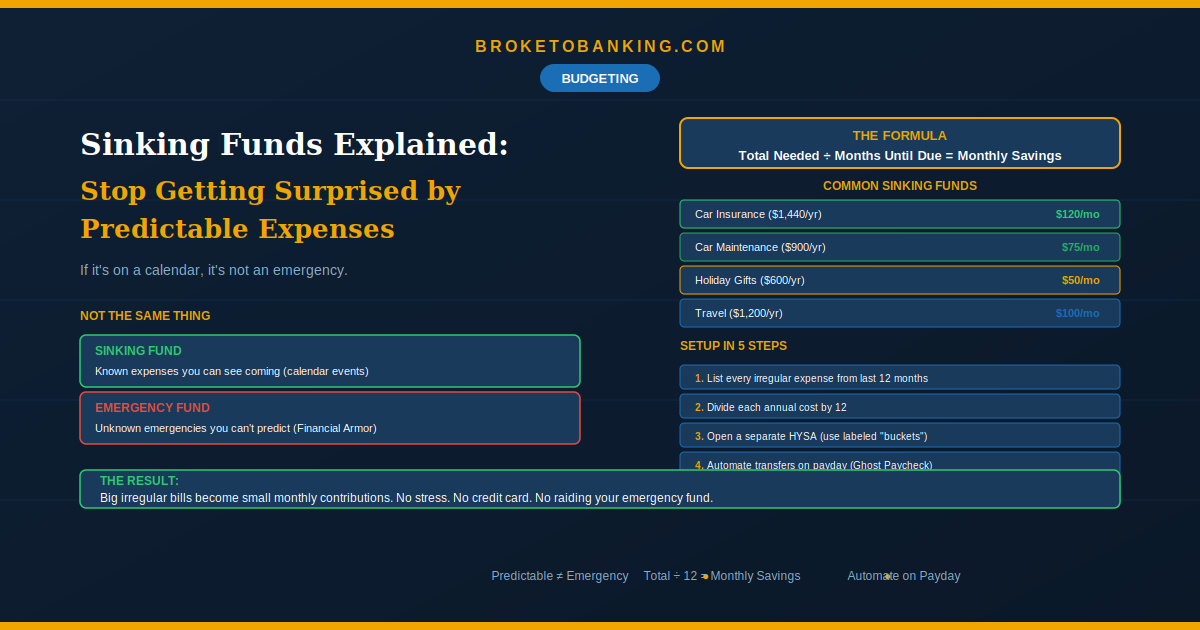

Sinking Funds Explained: Stop Getting Surprised by Predictable Expenses

Quick Verdict: If You Can Put It on a Calendar, It’s Not an Emergency

“We do fine with our budget… until something always comes up.” Christmas rolls around in December — every single year. Car insurance is due every six months like clockwork. Tires wear out. Subscriptions renew. None of these are surprises. They’re calendar events.

The real problem isn’t that these expenses show up. It’s that your budget doesn’t have a spot for them. So when the $600 car insurance bill lands, you pull from your emergency fund or throw it on a credit card at 22%. You’re using the wrong tool for a predictable problem.

A sinking fund fixes that. It’s money you set aside every month for a specific expense you know is coming. Big irregular bills become small monthly contributions. By the time the bill arrives, the money is already sitting there. No stress, no debt, no raiding the Financial Armor that’s meant for real surprises.

And in 2026, this is the Golden Age of Sinking Funds — with top HYSAs paying 4%+ APY, your parked cash is actually earning real money while it waits. $5,000 spread across your sinking funds generates roughly $200/year in passive interest. You’re not just saving for a bill — you’re getting a discount on it paid for by the bank.

The Quick Verdict:

- STACK: Set up sinking funds for every predictable irregular expense ✅ — If it’s on a calendar, it gets a fund.

- STACK: Automate contributions on payday ✅ — Same Ghost Paycheck philosophy.

- RUNNER UP: Keep them in a separate labeled HYSA — Use “buckets” (Ally, SoFi) for visual friction.

- SKIP: “Mental sinking funds” ❌ — If the money isn’t in a separate account with a label on it, it doesn’t exist. Keeping it “in your head” means it gets spent on Taco Tuesday.

How It Works (Dead Simple)

The formula: Total Amount Needed ÷ Months Until Due = Monthly Contribution

Example: Car insurance = $720, due every 6 months. $720 ÷ 6 = $120/month into your car insurance sinking fund.

When the bill arrives, pay it from the fund. Zero disruption. No credit card. No scrambling.

The Buffer Rule: Add 10% to your estimate. Premiums and costs rarely go down year-over-year. A $720 bill this year might be $790 next year. Budget $133/month instead of $120 and you’ll always have a cushion.

The Sinking Funds Most People Need

Start with the ones that have bitten you before:

| Sinking Fund | Annual Cost (est.) | Monthly Contribution |

|---|---|---|

| Car insurance (biannual) | $1,440 | $120 |

| Car maintenance & repairs | $900 | $75 |

| Holiday gifts & birthdays | $600–$800 | $50–$67 |

| Annual subscriptions & renewals | $480–$600 | $40–$50 |

| Medical/dental copays | $600 | $50 |

| Clothing & shoes | $480 | $40 |

| Travel/vacation | $1,200 | $100 |

| Pet care | $500 | $42 |

Note: Full-coverage auto insurance averages higher (~$2,200–$2,500/year in 2026). Adjust your fund to match your actual premiums. Subscription creep is the silent 2026 budget killer — audit yours before setting the number.

You don’t need every fund on day one. Start with 2–3 that cover your biggest irregular expenses. Add more as your margin grows.

Sinking Fund vs. Emergency Fund (Not the Same Thing)

| Sinking Fund | Emergency Fund | |

|---|---|---|

| For | Known, predictable expenses | Unknown, unexpected emergencies |

| Examples | Insurance, holidays, car maintenance | Job loss, medical crisis, major repair |

| Timing | You know when it’s coming | No idea when it’ll hit |

| Replenishment | Naturally refilled by monthly contributions | Rebuilt using the Replacement Protocol |

Your emergency fund is Financial Armor — protection against genuine surprises. Sinking funds handle everything you can see on the calendar. Mix them up and both systems break.

How to Set Them Up (One Afternoon)

Step 1: The Calendar Audit. Go through 12 months of bank statements. Flag every non-monthly bill: insurance, subscriptions, car work, holidays, medical, travel. Write down the annual amount for each.

Step 2: Divide by 12 (+ the 10% buffer). Each expense becomes a monthly budget line item.

Step 3: Open a separate HYSA. Keep sinking funds away from checking — Checking Account Gravity will consume them otherwise. Banks like Ally and SoFi let you create labeled “buckets” within one account so you don’t need six separate accounts. The visual labels create friction — you’re less likely to raid the “Car Insurance” bucket for an impulse purchase.

Step 4: Automate transfers on payday. Set the transfer to trigger within hours of your direct deposit. If money stays in checking past lunch, it’s already gravitating toward a random Amazon purchase. The Ghost Paycheck approach: money moves before you see it.

Step 5: When the expense hits, pay from the fund. Transfer what you need back to checking, pay the bill, and move on. No drama.

The First Year Is the Hardest

Sinking funds take a full cycle to mature. If your $720 car insurance is due next month and you just started, you won’t have $720. Cover the gap from savings this one time.

After the first year, the system runs on its own. Every future bill is pre-funded. The roller coaster of high-expense months and low-expense months flattens into a consistent monthly budget. That’s the whole point — turning Financial Chaos into Mechanical Certainty.

The Skeptic’s Friction Report

“That’s a lot of monthly contributions.” It is. But you’re already paying these expenses — you’re just doing it reactively (often with credit card interest) instead of proactively with pre-saved cash. Total cost stays the same. The timing changes.

“I don’t have margin for sinking funds.” Start with one. The expense that hurt you most last year gets a fund. Even $25/month toward holidays means you enter December with $300 instead of $0. As your margin grows — through lowering bills, killing debt, or negotiating a raise — add more.

“Can I just use one fund for everything?” You can, but labeled funds work better. Seeing “$120 for car insurance” and “$50 for gifts” keeps you honest. One big pot gets raided.

FAQ

Are sinking funds the same as savings goals?

Essentially. A sinking fund is a savings goal with a specific purpose and usually a deadline. “Save $1,200 for vacation by June” is a sinking fund. “Save more money” is a vague wish.

Where should I keep them?

A high-yield savings account separate from checking. Labeled sub-accounts or “buckets” make tracking easy.

How many should I have?

Start with 2–3. Expand to 6–8 once the system is running. More than that gets hard to manage.

What if I don’t use all the money?

It rolls over. Extra car maintenance money this year becomes a bigger cushion for next year. Nothing is wasted.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: