What Is a Target-Date Fund? (The “Set It and Forget It” Retirement Option)

Quick Verdict: It’s the Easy Button for Retirement Investing

We’ve told you to buy broad index funds and automate through dollar-cost averaging. That’s the DIY path — and it works. But some people want the truly zero-decision option: one fund, no rebalancing, no thinking. That’s a target-date fund.

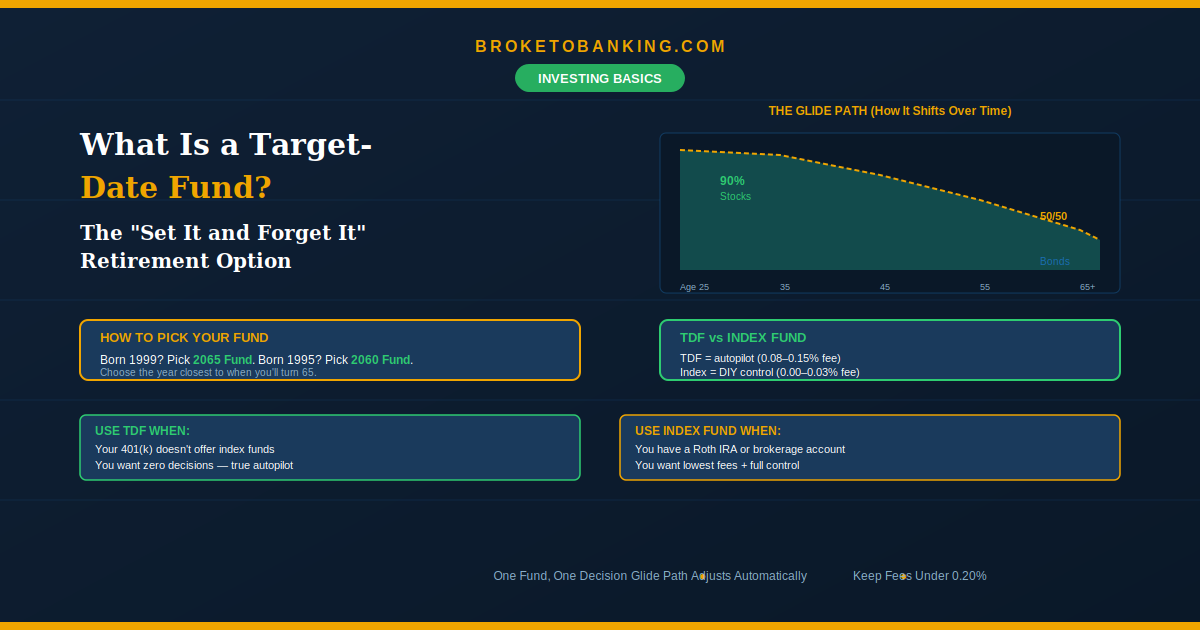

A target-date fund (TDF) is a single mutual fund that holds a diversified mix of stocks, bonds, and other investments — then automatically adjusts that mix as you approach retirement. When you’re 27, the fund is mostly stocks. As you near 65, it gradually shifts toward bonds and cash. You don’t touch anything. The fund manager handles the rebalancing on a predefined schedule called a “glide path.”

Pick the year closest to when you plan to retire — 2060, 2065, whatever — and invest. That’s it. If you were auto-enrolled in a 401(k) and never changed the default, there’s roughly a 90% chance you already own one. In 2026, TDFs manage trillions in assets for a simple reason: they remove the decision-making friction that keeps most people from investing in the first place.

The Quick Verdict:

- STACK: Low-cost TDFs (under 0.15%) in your 401(k) ✅ — If your plan doesn’t offer a total market index fund, this is your best default.

- STACK: Pick the fund closest to the year you turn 65 ✅ — Born 1999? Pick 2065. Born 1995? Pick 2060.

- RUNNER UP: If you want more control + lower fees, use index funds directly — Our One-Fund Start at 0.03%.

- SKIP: TDFs over 0.20% — and watch for the Active vs Index trap ❌ — More below.

How the Glide Path Works

The glide path is what makes a TDF different from a regular index fund. It’s the automatic shift from aggressive to conservative:

| Your Age | Years to Retirement | Typical Allocation |

|---|---|---|

| 25–35 | 30–40 years | ~90% stocks / 10% bonds |

| 35–45 | 20–30 years | ~80% stocks / 20% bonds |

| 45–55 | 10–20 years | ~65% stocks / 35% bonds |

| 55–65 | 0–10 years | ~50% stocks / 50% bonds |

| 65+ | In retirement | ~30–40% stocks / 60–70% bonds |

When you’re young and have decades of compounding ahead, the fund stays heavy in stocks — the Compound Interest Cheat Code needs growth to work. As retirement approaches, the fund reduces stock exposure to protect your nest egg. You never adjust. The fund does it automatically.

A single target-date fund is more diversified than almost any other investment you can hold — it owns thousands of U.S. stocks, international stocks, and bonds across the globe, all in one package.

Target-Date Fund vs. Index Fund

| Target-Date Fund | Index Fund (VTI/VOO) | |

|---|---|---|

| Decision-making | Zero — pick a year and invest | Minimal — pick fund, automate |

| Rebalancing | Automatic (glide path) | Manual (or never — many stay 100% stocks) |

| Expense ratio | 0.08–0.15% (best options) | 0.00–0.03% |

| Bond allocation | Automatically adds bonds as you age | You decide when/if to add bonds |

| Best for | 401(k) defaults, true beginners | Roth IRA, people wanting max control + lowest fees |

The honest take: If you’re in your 20s–30s using a Roth IRA, an index fund at 0.03% beats a TDF at 0.12% — the fee gap compounds over decades. But if your 401(k) only offers TDFs and actively managed funds, the TDF is almost always the best option on the menu.

The hybrid strategy: Many investors use a TDF in their 401(k) and index funds in their Roth IRA. This balances ease-of-use with fee optimization — and it works great.

The Active vs. Index Trap (Read This Carefully)

This is the most expensive mistake in 401(k) investing. Some providers offer two versions of their target-date fund with nearly identical names:

Example: Fidelity has a “Freedom Fund” (actively managed, ~0.70%) and a “Freedom Index Fund” (passively managed, ~0.12%). The name looks almost the same. The fee difference over a 40-year career costs you $100,000+.

The rule: Always look for the word “Index” in the fund name. If your plan offers both, pick the index version every time.

2026 fee benchmarks:

| Provider | Fund | Expense Ratio |

|---|---|---|

| Vanguard | Target Retirement | 0.08% |

| Schwab | Target Index | 0.08% |

| Fidelity | Freedom Index | 0.12% |

| Industry average | All TDFs | ~0.27% |

Anything over 0.20% — question it. Over 0.50% — look for alternatives.

The Skeptic’s Friction Report

The convenience fee is real. A TDF at 0.12% costs more than VTI at 0.03%. On $100,000 over 30 years, that 0.09% gap costs roughly $10,000. On a $1 million portfolio, the autopilot costs $500–$1,000/year. If you’re willing to spend one hour a year rebalancing a DIY portfolio, you keep that money. For most 401(k) investors who’d otherwise pick random funds or leave cash in a money market, it’s worth the fee.

The Bond Drag. In your 20s and 30s, TDFs hold ~10% bonds. In a high-growth market, those bonds act as a drag on returns. Most DIY investors stay 100% stocks until their 40s to maximize the Compound Interest Cheat Code. The TDF’s conservative start costs you some growth in exchange for less volatility. Whether that trade-off matters to you depends on your stomach for market drops.

One Size Fits None. A 2065 fund treats every investor the same — whether you have a pension, a spouse with big savings, or plan to work until 70. It doesn’t know your complete picture. For most people, that’s fine. For complex situations, a DIY approach or advisor may serve better.

You’re not truly “forgetting it.” You still need to contribute consistently, increase contributions over time (auto-escalation), and verify you’re in the right year’s fund. “Set it and forget it” means the allocation is on autopilot — not your savings rate.

FAQ

I’m 27. Which fund?

Born 1999 + 65 = 2064. Pick the 2065 fund. Want slightly more aggressive? Pick 2070.

What if I want to retire early?

Pick an earlier target date — the glide path shifts to conservative sooner.

Can I have a TDF AND index funds?

Yes. TDF in the 401(k), index funds in the Roth IRA. Solid hybrid strategy.

Are they “safe”?

No investment is risk-free. TDFs hold stocks, which can drop hard in any year. In 2008, near-retirement TDFs lost 20–30%. They reduce risk over time — they don’t eliminate it.

My 401(k) TDF charges 0.60%. Too high?

Yes — 5–7x what the best ones charge. Check if there’s a cheaper index fund or index TDF. If the 0.60% fund is the only diversified option, it’s still better than a money market earning almost nothing.

Is it safe to have 100% of my 401(k) in one TDF?

Actually, yes — a TDF is more diversified than almost any single investment. It holds thousands of stocks and bonds across the globe. “One fund” doesn’t mean “one stock.”

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: