What Happens If You Never Pay Credit Card Debt? The Real Answer (2026)

Quick Verdict: The Debt Decay Timeline

Let’s get the uncomfortable truth out of the way right up front: if you never pay your credit card debt, it doesn’t just disappear. It follows a very predictable path — late fees, credit damage, collections calls, and possibly a lawsuit — and it gets worse at every stage.

But here’s what the scary headlines usually leave out: there are legal time limits on how long creditors can actually come after you, and the damage on your credit report does eventually expire.

If you’re currently staring at a balance you can’t pay, you’ve probably encountered two types of advice: the horror story (“your life is over”) and the too-good-to-be-true version (“just ignore it and it goes away”). Neither is accurate. You won’t go to jail — debtors’ prisons haven’t existed in the U.S. since the 1830s. But you are entering a process we call the Debt Decay Timeline — the predictable lifecycle every unpaid credit card balance follows from missed payment to eventual resolution. Understanding it takes away a lot of the fear and gives you real leverage.

The Quick Verdict:

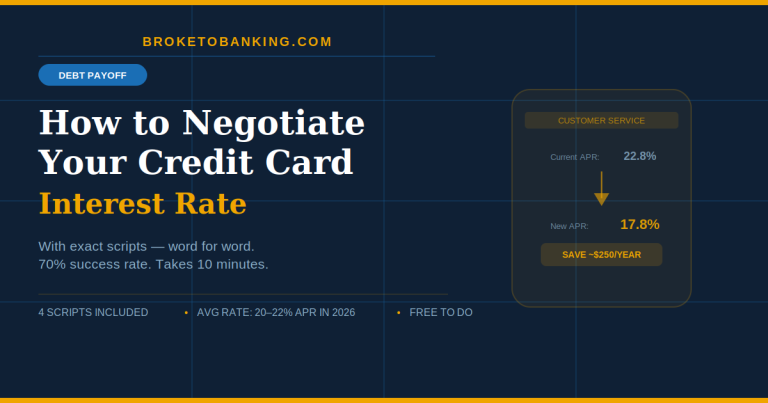

- STACK: Call for a Hardship Program ✅ — If you’re in trouble, call the issuer before you miss a payment. Many will drop your rate to 0–5% temporarily just to keep you from defaulting. This is the single highest-value move.

- RUNNER UP: Debt Validation — If your debt hits collections, don’t pay a cent until you send a Validation Letter. If they can’t prove they own the debt with proper documentation, they legally cannot collect.

- SKIP: The “Good Faith” Partial Payment ❌ — If your debt is already years old, making a small payment doesn’t help your score — it triggers the Clock Reset Trap, giving the creditor another 3–6 years to sue you.

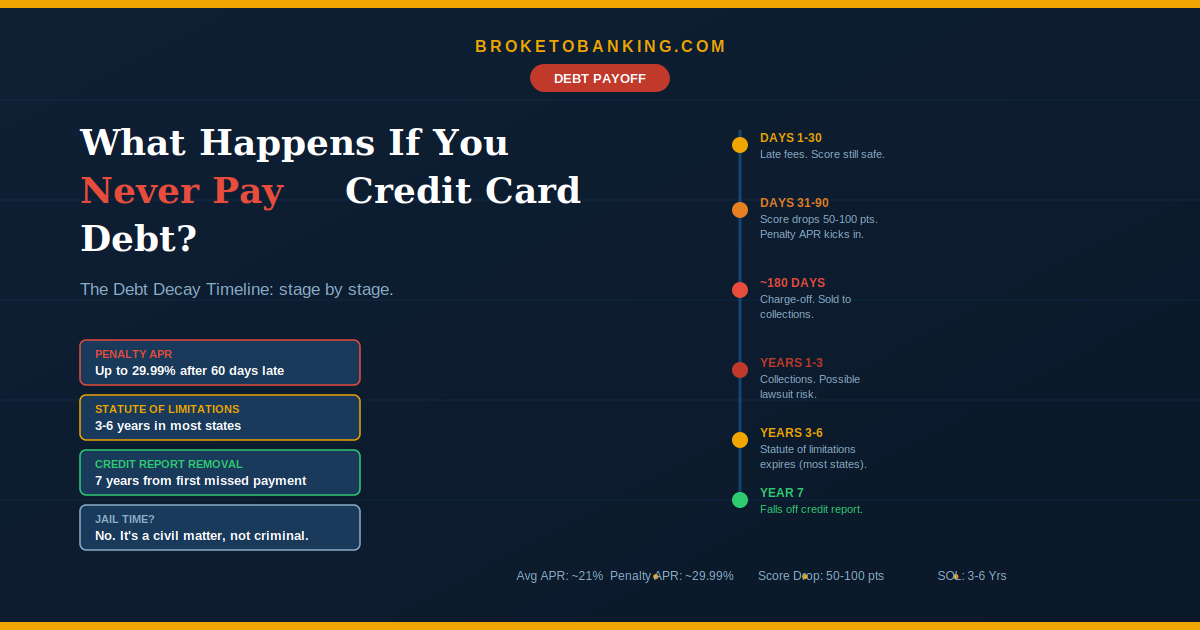

The quick timeline:

- Days 1–30: Late fees kick in. Your credit score is still safe if you catch up.

- Days 31–60: The credit bureaus get notified. Your score drops hard (50–100 points). Penalty interest rates start.

- Days 61–180: The balance balloons with fees and interest. The account is heading toward charge-off.

- After 180 days: The account is charged off and usually sold to collections. The original creditor writes it off.

- Years 3–6: The statute of limitations expires in most states. Creditors can no longer sue you.

- Year 7: The negative mark falls off your credit report completely.

Stage 1: Days 1–30 — The Late Fee Zone

The second your payment is even one day late, the issuer can hit you with a late fee. Right now those fees are usually $30 for the first offense and up to $41 for repeats within six billing cycles. (A 2024 CFPB rule trying to cap them at $8 has been blocked by a federal court, so the higher fees are still in effect.)

Here’s the part a lot of people miss: your credit score isn’t damaged yet. Credit card companies don’t report late payments to the bureaus until you’re 30 days past due. If you can scrape together even the minimum payment within that first month, you’ll eat the late fee but avoid any credit hit.

This is the cheapest and easiest stage to fix things. One $30 fee beats everything that comes next.

Stage 2: Days 31–90 — The Credit Damage Zone

Once you cross the 30-day mark, the account is officially delinquent and the issuer reports it to Equifax, Experian, and TransUnion. This is when the real damage starts.

A single missed payment can drop your credit score by 50–100 points, according to experts cited by U.S. News & World Report. And the higher your score was before, the harder the fall. Someone sitting at 780 might lose more points than someone already at 620.

Around the 60-day mark, most issuers also flip on the Penalty Rate Trap — your interest rate jumps to a penalty APR that can be as high as 29.99%. The average penalty APR across major issuers is approximately 27.29%, according to WalletHub. That means the balance you’re already struggling with starts growing much faster.

On a $5,000 balance, going from 21% to 29.99% adds roughly $450 a year in extra interest alone. Late fees keep stacking on top. This is where Interest Gravity — a concept we’ve covered in our debt payoff guide — takes over completely. The balance accelerates exactly when you’re least able to keep up.

The Skeptic’s Friction Report:

The Penalty Rate Trap is designed to be permanent. Under the CARD Act, issuers must review your account after six months of on-time payments and consider reducing the penalty APR — but they’re not required to actually reduce it. Many don’t.

Stage 3: Days 91–180 — The Charge-Off and the Phantom Tax

If you still haven’t caught up, the issuer is counting down to a charge-off, which usually happens around the 180-day mark — six months of non-payment.

A charge-off doesn’t mean the debt is forgiven. It just means the credit card company has decided they’re unlikely to collect from you directly, so they write it off as a loss on their books. You still owe the full amount.

What usually happens next: the original creditor either sends the account to a third-party collection agency or sells the debt outright to a debt buyer — often for as little as a few cents on the dollar. The buyers then try to collect the full balance from you, pocketing the difference as profit.

And then there’s the Phantom Tax. If a creditor forgives or writes off $600 or more of your debt, they’re required to report it to the IRS on a 1099-C form. The IRS may treat that forgiven amount as taxable income — meaning you didn’t get the money, but you could owe taxes on it as if you did. If you had $4,000 charged off, you could owe several hundred dollars in taxes at your marginal rate. This is the nasty surprise most people never see coming. If you’re heading toward a charge-off, consider setting aside money for the potential tax bill.

At this point your credit report shows both the original delinquency and a new collections entry. The damage is compounded.

Stage 4: Collections — The Pressure Campaign

Once the debt lands in collections, the calls and letters start. Debt buyers like Midland Credit Management and Portfolio Recovery Associates make their money by purchasing old debts cheap and collecting as much as possible from you. Their entire business model runs on persistence and pressure.

Your rights under the Fair Debt Collection Practices Act (FDCPA):

Collectors can’t call before 8 AM or after 9 PM. They can’t threaten arrest or use obscene language. They must stop contacting you if you send a written request. And if you ask for debt validation within 30 days of their first contact, they have to prove they own the debt, that the amount is correct, and that they have the legal right to collect it.

That validation step is powerful — many debts get sold multiple times between agencies, and errors accumulate along the way. If they can’t validate it, they have to stop collecting. Never pay a collector a single dollar until you’ve sent a Validation Letter and received proper documentation back. This is non-negotiable.

The Skeptic’s Friction Report:

Even with legal protections, dealing with collectors is stressful. They’re trained to create urgency and push boundaries. Some count on the fact that most consumers don’t know their rights. The single best move at this stage: put everything in writing. Phone calls are harder to document. Written communication creates a paper trail you can use if a collector crosses the line.

Stage 5: The Lawsuit Question — Can They Actually Sue You?

Yes, they can — and some creditors are aggressive about it. Research and consumer attorney reports indicate that Capital One and Discover are among the more litigious creditors when it comes to unpaid balances. Some major debt buyers are equally aggressive, filing lawsuits in bulk.

If a creditor or collector sues you, you’ll be served with legal papers. If you ignore them, the court can issue a default judgment against you. That judgment can lead to wage garnishment (your employer is ordered to send part of your paycheck to the creditor) or bank account levies (they can freeze and seize money from your account).

Never ignore a lawsuit. Showing up in court gives you a chance to negotiate, raise defenses, or set up a payment plan.

But there’s a hard deadline: Every state has a statute of limitations on credit card debt — a legal window after which creditors can no longer sue you. According to the CFPB and consumer law resources, most states set this at 3–6 years from the date of your last payment, though some go as long as 10 years.

| Statute of Limitations | States (Examples) |

|---|---|

| 3 years | North Carolina, New York, Maryland, Mississippi, and 9 others |

| 4 years | California, Texas, Pennsylvania, Ohio |

| 5 years | Colorado, Louisiana, Nebraska |

| 6 years | Connecticut, Illinois, Massachusetts, Michigan, New Jersey, Wisconsin |

| 10 years | Indiana, Iowa |

After that window closes, the debt is time-barred. Collectors can still ask you to pay voluntarily, but they can’t sue or threaten to sue you. If they do, it’s a violation of the FDCPA.

The critical warning — the Clock Reset Trap: In many states, even a small partial payment on old debt can restart the statute of limitations clock. A well-meaning $25 payment on a $3,000 debt that was about to expire can give the collector another 3–6 years to sue you. Collectors know this — some will deliberately try to get you to make a tiny “good faith” payment specifically to restart the clock. Never make a payment on old debt without first checking your state’s rules. According to the CFPB, acknowledging the debt or making a partial payment may restart the time period in some states.

Stage 6: Year 7 — The Credit Report Reset

No matter what you do (or don’t do), the Fair Credit Reporting Act limits how long negative items can stay on your credit report. For credit card delinquencies, charge-offs, and collections, the limit is seven years from the date of the original delinquency — the first missed payment you never caught up on.

After seven years, the entry must be removed automatically. You shouldn’t have to dispute it, but it’s smart to check your reports to make sure it actually disappears on schedule.

One key point: the seven-year credit reporting window and the statute of limitations for lawsuits are two separate clocks. They run independently. A debt can be past the statute of limitations but still on your credit report, or off your report but still within the lawsuit window.

Also important: paying or settling an old debt does not reset the seven-year reporting clock. The clock is tied to the original delinquency date, not any subsequent activity.

The Trended Data Warning: Even after a debt falls off your credit report, you may not be completely in the clear with every lender. In 2026, many lenders use scoring models like FICO 10T that analyze your payment behavior over time. And some issuers — American Express and Chase are widely reported examples — maintain internal records of customers who defaulted. These informal “blacklists” can reportedly prevent you from being approved for a new card with that specific issuer for 10–20 years, even after the debt has left your credit report entirely. The public score resets, but the institutional memory may not.

The Complete Debt Decay Timeline

| Timeline | What Happens | Credit Impact | Can They Sue? |

|---|---|---|---|

| Days 1–30 | Late fee charged | None (not reported yet) | No |

| Days 31–60 | Reported to bureaus, score drops 50–100 pts | Severe | Unlikely |

| Days 61–180 | Penalty APR, balance grows, heading to charge-off | Severe and worsening | Possible |

| ~180 days | Charged off, sold to collections | Major new negative entry | Yes |

| Years 1–3 | Collections calls, possible lawsuit | Ongoing damage | Yes (in most states) |

| Years 3–6 | Statute of limitations expires (varies by state) | Damage lessening | No (in most states) |

| Year 7 | Falls off credit report | Removed | Depends on state SOL |

So Should You Just Stop Paying?

I’m not going to tell you to strategically default on your credit cards. But I will be honest about the reality so you can make informed decisions.

When paying makes sense: If you can afford even the minimum payments, staying current avoids the entire cascade above. Minimum payments are expensive in interest, but they keep the system from turning against you.

When you genuinely can’t pay: If you’re choosing between rent and credit card payments, your housing comes first. Credit card debt is unsecured — there’s nothing for them to repossess. Call your issuer before you miss a payment and ask about hardship programs. Many will temporarily lower your interest rate, reduce payments, or offer deferrals if you’re dealing with job loss, medical issues, or other hardships. You’re more likely to get help while your account is still in good standing.

When the debt is already old: If you’re years into non-payment and the statute of limitations is approaching, making even a small payment can actually hurt you by triggering the Clock Reset Trap. At this stage, talking to a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC) or a consumer attorney is worth your time before you do anything.

FAQ

Can I go to jail for not paying credit card debt?

No. This is a civil matter, not criminal. You cannot be arrested or jailed for unpaid credit card debt. If a creditor sues you and wins a judgment, and you then ignore a court order related to that judgment (like failing to appear for a debtor’s examination), that could theoretically result in a contempt of court charge — but that’s about ignoring the court, not the debt itself.

Does unpaid credit card debt ever actually go away?

The credit reporting damage goes away after seven years. The statute of limitations on lawsuits expires after 3–10 years depending on your state. But technically the debt still exists until it’s paid, settled, or discharged in bankruptcy. After the statute of limitations expires, it becomes “time-barred” — creditors can still ask you to pay voluntarily, but they can’t sue.

What is a charge-off, and does it mean I don’t owe the money?

A charge-off means the issuer wrote the account off as a loss for their own books. It does not mean the debt is forgiven. You still owe it, and the issuer or a collector can still pursue it. It’s one of the most damaging entries that can appear on your credit report.

Should I pay a debt that’s already in collections?

It depends on your situation. If the statute of limitations has expired, paying could restart the legal clock in some states. If the debt is close to falling off your credit report (nearing the seven-year mark), paying won’t remove the negative mark any faster — and in some scoring models, a recently paid collection can actually look worse than an old inactive one. But if you’re planning to buy a house soon, many lenders require collections to be resolved first. A nonprofit credit counselor can help you weigh the specifics.

What’s the difference between the statute of limitations and the credit reporting time limit?

The statute of limitations (usually 3–6 years) determines how long a creditor can sue you. The credit reporting time limit (7 years under the FCRA) determines how long the negative mark stays on your credit report. They are two separate clocks that run independently. A debt can be past the statute of limitations but still on your credit report, or it can be off your report but still within the lawsuit window.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: