What Is Dollar-Cost Averaging? (Why Timing the Market Is a Myth)

Quick Verdict: It’s Investing the Same Amount on the Same Day, Every Month — No Matter What

If you’ve followed our advice to automate your investments — setting up a recurring $200/month into VTI or FZROX inside your Roth IRA — congratulations. You’re already doing dollar-cost averaging. You just didn’t know it had a name.

Dollar-cost averaging (DCA) means investing a fixed dollar amount at regular intervals regardless of whether the market is up, down, or sideways. $200 on the 1st of every month, no matter what. When prices are high, your $200 buys fewer shares. When prices drop, your $200 buys more shares at a discount. Over time, this lowers your average cost per share and removes the single biggest threat to your returns: your own emotions.

The alternative — waiting for the “right time” to invest — sounds smart but almost never works. People who sat out waiting for a dip in 2023 missed a 26% gain. Those who waited in 2024 missed another 25%. By early 2026, anyone who was “waiting for the dip” since 2023 had missed massive cumulative gains while sitting in cash. The market spends roughly 75% of its time going up. Waiting for a crash means sitting on the sidelines during most of the growth.

The Quick Verdict:

- STACK: Automate a fixed monthly investment — same amount, same day ✅ — This is DCA. Consistency beats timing.

- STACK: Keep investing during downturns — that’s when DCA helps most ✅ — Falling prices mean your fixed amount buys more shares at a discount.

- RUNNER UP: If you receive a windfall, invest most of it immediately — Lump sum beats DCA about 68% of the time (Vanguard). DCA the rest if you need to sleep at night.

- SKIP: “I’ll wait for the dip” ❌ — Time in the market beats timing the market. Every time.

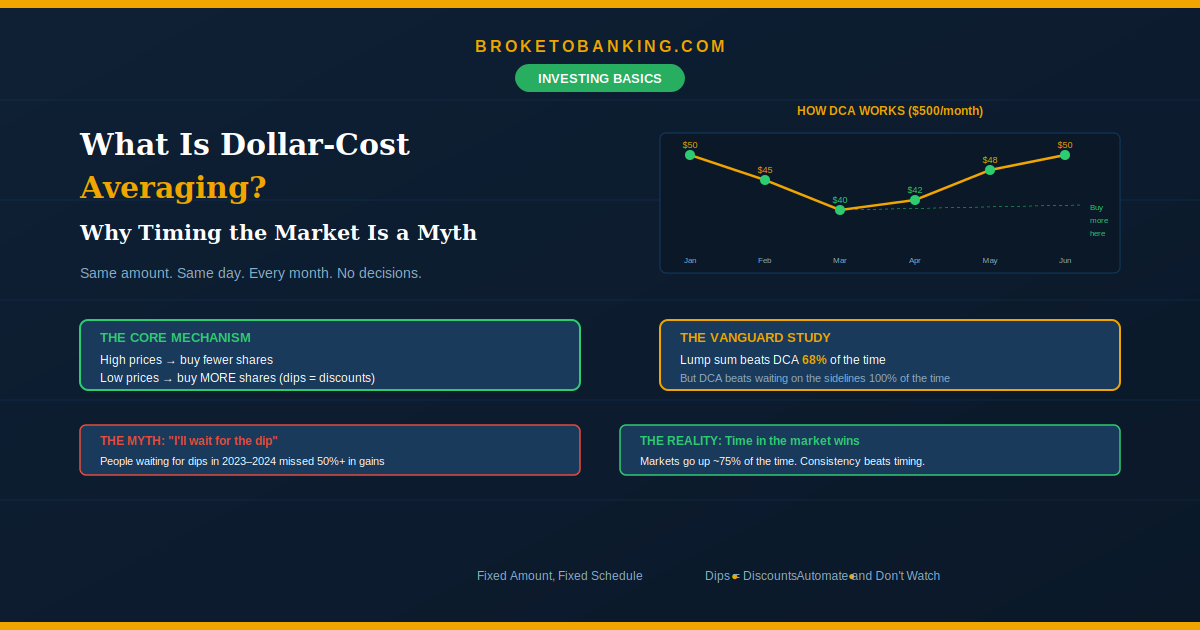

How It Actually Works (With Real Numbers)

Say you invest $500/month into an S&P 500 index fund over 6 months while prices fluctuate:

| Month | Share Price | $500 Buys | Shares Purchased |

|---|---|---|---|

| January | $50.00 | $500 | 10.0 shares |

| February | $45.00 | $500 | 11.1 shares |

| March | $40.00 | $500 | 12.5 shares |

| April | $42.00 | $500 | 11.9 shares |

| May | $48.00 | $500 | 10.4 shares |

| June | $50.00 | $500 | 10.0 shares |

| Total | $3,000 | 65.9 shares |

Your average cost per share: $3,000 ÷ 65.9 = $45.52

If you’d invested the full $3,000 in January at $50/share, you’d own 60 shares. With DCA, you ended up with 65.9 — nearly 10% more — because you bought more during the dips in February and March. The volatility that scares lump-sum investors actually worked in your favor.

This is the core mechanism: DCA turns market drops from something scary into a Black Friday discount.

Why “Waiting for the Dip” Is a Fantasy

This is the myth that quietly costs people the most money.

1. You don’t know when the dip is coming. Nobody does. Professional fund managers can’t time the market — that’s why 90%+ of them underperform the index over 20 years.

2. Even if you spot a drop, you probably won’t act. When the market actually crashes, the news is terrifying. Headlines scream recession. Your friends are selling. The “dip” you waited for feels like the start of a freefall, and you freeze.

3. Missing the best days is devastating. J.P. Morgan research shows that missing just the 10 best market days over 20 years cuts your total returns roughly in half. Most of those best days happen right after the worst days — during the exact moments when people are panic-selling.

DCA sidesteps all of this. You invest on your scheduled day no matter what. No decisions, no emotions, no CNBC.

The Honest Truth: Lump Sum Usually Wins the Math

Here’s the part most DCA articles leave out. According to Vanguard’s comprehensive study, lump-sum investing outperforms DCA roughly 68% of the time over rolling periods going back decades. Markets go up more often than they go down, so having more money in earlier generally produces better returns.

So why do we still recommend DCA? Because most of our readers aren’t choosing between “invest $20,000 today vs. spread it over 12 months.” They’re choosing between “invest $200 from this paycheck or spend it on junk.”

For most people, DCA isn’t a strategy — it’s the reality of having a job. You invest what you can, when you can. And the data is clear: consistent monthly investing crushes waiting on the sidelines.

The Peace of Mind Compromise: If you receive a windfall (inheritance, bonus, tax refund), the math says invest most immediately. If investing it all at once would make you anxious and likely to sell during the next downturn, use the hybrid approach: invest half now, DCA the rest over 3–6 months. The best strategy is the one you’ll actually stick to.

DCA + Automation = The Entire BrokeToBanking System

Dollar-cost averaging is the engine behind nearly everything we’ve built:

The Squeeze from our compound interest guide — $50–$200/month automated into an index fund. That’s DCA.

The Ghost Paycheck from Post #2 — automatic transfer on payday. DCA for your savings account.

DRIP (dividend reinvestment) from our index fund guide — reinvesting dividends at whatever the current price is. DCA on your returns.

401(k) payroll deductions — same amount every pay period, automatically invested. DCA by default.

If you’ve automated your finances using our automation guide, you’re already dollar-cost averaging across your entire financial life. You didn’t need to know the term — you needed the system.

The Skeptic’s Friction Report

DCA doesn’t protect you from long-term declines. If the market drops for 2 years, your portfolio shows losses during that period. DCA reduces timing risk, not market risk. But historically, every decline has recovered — and DCA lets you accumulate shares cheaply the whole way down.

Cash on the sidelines has a real cost. In 2026, you can park uninvested cash in a HYSA earning ~4.2%. That’s great for your emergency fund — but the S&P 500 can gain that much in a single quarter. Use HYSAs for safety. Don’t let them replace your wealth-building index funds.

DCA works best for patient, long-term investors. If you check your portfolio daily and panic when it’s red, automation helps — but you still have to trust the process.

Don’t DCA into individual stocks. DCA works because broad index funds always recover. If you DCA into a single company that goes bankrupt, you’re throwing good money after bad. Stick to the whole market — VTI, VOO, FZROX.

FAQ

Is DCA better than lump-sum investing?

Mathematically, no — lump sum wins about 68% of the time. Behaviorally, yes — DCA keeps people invested through volatility instead of panicking and selling. For most paycheck investors, DCA is the only realistic option anyway.

How often should I invest?

Monthly is the most common and practical — aligns with paychecks. Weekly or biweekly works too. The frequency matters far less than the consistency.

What if the market crashes right after I invest?

Good — that means your next monthly purchase happens at a Black Friday discount. A crash is only a loss if you sell. If you keep buying, you’re lowering your average cost.

Does DCA work with index funds?

It’s the ideal pairing. A broad index fund plus automatic monthly purchases is the simplest, most proven wealth-building system available to regular people. DCA into individual stocks is a Skip — stick to the whole market.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: