How to Pay Off Student Loans Faster in 2026 (Without Sacrificing Everything Else)

Quick Verdict: Your Interest Rate Determines the Urgency — Not Your Feelings

Student loans are the constant background hum of our reader’s financial life. The average borrower carries roughly $37,000–$40,000, and the national total sits near $1.8 trillion. It feels like a weight you’ll never shake. But the smartest strategy isn’t “throw every dollar at it until it’s gone” — it’s understanding exactly where your loans fit in the Money Sequence and making decisions based on math, not emotion.

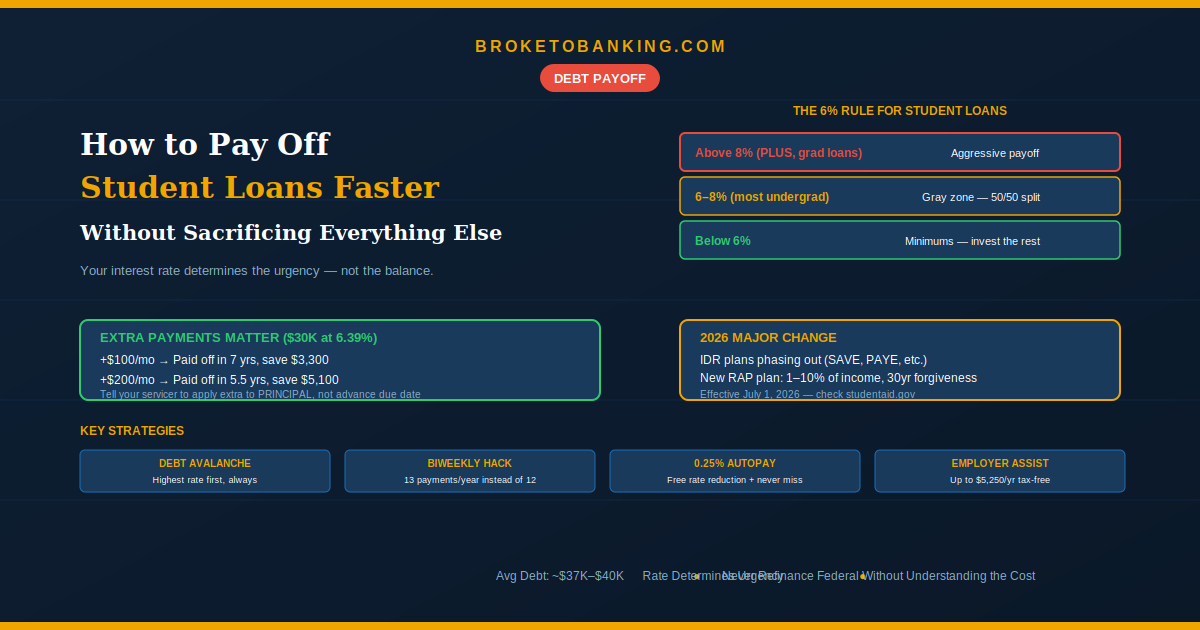

This is where the 6% Rule matters most: loans above ~6% are a Financial Leak that should be plugged aggressively before investing beyond the 401(k) match. Loans below 6% can ride alongside investing — minimums while your money works harder in a Roth IRA. The emotional pull to be debt-free is real, but a 5% loan doesn’t deserve the same urgency as a 22% credit card.

The Quick Verdict:

- STACK: Always capture the 401(k) match — even with student loans ✅ — That guaranteed 50–100% return beats any student loan rate.

- STACK: Attack loans above 6% using the Debt Avalanche ✅ — Paying off a 9% PLUS loan is a guaranteed 9% return. No index fund can promise that.

- RUNNER UP: Loans below 6% — minimums while you invest the rest — The market’s ~10% average beats your 5% interest.

- SKIP: Refinancing federal loans without understanding what you permanently lose ❌ — Forgiveness, IDR plans, interest subsidies, and borrower protections vanish forever.

Step 1: Know Exactly What You Owe

Log into studentaid.gov and list every federal loan. For private loans, check your lender portal or pull your credit report. Note the balance, interest rate, loan type, and servicer.

2026 federal rates:

- Direct Subsidized/Unsubsidized (undergrad): ~6.39%

- Direct Unsubsidized (graduate): ~7.89–8.89%

- PLUS Loans (parent/grad): ~8.89–9%

Map each against the 6% Rule:

| Rate | Action |

|---|---|

| Above 8% (PLUS, grad) | Aggressive payoff — treat like high-interest debt |

| 6–8% (most undergrad, some grad) | Gray zone — 50/50 split or lean toward payoff |

| Below 6% | Minimums — invest the difference |

Step 2: Set Your Repayment Strategy

The Avalanche (Recommended)

Same Debt Avalanche method: minimums on everything, every extra dollar to the highest-rate loan. When it’s dead, redirect to the next highest. This saves the most in interest — especially with a mix of 5% undergrad and 9% PLUS loans.

Extra Payments Matter

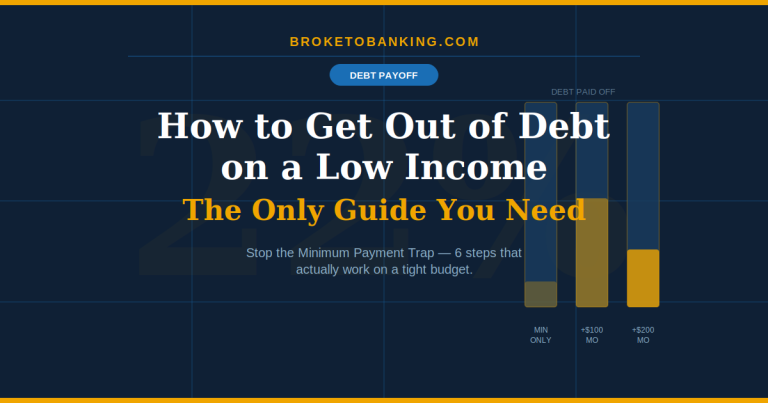

On a $30,000 loan at 6.39% (standard 10-year plan):

- Minimum only ($339/mo): $10,680 in total interest

- +$100/month ($439): Paid off in ~7 years, saving ~$3,300

- +$200/month ($539): Paid off in ~5.5 years, saving ~$5,100

The Due Date Trap: When you make extra payments, tell your servicer to apply them to principal, not to advance your due date. Most servicers default to advancing — which doesn’t reduce your interest. Call or set it in the portal. This is the single most common mistake borrowers make.

The Biweekly Hack

Pay half your monthly payment every two weeks. 52 weeks ÷ 2 = 26 half-payments = 13 full payments per year instead of 12. One extra payment annually, shaving months off the loan with almost no change to your daily budget.

The 2026 Repayment Landscape (Major Changes)

This is the biggest overhaul in decades. The “Big, Beautiful Bill” is phasing out existing Income-Driven Repayment plans — SAVE, PAYE, REPAYE, and ICR. A new Repayment Assistance Plan (RAP) takes effect July 1, 2026.

RAP key details:

- Payments capped at 1–10% of adjusted gross income

- Forgiveness after 30 years (up from 20 years under previous plans)

- Interest subsidy: If your RAP payment doesn’t cover your monthly interest, the government covers the shortfall. This prevents your balance from growing despite making payments — it effectively kills Interest Gravity for low-to-mid earners.

- PSLF remains intact — 120 qualifying payments (10 years) for government/nonprofit workers

The SAVE transition: If you were on the SAVE plan before the court-ordered shutdown, you’re in a 90-day transition window. Don’t let your servicer pick your plan by default — log into studentaid.gov and manually compare RAP vs. IBR (which may still offer 20-year forgiveness for some borrowers, a full decade shorter than RAP). Also expect servicer administrative errors during the transition. Audit your statements monthly through the rest of 2026.

The bottom line on RAP: If your income is low and you need the interest subsidy to survive, RAP is a Stack. If you’re a higher earner, the 30-year timeline is a Slow Tax — you’re better off using the Avalanche to kill the debt outright. Don’t rely on 30-year forgiveness. Three decades is a long time to carry a ghost.

Should You Refinance?

| Feature | Federal (2026) | Private (2026) |

|---|---|---|

| Interest rates | 6.39–9% (fixed) | 5–15% (variable/fixed) |

| Forgiveness | PSLF (10yr) / RAP (30yr) | None |

| Safety net | Subsidies, deferment, forbearance | Minimal |

| Repayment | 1–10% AGI under RAP | Fixed monthly |

Private loans at 8%+: Refinance if you have 670+ credit. Shop multiple lenders, target a shorter term.

Federal loans: Think very carefully. You permanently lose forgiveness, IDR, deferment, forbearance, and interest subsidies. With the OBBBA introducing new subsidy provisions under RAP, giving up federal protections for a 0.5% lower rate is a high-risk, low-reward gamble. Only refinance federal if you’re certain you don’t need protections AND can get a meaningfully lower rate.

Where Student Loans Fit in the Money Sequence

- 401(k) match — always first

- $1,000 Financial Armor — emergency buffer

- Credit card debt — 22% APR, pay off immediately

- Student loans above 6% — aggressive Avalanche

- HSA + Roth IRA — while making minimums on loans below 6%

- Increase 401(k) toward 15%

Your 9% PLUS loan gets the same urgency as credit card debt. Your 5% undergrad loan coexists with investing. The rate determines the priority — not the label.

Step 3: Use Every Advantage

- 0.25% autopay discount — free rate reduction + protects your credit score

- Employer repayment — up to $5,250/year tax-free. Ask HR.

- Windfalls — tax refunds, bonuses, side hustle income, salary negotiation wins go to the highest-rate loan first

FAQ

Pay off loans or invest?

Follow the 6% Rule. Above 6% → prioritize payoff. Below 6% → invest while making minimums. Gray zone → split 50/50 or lean toward payoff for peace of mind.

Do student loans affect credit?

On-time payments help (35% of your score). A missed payment is a Credit Nuke. Autopay solves this.

Should I count on forgiveness?

PSLF is solid if you qualify. The new RAP’s 30-year timeline is real but very long. Build your plan around payoff — treat forgiveness as a bonus.

How much extra should I pay?

At minimum, the required payment. Ideally +$100–$200/month to the highest-rate loan. Use the Loan Simulator at studentaid.gov to see how extra payments change your timeline.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: