How to Improve Your Credit Score by 100 Points in 6 Months (2026)

Quick Verdict: The Score Lever System

If you’re looking at a credit score in the 500s or low 600s, you aren’t just “unlucky” — you’re being systematically overcharged. In 2026, a 100-point gap can mean the difference between a reasonable mortgage rate and one that costs you tens of thousands extra. Your credit score isn’t a grade on your character — it’s a mathematical algorithm. To scale the 100-Point Wall in 180 days, you need to manipulate the levers that the algorithm prioritizes.

We call this the Score Lever System — a prioritized plan that attacks the highest-impact factors first. According to FICO’s Spring 2026 Credit Insights report, the average FICO score is 714. If you’re significantly below that and willing to be disciplined for six months, a 100-point jump is realistic — especially starting in the 500s or low 600s where there’s more room to move.

The Quick Verdict:

- STACK: Pay down credit card balances to get utilization under 10% ✅ — The single fastest lever. Utilization updates every billing cycle — score changes within 30 days.

- STACK: Dispute credit report errors ✅ — The FTC found 1 in 5 consumers has a confirmed material error. You’re paying a Success Tax for the bank’s bad data.

- RUNNER UP: Set up autopay on every account — One missed payment is a Credit Nuke that costs 50–100 points. Autopay is cheap insurance.

- SKIP: “Credit repair” companies ❌ — In 2026, you’ll see ads for “Credit Repair AI.” They charge $100/month to send dispute letters you can download for free.

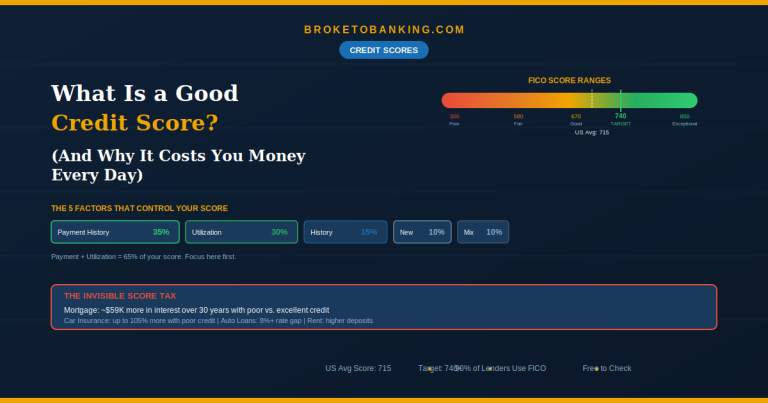

The Five Score Levers

Your FICO score comes from five categories. Here’s the breakdown according to myFICO:

| Score Lever | Weight | Speed of Impact |

|---|---|---|

| Payment History | 35% | Slow (needs months of consistency) |

| Credit Utilization | 30% | Fast (updates every billing cycle) |

| Credit History Length | 15% | Very slow (years) |

| New Credit | 10% | Medium (inquiries fade in 12 months) |

| Credit Mix | 10% | Slow (don’t open accounts just for this) |

65% of your score comes from just two factors. The other three are Background Levers — they reward patience, not action. Don’t waste time on credit mix while you still have big wins on utilization and payment history. Pull the big levers first and stop paying the Invisible Score Tax — the daily cost of a low score across loans, insurance, and deposits.

Month 1: The Utilization Blitz

The Verdict: STACK ✅ — Target: 30–50 points in 30 days

Credit utilization is the single fastest lever you can pull. The critical detail: utilization has no memory. The algorithm only sees your current reported balance. Pay off your cards today, your score updates within one billing cycle.

The average American’s utilization sits at about 35.5%, according to FICO’s 2025 Credit Insights — above the 30% penalty threshold. People with the highest scores keep utilization under 10%.

The Utilization Sprint Protocol

1. Pay before the statement closing date — not the due date. Your issuer reports the balance on the closing date. Pay a few days before and a lower number gets reported.

2. Target the highest-utilization cards first. Per-card utilization matters. One maxed-out card hurts more than two at 40% each.

3. The Denominator Play — request credit limit increases. If they raise your limit from $2,000 to $5,000 and your balance stays at $1,000, utilization drops from 50% to 20% instantly. Ask whether it’s a hard or soft pull before agreeing.

4. Don’t close old cards with zero balances. Closing reduces total available credit, pushing utilization higher. Keep them active with a small recurring charge.

Month 1–2: The Error Audit

The Verdict: STACK ✅ — Target: 0–100 points (if errors exist)

The FTC found about 1 in 5 consumers has a confirmed material error on at least one credit report. About 5% had errors serious enough to affect loan terms.

Pull all three reports free at AnnualCreditReport.com (still free weekly through 2026). Scan for accounts that aren’t yours, incorrect late payments, wrong balances or limits, duplicate collections, and Zombie Debts — accounts that should have aged off after seven years but are still lingering.

Dispute directly with the bureau online and include documentation. Also dispute with the company that reported the error. Both must investigate within 30 days under the FCRA. For collections, send a Debt Validation Letter before paying anything — if they can’t prove they own the debt, they must remove it.

Months 1–6: Payment History + Autopay Shield

Target: 20–50 points over six months

Payment history is 35% of your score but can’t be fixed overnight. Set up autopay for at least the minimum on every account — this is your Financial Safety Net against the single most expensive credit mistake. If you’re worried about overdrafts, autopay the minimum and manually pay more when you have cash.

Late payments stay on your report for seven years but fade over time. A late payment from four years ago hurts far less than one from four months ago. The strategy: bury old damage under a stream of new on-time payments.

Goodwill letter option: If you have a single late payment on an otherwise clean account, a polite letter to the creditor asking for removal works often enough to be worth trying.

Months 2–4: The Authorized User Shortcut

Target: 10–50 points (highest for thin-file individuals)

Ask a trusted family member with excellent credit to add you as an authorized user on an old, low-utilization card. Their payment history and credit limit get grafted onto your report. You don’t need the physical card — the reporting alone matters.

The ideal card: 5+ years old, under 10% utilization, perfect payment record, high limit. Only do this with someone whose credit behavior you trust completely — their mistakes will hurt your score too.

Months 3–6: The Advanced Plays

Experian Boost: Free tool that adds utility, phone, streaming, and rent payments to your Experian file. Average increase: 13 points.

The Trended Data Strategy: FICO 10T examines your balance trajectory over 24 months. Flat balances signal Debt Persistence. Even $10 above the minimum creates a downward slope the model reads as de-leveraging. Start the pattern now.

Application timing: Each hard inquiry costs 3–5 points. Multiple inquiries for the same loan type within 14 days count as one. Avoid scattered applications.

The 6-Month Roadmap

| Month | Action | Expected Impact |

|---|---|---|

| 1 | Pay balances to under 10% utilization | 30–50 pts |

| 1 | Pull reports, dispute errors | 0–100 pts (if errors) |

| 1 | Set up autopay on everything | Prevents damage |

| 2 | Credit limit increases (Denominator Play) | 5–20 pts |

| 2–3 | Authorized user on trusted card | 10–50 pts |

| 3 | Experian Boost | ~13 pts |

| 1–6 | On-time payments + declining balances | 20–50 pts cumulative |

Realistic expectations: Starting in the 500s, 50–100+ points is realistic with aggressive action. Starting in the 600s, expect 30–60 points. Starting in the 700s, 10–30 points — at that level, avoiding mistakes matters more than adding strategies.

FAQ

Can I really raise my score 100 points in six months?

If you start in the low 500s or 600s with high utilization, credit report errors, or addressable negative marks, yes. If you’re already in the high 600s or 700s with a clean report, gains will be smaller and slower.

What’s the single fastest way to improve my score?

Paying down credit card balances. Utilization is the only major factor that updates every billing cycle. You can see changes within 30 days.

Should I pay for a credit repair company?

Almost never. Everything they do — disputes, validation letters, bureau correspondence — you can do for free. The only exception: identity theft or complex mixed-file issues where a consumer rights attorney adds real value.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: