What Is Compound Interest? The Beginner’s Guide to Growing Money While You Sleep (2026)

Quick Verdict: It’s Interest on Your Interest (And It Changes Everything)

Compound interest is the single most important concept in personal finance. We’ve called it the Compound Interest Cheat Code across multiple posts — and in 2026, with inflation still a nagging reality, it’s the only way to ensure your money doesn’t just sit there but actually works.

Here’s the simplest definition: compound interest is earning interest on your interest. Your money earns returns. Then those returns earn returns. Then those returns earn returns. The cycle never stops, and the longer it runs, the faster it accelerates. It’s the reason a 25-year-old who invests $200/month can end up with more money at 65 than a 35-year-old who invests $400/month. Time is the multiplier.

But here’s what most compound interest articles won’t tell you: it works both ways. When you’re investing, compound interest builds your wealth while you sleep. When you’re carrying credit card debt at 22% APR, compound interest is building the bank’s wealth while you sleep — at your expense. You can’t outrun a 22% interest fire with a 10% market return. Understanding which side of this equation you’re on is the difference between financial freedom and financial quicksand.

The Quick Verdict:

- STACK: Start investing as early as possible — even $5 ✅ — Time matters more than the dollar amount. $50/month at 25 beats $200/month at 35.

- STACK: Reinvest everything — dividends, interest, gains ✅ — Every dividend you pull out is a Success Tax you’re paying yourself today at the cost of your future.

- RUNNER UP: Use tax-advantaged accounts — A Roth IRA lets compound interest work completely tax-free.

- SKIP: Waiting until you “have enough” to start ❌ — In 2026, fractional shares mean there is no barrier. Every month you wait is a month of compounding you’ll never get back.

How It Actually Works (With Real Numbers)

The difference between simple interest and compound interest is the difference between a ladder and a rocket ship.

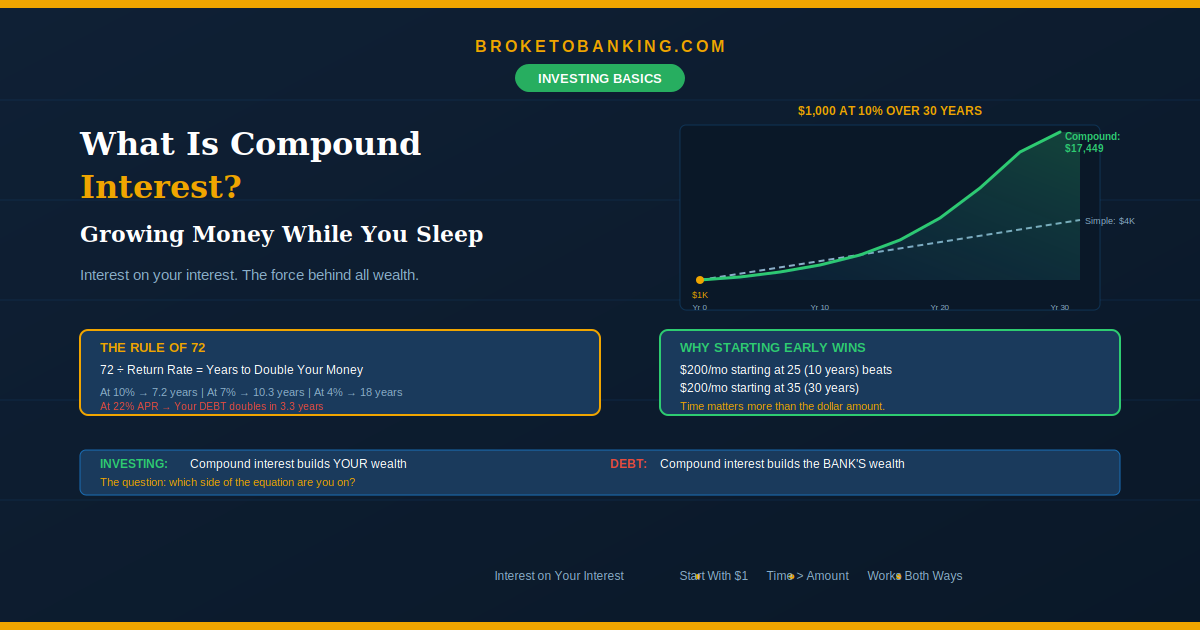

Simple interest: You earn interest only on the original amount. $1,000 at 10% = $100/year, every year. After 30 years: $4,000.

Compound interest: You earn interest on the original amount plus all the interest that’s already accumulated. Same $1,000 at 10%:

| Year | Balance (Simple) | Balance (Compound) |

|---|---|---|

| 1 | $1,100 | $1,100 |

| 5 | $1,500 | $1,611 |

| 10 | $2,000 | $2,594 |

| 20 | $3,000 | $6,727 |

| 30 | $4,000 | $17,449 |

Same $1,000. Same 10% rate. Same 30 years. Simple interest: $4,000. Compound interest: $17,449. The difference — over $13,000 — came entirely from interest earning interest. The growth isn’t linear. It’s exponential. It starts slow, feels invisible for the first few years, and then accelerates dramatically. The magic happens in the later years, which is exactly why starting early matters so much.

The Rule of 72: A Mental Shortcut

Want to know how long it takes your money to double? Divide 72 by your annual return rate.

- At 4.2% (HYSA): 72 ÷ 4.2 = ~17 years to double

- At 7% (balanced portfolio): 72 ÷ 7 = ~10 years to double

- At 10% (S&P 500 historical average): 72 ÷ 10 = ~7.2 years to double

- At 22% (credit card APR): 72 ÷ 22 = ~3.3 years for your debt to double

That last one is why credit card debt is so dangerous. At 22% APR with minimum payments, your balance is working against you at the same compounding speed that builds wealth for investors. This is Interest Gravity — compound interest in reverse, pulling you into financial quicksand. It’s why our Money Sequence is non-negotiable: kill high-interest debt before you invest heavily.

Why Starting Early Beats Starting Big

This is the most counterintuitive part — and the most important for our readers.

Scenario A: You invest $200/month starting at age 25, for 10 years only (total invested: $24,000). Then you stop contributing entirely. Your money compounds at 8% until age 65.

Scenario B: You invest $200/month starting at age 35, every month for 30 years straight (total invested: $72,000) at the same 8% return until age 65.

Result: Scenario A — the person who invested less money but started earlier — ends up with more at 65. The 10 extra years of compounding on the early contributions outweigh 20 additional years of new contributions.

$50/month at 25 is worth more than $200/month at 35. Every year you wait isn’t just a year lost — it’s the most valuable compounding year you’ll ever have, because it has the longest runway.

Compound Interest Works Against You Too

Credit cards compound interest daily. At 22% APR, a $5,000 balance grows by roughly $3 per day in interest. If you only pay the minimum, you’ll pay over $7,000 in interest alone over the next two decades — more than the original balance.

This is why our Money Sequence puts killing high-interest debt before investing (after capturing the 401(k) match). When compound interest is working against you at 22%, eliminating it is the best guaranteed return available. You’re essentially earning 22% risk-free by paying off the debt. The same force that makes investing powerful makes debt devastating. The question is always: which side are you on?

The 2026 Action Plan: Putting the Cheat Code to Work

1. Capture the 401(k) match. Your employer’s match is a 100% return — the ultimate compounding starter. See our 401(k) guide.

2. Open and fund a Roth IRA. The 2026 limit is $7,500. In a Roth, your compound interest works completely tax-free — the IRS doesn’t get a cut of your growth. See our Roth IRA guide.

3. Automate “The Squeeze.” Even $50/month into a Total Market Index Fund (like VTI) starts the chain. Use Fidelity or Robinhood — fractional shares let you invest with $1. The One-Fund Start gives you instant diversification.

4. Turn on DRIP. Set your brokerage to automatically reinvest dividends. Every dividend that gets reinvested is another soldier in the field working for you. Pulling dividends out breaks the compounding chain.

5. Kill high-interest debt first. Get compound interest working for you instead of against you. Our debt payoff plan shows exactly how.

6. Never break the chain. The market will go up, down, and sideways. Over decades, compound interest rewards patience and consistency. The first 10 years feel like nothing is happening. Year 25 feels like magic.

FAQ

How much do I need to start?

$1. Fractional shares let you buy a piece of any ETF for a dollar. The barrier isn’t money — it’s the decision to start.

Does compound interest work in a savings account?

Yes, but slowly. A HYSA earning ~4% is better than a traditional account at 0.01%, but far below the 8–10% historical market average. HYSAs are for your emergency fund; investing is for compound growth. See our HYSA guide.

How long until I see real results?

Compound interest is front-loaded with patience and back-loaded with results. The first 5–10 years feel slow. After 15–20 years, the curve bends dramatically upward. You’re buying yourself time on the steep part of the curve.

Is it too late to start at 30? 35? 40?

Never too late. A 40-year-old still has 25+ years of compounding ahead. Less dramatic than starting at 25, but infinitely better than starting at 50 — or never. The best time to plant a tree was 20 years ago. The second best time is today.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: