What Is an Index Fund? The Beginner’s Guide to Investing Without Overthinking It (2026)

Quick Verdict: It’s Owning a Tiny Piece of the Entire Market

We’ve been telling you to “buy a broad index fund” in pretty much every investing article on this site — our Roth IRA guide, investing apps breakdown, compound interest explainer, and Money Sequence. Today we’re explaining exactly what that means in plain English.

An index fund is a simple investment that automatically buys every stock in a specific market index — the S&P 500 (the 500 biggest U.S. companies) or the total U.S. stock market (4,000+ companies). Instead of trying to pick the next winners, you own a little slice of all of them. When the market rises, your money rises with it. When it drops, it drops too. But over the long haul, the market has grown about 10% per year on average for the S&P 500.

That’s really the whole idea. No guessing. No timing the market. No hoping you picked the next Tesla. Just low-cost, automatic ownership of the market itself.

The Quick Verdict:

- STACK: One broad index fund is enough to start ✅ — VTI, VOO, or FZROX. Buy it, automate monthly contributions, and let it run.

- STACK: Reinvest all dividends (DRIP) ✅ — If you’re pulling dividends out, you’re cutting your own compounding legs off.

- RUNNER UP: Add international exposure later — VXUS covers stocks outside the U.S. But one U.S. fund is a fine starting point.

- SKIP: Picking individual stocks as a beginner ❌ — You’re not trying to outsmart Wall Street.

- SKIP: Niche “hype” funds ❌ — If it’s a fund focused only on “AI Metaverse Crypto,” you’re probably buying at the top. Stick to the whole market.

How an Index Fund Actually Works

A “market index” is simply a list of stocks. The S&P 500 is the 500 largest public companies in America — Apple, Microsoft, Amazon, and so on. You can’t buy the list itself, so an index fund does it for you — it purchases every stock on that list, in roughly the same proportion as their size in the market.

Buy one share of an S&P 500 index fund, and you instantly own a tiny piece of all 500 companies. Apple has a killer quarter? You benefit. One company struggles? The other 499 soften the blow. That’s built-in diversification, and it’s why Warren Buffett and the entire Bogleheads community recommend index funds for most people.

The big insight: You’re not trying to beat the market. You are the market. And history shows that simply owning the market beats the vast majority of professionals. According to the SPIVA Scorecard, over 90% of actively managed large-cap funds underperformed the S&P 500 over 20 years — and even in single years, roughly 79% of managers fail to beat the index. They’re too busy trying to “time the Fed” while the index just keeps climbing. If the pros can’t beat it, don’t pay them to try.

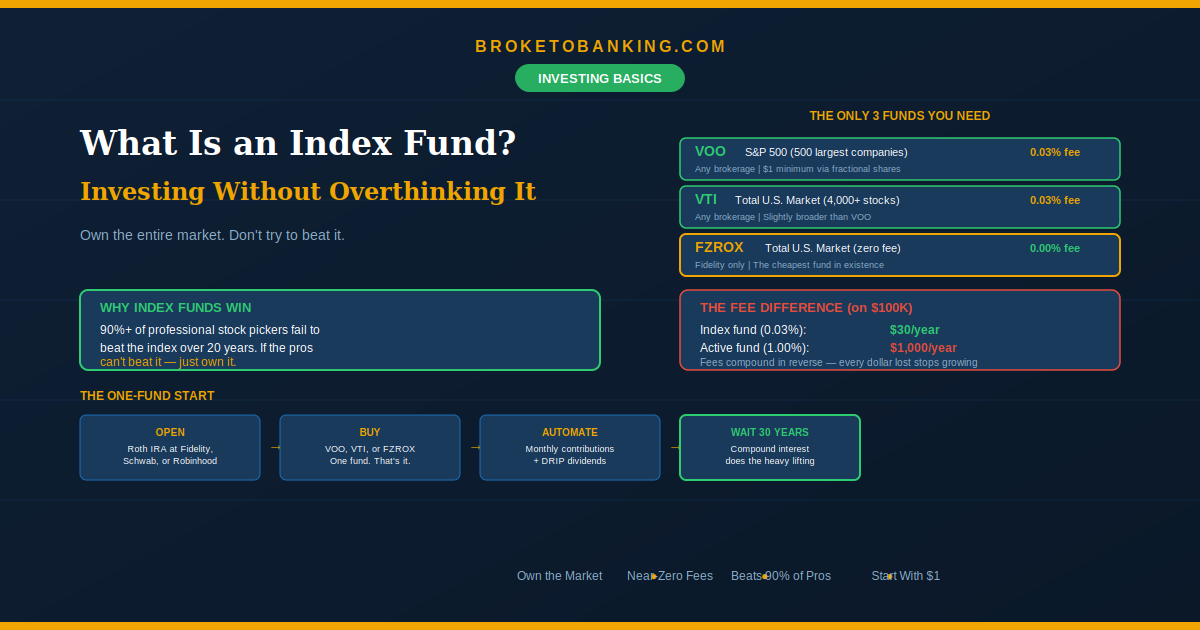

The Only Three Funds You Need to Know

| Fund | What It Tracks | Expense Ratio | Where to Buy |

|---|---|---|---|

| VOO | S&P 500 (500 largest U.S. companies) | 0.03% | Any brokerage |

| VTI | Total U.S. stock market (4,000+ stocks) | 0.03% | Any brokerage |

| FZROX | Total U.S. stock market | 0.00% | Fidelity only |

VOO vs. VTI: They perform very similarly because large companies dominate both. But here’s the 2026 reality: the S&P 500 is currently very top-heavy — roughly 30% of your money is concentrated in just a handful of Big Tech names. VTI adds 3,000+ smaller companies as a cushion if that concentration ever stumbles. For that reason, we slightly prefer VTI, but either one is an excellent starting point.

FZROX: Fidelity’s zero-fee option. Literally 0.00% expense ratio — the cheapest investing option in existence. If you’re at Fidelity, there’s no reason not to use it.

The One-Fund Start means exactly this: pick one, turn on automatic investments and dividend reinvestment (DRIP), and stop checking every day. You now own the entire U.S. market for essentially free.

Why Fees Matter More Than You Think

The expense ratio is the annual fee deducted automatically from your investment. It looks tiny. It’s not.

On a $100,000 portfolio, the difference between a 0.03% index fund and a 1.00% actively managed fund is $970/year. Over 30 years of compound growth, that Loyalty Tax to an expensive fund costs you over $150,000 in lost compounding. Every dollar taken in fees is a dollar that stops working for you. This is why we obsess over ultra-low-cost funds in every recommendation on this site.

ETF vs. Mutual Fund — Don’t Overthink It

ETF (like VOO, VTI): Trades like a stock throughout the day. Great for flexibility and fractional shares.

Mutual Fund (like FZROX): Priced once per day. Super easy for automatic monthly investments.

For most beginners automating a Roth IRA, it barely matters. Choose whatever feels simplest at your brokerage.

What About Risk?

Index funds aren’t risk-free. The market dropped 34% in 2020, nearly 50% in 2008. But every single major crash in history has eventually recovered. Money you won’t need for 5–10+ years belongs in the market. Short-term cash belongs in a HYSA.

The Skeptic’s Friction Report:

The biggest risk to an index fund isn’t a crash — it’s your behavior. The Check Frequency Tax is real: research shows the more often you check your account, the more likely you are to panic and sell at the bottom. And “I’ll wait for the dip to buy” is a fantasy — people waiting for a dip in 2025 missed significant gains while the index kept climbing. Time in the market beats timing the market. Set it to autopay, turn on DRIP, and forget the password. The Compound Interest Cheat Code requires patience above all else.

One more trap: Recency Bias. The S&P 500 returned roughly 26% in 2023 and 25% in 2024. That doesn’t mean it’ll do the same this year. Index funds are for money you don’t need for 10+ years. The long-term average is what matters, not last year’s number.

How to Buy Your First Index Fund (5 Minutes)

1. Open a Roth IRA at Fidelity, Schwab, or Robinhood. $0 minimum.

2. Deposit whatever you can — $50, $100, $500.

3. Search the ticker: VOO, VTI, or FZROX.

4. Buy with a market order. Fractional shares let you invest any dollar amount — don’t wait until you “have enough.”

5. Turn on DRIP (automatic dividend reinvestment).

6. Set up recurring monthly purchases. Even $50/month starts the chain. This is The Squeeze from our compound interest guide.

That’s it. Index funds are boring. They aren’t going to give you a 10x crypto win overnight. But they are the only proven way to turn a normal salary into a serious retirement. Stop overthinking it and just buy the market.

FAQ

Can I lose money?

Yes, in the short term. Markets drop regularly. But if you stay invested 10+ years and don’t sell during scary times, history shows you come out ahead.

How much do I need?

$1. Fractional shares and zero-minimum funds have removed every barrier.

VOO or VTI?

Both are excellent. VTI is slightly more diversified and less concentrated in Big Tech. You genuinely can’t go wrong with either.

International stocks?

A U.S. total market fund is a solid start. When ready, add VXUS (0.08% expense ratio) for global exposure. VTI + VXUS covers essentially the entire world.

Why not pick stocks?

Because 90%+ of professionals can’t beat the index over 20 years. Why gamble when you can own the whole market for near-zero cost?

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: