How to Negotiate Your Credit Card Interest Rate (With Exact Scripts)

Quick Verdict: The 10-Minute “Loyalty Tax” Reversal

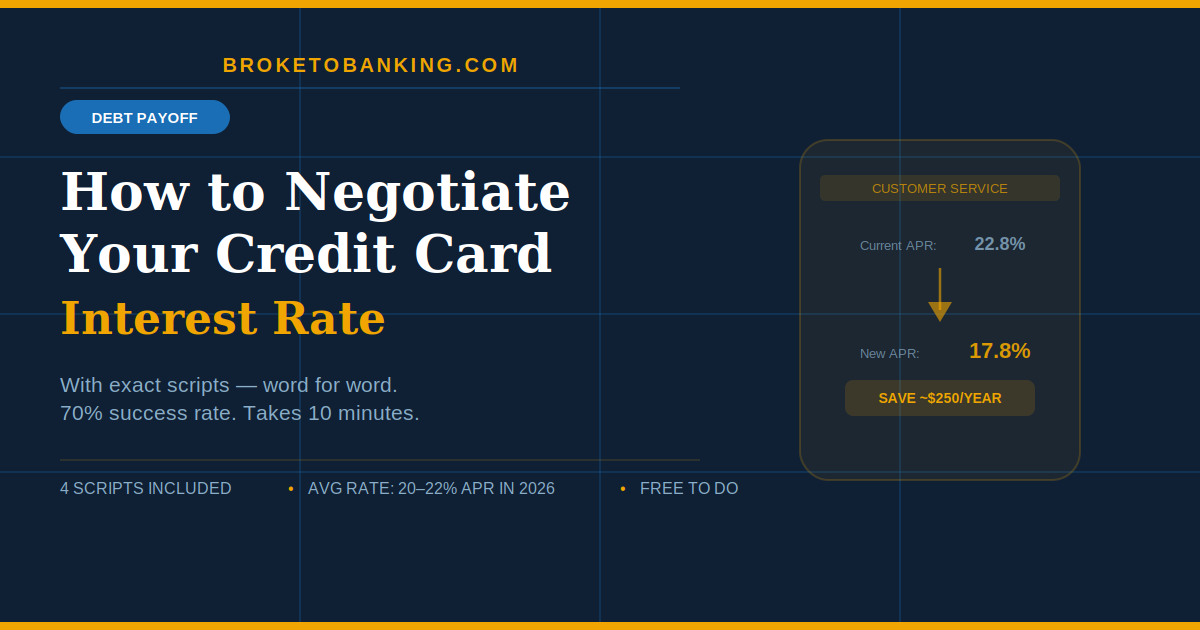

The average credit card interest rate in 2026 is hovering near 22% APR — basically historic highs. On a $5,000 balance at 22%, you’re handing over roughly $1,100 a year in interest alone.

Here’s the skeptical reality: your credit card company is currently charging you a Loyalty Tax. While the Federal Reserve has trimmed rates recently, credit card issuers have been notoriously slow to pass that relief onto existing customers. They’re betting you’ll keep paying yesterday’s rates while the rest of the market moves on.

But the data is on your side. According to a CreditCards.com survey, nearly 70% of cardholders who called their issuer and asked for a rate reduction received one. Only about 25% of cardholders ever make that call.

Do the math: 75% of people are quietly paying a Silence Tax — leaving hundreds of dollars per year on the table because they never picked up the phone. You don’t need a debt relief service. You need 10 minutes, a phone, and the scripts below.

Do this today: Call your oldest card first — your Customer Lifetime Value is highest there, and they’re the most motivated to keep you from transferring your balance to a competitor. Runner-up move: If the call doesn’t work, a 0% balance transfer card is your next move. In 2026, 18–21 month promotional windows are still common. Skip entirely: “Interest rate reduction” companies that charge fees to negotiate on your behalf. They use the exact same scripts below and charge you $500 for the privilege.

Why This Actually Works

Credit card companies quietly charge long-term customers higher rates than brand-new ones who arrived with a promotional offer. They’re betting you’ll never call to challenge it.

When you do call — and politely mention you’re looking at other options — you get routed to the retention department. These people are evaluated on how many customers they don’t lose. They have the pricing keys that frontline reps don’t. Their entire job is to prevent you from moving your balance to a competitor.

The math that makes this worth 10 minutes:

- On a $5,000 balance at 22% APR, dropping 5 points to 17% saves approximately $250 per year — about $20/month.

- On a $10,000 balance at 28%, a 6-point reduction saves roughly $600 per year.

Published consumer finance research consistently shows 70% of people who ask get some kind of reduction — typically 3–6 percentage points. That’s real money recovered with one short call.

The “Leverage” Audit — 5-Minute Prep Before You Dial

Don’t go into this call empty-handed. In 2026, fairness isn’t a strategy. Leverage is.

1. Know your current APR Check your latest statement or the app. Look for “Purchase APR.” Write it down.

2. The Credit Score Flex If your score has improved since you opened the account, this is your strongest card to play. You are literally a less risky customer now than when they set your original rate. Free score checks: Credit Karma, your bank app, or Experian.

3. Know your payment history How long have you had the card? How many on-time payments? Long-term on-time customers are exactly who retention departments want to keep.

4. Find your Exit Plan Do a quick search for 0% balance transfer offers from a competitor — Chase Slate Edge, Citi Simplicity, or similar. Having a specific “Plan B” makes your case credible. “I received an offer from [Competitor] for 0% for 18 months” is a concrete alternative your issuer wants to prevent.

5. Call the number on the back of the card Not the website chat. Not the general contact form. The number on the physical card connects you directly to account services with real authority.

The Exact Scripts (2026 Edition)

Script 1: The Loyalty Play

Best for: Cards you’ve had for 3+ years with a clean payment history

“Hi, I’m [Name]. I’ve been a loyal customer since [Year] and I have a perfect payment record on this account. I’m currently paying [X]% APR, but I know rates have been adjusting across the market and I’d like to stay with [Bank Name] — I just need you to review my account for a permanent APR reduction to keep it competitive. Is that something you can look into for me?”

Script 2: The Competitor Leverage Play

Best for: Larger balances you’re genuinely prepared to transfer

“I’m calling because I just received a 0% balance transfer offer from [Competitor] for 18 months. I like [Bank Name]’s service and I’d prefer to stay, but I can’t ignore a 20%+ interest difference on my balance. What can you do to lower my rate today so I don’t have to initiate this transfer?”

This works because you’re giving the retention rep a clear business reason to act — they don’t want to lose your balance.

Script 3: The Hardship Pivot

Best for: If you’ve missed a payment or are genuinely struggling

“I’ve hit a rough financial patch and I want to make sure I keep this account in good standing. My current interest rate is making that really difficult. Does [Bank Name] have a hardship program or a temporary rate freeze available to help me prioritize paying down the principal?”

Many issuers have formal hardship programs — temporary rate freezes, reduced minimums, even 0% for 6–12 months. They’re rarely advertised. You have to ask by name.

Script 4: The Escalation Play

Use this when the first rep says no

“I understand you may not have the authority to change my rate — I appreciate you checking. Is there a supervisor or someone in the retention department I could speak with? I want to make sure I’ve talked to someone who has full pricing authority before I decide what to do next.”

Frontline reps are often Tier 1 with limited authority. Retention departments have the actual pricing keys. Asking to be transferred is not rude — it’s the correct next move.

What to Do When They Say No

A “no” today isn’t a permanent no. Your playbook:

Ask for a partial win — “I understand on the rate — is there anything you can do about my annual fee this year?” A $95 fee waiver is mathematically identical to a 2% rate reduction on a $5,000 balance.

Ask for a temporary reduction — “Is a short-term rate reduction possible, even for 6 months? I’m working hard to pay this down and any help would mean a lot.”

The 90-Day Rule — Mark your calendar. Banking internal policies change quarterly. A “no” in April can become a “yes” in July with a different rep. Call back and say: “I called a few months ago about a rate reduction. My credit score has improved since then and I wanted to revisit this.”

Go for the balance transfer — If they won’t budge, a 0% APR promotional card is your move. The 3–5% balance transfer fee is usually far cheaper than months of 22% interest. On a $4,000 balance, a 3% fee costs $120 versus $880 in annual interest at 22%.

Apply for a lower-rate card — If your credit is solid, a new card with a better ongoing APR is a long-term fix. Don’t close the old card immediately — keeping it open preserves your credit utilization ratio and account age.

The Follow-Up — Don’t Skip This

Banks are notorious for “forgetting” to apply negotiated rates.

Get a reference number — Before you hang up, ask for the call’s reference number and the representative’s name. Write both down.

Watch for the Statement Drag — It typically takes 1–2 billing cycles for the new rate to appear. Check your next two statements specifically for the interest charge calculation.

If it doesn’t show up — Call back immediately with your reference number, the rep’s name, and the date of the original call. This resolves it quickly.

Don’t Reward the Win — This is the trap most people fall into. A lower interest rate is a tool to pay off the debt faster — not an excuse to spend more. If you lower your rate by 5% but increase your balance by 10%, you’ve handed the win straight back to the bank.

When to Call — And How Often

The best time to negotiate is from a position of strength — when your account is current and your credit is solid.

Best triggers to call:

- Your credit score has improved since you opened the card

- You’ve had the card 6+ months

- You just received a competing offer by mail or email

- You’re about to carry a larger balance than usual

- It’s been over a year since your last call

Ideal frequency: Once per year, per card. Rates change, your situation changes, and different reps have different authority levels.

Which Card to Call First

| Priority | Card to call | Why |

|---|---|---|

| 1st | Your oldest card | Highest Customer Lifetime Value — most leverage |

| 2nd | Highest APR card | Biggest savings per point reduced |

| 3rd | Largest balance card | Biggest absolute dollar savings |

| 4th | Cards you use most | Keeps future spending cheaper |

Work through the list one call per day. Keep a simple log — date, rep name, reference number, outcome.

FAQ

Does calling to negotiate hurt my credit score? No. This is a service request — no hard credit pull. Your score is unaffected whether they say yes or no.

What’s a realistic reduction to expect? Most successful negotiations result in 3–6 percentage points. On a $5,000 balance, 5 points saves approximately $250 per year according to published consumer finance research.

What if I’ve missed payments? Your leverage is lower but not gone. Use the hardship script. Issuers would often rather work with you than have you default — ask specifically about hardship programs and temporary rate freezes.

Should I threaten to cancel the card? Only if you’re genuinely prepared to follow through. An empty threat you don’t execute destroys your credibility for future calls. The competitor leverage approach — mentioning a specific real offer — is more effective and more honest.

Does this work for business credit cards? Yes. The same scripts work for business cards. Business card reps often have more flexibility because the balances and relationship value are typically higher.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: