is free. Disputing errors is free. And fixing just one mistake can boost your score fast enough to save real money on your next big loan.

The Quick Verdict:

- STACK: Pull reports from all three bureaus at least quarterly ✅ — Free at AnnualCreditReport.com. Once a quarter is the skeptic’s sweet spot — catching an error in April is far easier than fixing it in October.

- STACK: Dispute every error you spot — it’s your legal right ✅ — The bureaus must investigate within 30 days.

- RUNNER UP: Check before any major application — Mortgage, auto loan, apartment. Fix problems before they cost you.

- SKIP: Paying “credit repair” services ❌ — They charge $100/month to send the same letters you can send for the price of a stamp.

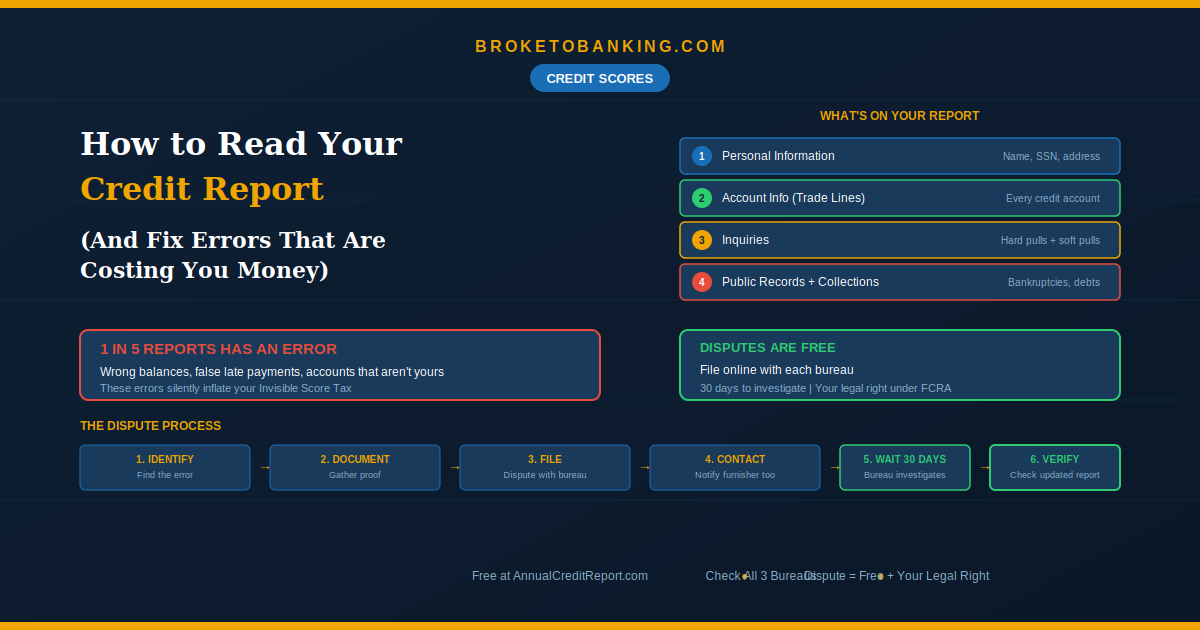

What’s Actually on Your Report (4 Sections)

1. Personal Information — Name, addresses (current and past), SSN, date of birth, employment history. Red flags: misspellings, addresses you’ve never lived at, wrong SSN digits, or someone else’s name mixed in. These glitches often mean a “mixed file” — another person’s accounts tangled into yours, and the most common source of phantom debt.

2. Account Information (Trade Lines) — Every credit account you’ve ever had: cards, car loans, student loans, mortgage. Shows creditor name, account number, open date, credit limit or loan amount, current balance, month-by-month payment history, and status. Red flags: accounts you don’t recognize (identity theft or mixed file), balances that don’t match what you actually owe, “late” payments you know you made on time, closed accounts still listed as open, or the same debt appearing twice under different names.

3. Inquiries — Hard inquiries (you applied for credit — can ding your score for up to two years) and soft inquiries (you checked your own score — zero effect). Red flag: any hard inquiry you didn’t authorize. That’s a sign someone may have tried to open credit in your name.

4. Public Records & Collections — Bankruptcies, court judgments, and accounts sent to collections. Red flags: collections that aren’t yours, wrong balances, or old negative items that should have dropped off (most fall off after 7 years; bankruptcies after 7–10 years).

2026 Updates You Need to Know

The BNPL Audit. As of 2026, Buy Now Pay Later plans from companies like Affirm and Klarna are officially showing up on major credit reports. A $50 “pay in four” marked late can tank your score just as much as a missed credit card payment. Check these carefully — many people don’t realize BNPL activity is being reported.

The Medical Debt Update. A 2025 court ruling vacated the CFPB’s attempted total ban on medical debt reporting. However, the three major bureaus are still voluntarily removing paid medical collections and any medical debt under $500. If you see a paid-off hospital bill or a small medical balance on your report, it probably shouldn’t be there. Dispute it immediately.

Small errors matter. A $20 balance error affects your utilization ratio just as much as a $2,000 one — and utilization is 30% of your FICO score. Don’t ignore “minor” mistakes.

The Most Common Errors (And Why They’re Expensive)

- Incorrect balance — Very common. Makes your utilization look worse than it is.

- Payment marked “late” when it wasn’t — Super common. Payment history is 35% of your score.

- Account that isn’t yours — Common with mixed files. You suddenly “owe” money you don’t.

- Same debt listed twice — Happens when debt gets sold. Doubles the damage.

- Closed account showing as open — Moderate. Messes up utilization math.

- Hard inquiry you didn’t make — Moderate. Identity theft signal.

- Wrong credit limit — Moderate. Distorts your utilization ratio.

Even one of these can drop your score enough to bump you into a higher interest-rate tier. Over the life of a mortgage, that’s easily thousands extra.

How to Get Your Reports (Free)

AnnualCreditReport.com — the only official source. Pull from Equifax, Experian, and TransUnion once per week (permanently free since 2023). Takes about 15 minutes.

Why all three? Each bureau collects data independently. An error might show on one but not the others. Checking only one is like looking under half the couch cushions.

Pulling your own report is always a soft inquiry — zero effect on your score.

How to Dispute Errors (The 2026 Protocol)

The Fair Credit Reporting Act gives you the legal right to fix anything inaccurate. The process is free. But in 2026, the bureaus are notoriously automation-heavy — a computer is likely deciding your case. To win, you need to create enough Manual Friction to get a human to actually look at your file.

Step 1: Contact the furnisher first. The “furnisher” is the bank or lender that reported the wrong info. If they admit the mistake and update their records, the bureau has to follow suit. This is often faster than going through the bureau alone. This is the Furnisher First Rule — don’t just shout at the credit bureau.

Step 2: File the dispute with the bureau. Online is fastest. Certified mail gives you the best paper trail — in 2026, a physical record is the strongest proof they received your evidence. Each bureau’s portal:

- Equifax: equifax.com/personal/credit-report-services/credit-dispute

- Experian: experian.com/disputes/main.html

- TransUnion: transunion.com/credit-disputes

If the error appears on multiple reports, dispute with each bureau separately.

Step 3: Send real documentation, not templates. Bank statements, payment confirmations, closure letters — concrete proof. In the era of AI-processed disputes, bureaus are rejecting generic copy-paste letters from credit repair sites. If your dispute looks like it was generated from a template, it’ll likely get flagged as frivolous. Be specific, be clear, include documents that directly match the error.

Step 4: Wait for the investigation. The bureau has 30 days to investigate (sometimes 45). They must reach out to the furnisher and review your evidence.

Step 5: Verify the fix. If they correct it, you get a free updated report. If not, you can add your own dispute statement, send more documentation, or escalate by filing a complaint with the CFPB at consumerfinance.gov. Pull your report again to confirm the correction actually went through. Don’t assume — verify.

The Credit Report Audit Checklist

Run this every time you pull a report:

- Every account listed is actually mine

- All balances match what I know I owe

- No “late” payments I made on time

- No duplicate accounts (especially collections)

- All closed accounts show as closed

- No hard inquiries I didn’t authorize

- BNPL accounts are accurate and current

- Medical debt that’s paid or under $500 has been removed

- Personal info is correct (name, addresses, SSN)

- All negative items older than 7 years are gone

Your credit report is a living document — and in 2026, it’s under-policed. You have to be your own investigator. If you find an error, treat it like a personal insult to your bank account — because it is.

FAQ

How often should I check my report?

Quarterly is the sweet spot. Always pull all three bureaus 2–3 months before any major application so you have time to fix issues.

Should I pay for credit monitoring?

Not necessary. Many banks now offer free score updates. Credit Karma shows TransUnion and Equifax data for free. Paid services are convenience, not capability.

What about credit repair companies?

Skip them. They charge $50–$200/month for things you can do yourself. Under the Credit Repair Organizations Act, they can’t legally do anything you can’t do for free. The FTC and CFPB both warn consumers about these services.

How long does a dispute take?

Usually 30 days (up to 45 in some cases). Simple fixes like wrong balances or names get resolved quickly. Bigger issues might need a follow-up round with more documentation.

Will disputing hurt my score?

Nope. Filing a dispute doesn’t lower your score. And if they remove a false late payment or fix an inflated balance, your score will typically go up.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: