How to Use a Balance Transfer to Pay Off Credit Card Debt (2026 Guide)

Quick Verdict: It’s a 0% Interest Time-Out — If You Actually Have a Payoff Plan

A balance transfer moves your high-interest credit card debt to a new card with a 0% introductory APR — typically 15–21 months in 2026. During that window, every dollar you pay goes directly toward the actual balance instead of feeding Interest Gravity. No interest charges. No compounding working against you. Just pure principal reduction.

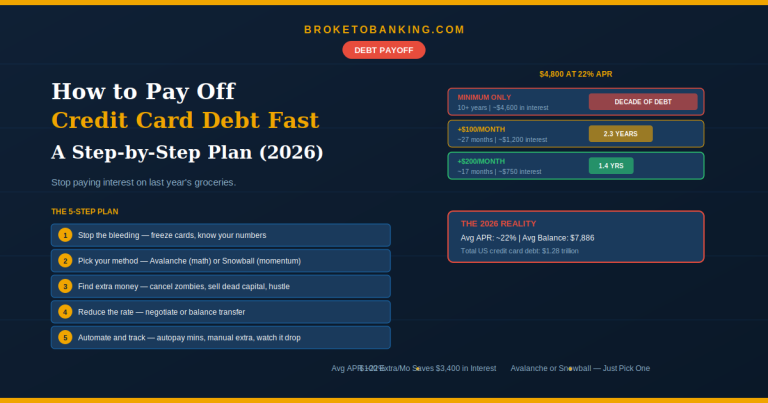

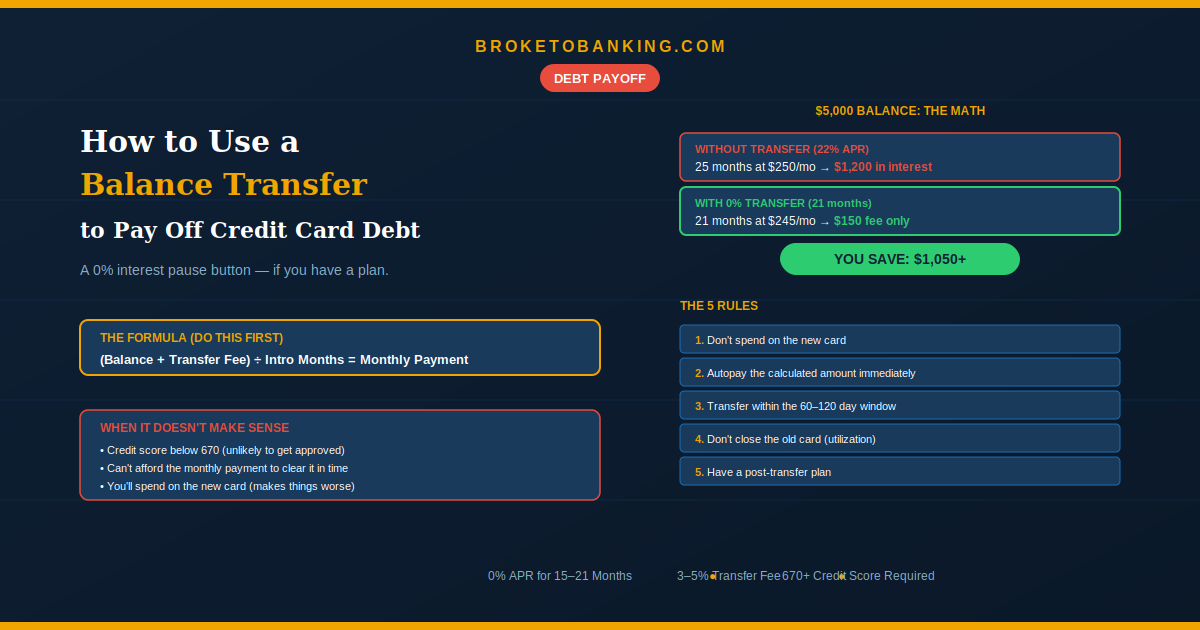

On a $5,000 balance at 22% APR paying $250/month, you’d waste over $1,200 on interest. Transfer that to a 0% card with a 3% fee ($150), and you’re debt-free in 21 months saving over $1,000. But here’s the 2026 reality: the standard 3% fee is becoming a “premium” — many of the longest-running 21-month offers now charge 5%. That changes the math, and you need to run it before you apply.

The Quick Verdict:

- STACK: 21-month 0% offers — the gold standard in 2026 ✅ — Nearly two years of interest-free runway.

- STACK: Do the fee math first ✅ — A 5% fee is a steep entry price. If you can’t pay it off in the window, you’re paying to move your problem around.

- RUNNER UP: Pair with the Debt Avalanche — Transfer your highest-rate card, then avalanche the rest.

- SKIP: Using the new card for anything else ❌ — Buy a latte on your balance transfer card and the interest math becomes a nightmare.

How a Balance Transfer Works

- Apply for a card with a 0% intro APR offer. You’ll need good credit — typically 670+, with 700+ for the best offers.

- Once approved, request the transfer within 60–120 days (the window varies by card).

- Your old balance moves to the new card. You pay a one-time transfer fee (3–5%).

- You now owe the balance at 0% APR for the intro period.

- Pay it off before the promo ends. Anything remaining starts accruing interest at 17–28%.

Important: You can’t transfer within the same issuer — no Chase-to-Chase, no Citi-to-Citi.

The Math You Must Run Before Applying

This is where most people mess up — they apply without knowing whether they can actually clear the balance in time.

The formula: (Balance + Transfer Fee) ÷ Intro Months = Required Monthly Payment

Example ($5,000 balance, 5% fee, 21-month promo):

($5,000 + $250 fee) ÷ 21 = $250/month

If $250/month fits your budget, apply. If it doesn’t, a balance transfer might just be paying a fee to move your problem around.

| Balance | 3% Fee | 5% Fee | 21-Month Payment (at 5%) | 15-Month Payment (at 5%) |

|---|---|---|---|---|

| $3,000 | $90 | $150 | $150/mo | $210/mo |

| $5,000 | $150 | $250 | $250/mo | $350/mo |

| $8,000 | $240 | $400 | $400/mo | $560/mo |

| $10,000 | $300 | $500 | $500/mo | $700/mo |

The 2026 fee reality: In 2024, most cards charged 3%. In 2026, the longest 21-month offers mostly charge 5% — the Success Tax for maximum runway. Some cards still offer 3% if you transfer within the first 4 months, then jump to 5% after. Read the fine print.

The 5 Rules of the 0% Pause Button

1. Lock the New Card Away

The second it arrives, put it in a drawer — or a block of ice. This card is a payoff tool, not a spending card. Here’s the trap most people don’t know: if you make purchases on the same card, your payments are often applied to the 0% transferred balance first, while your new purchases sit there accruing interest at 22%. Don’t touch it.

2. Autopay Is Non-Negotiable

In 2026, many issuers still have a Penalty APR trigger. Miss one payment by 30 days and they can kill your 0% promo and hike you to 29.99%. That’s the Credit Nuke. Set up autopay for at least the minimum — ideally for your full calculated monthly payment.

3. The Ghost Paycheck Redirect

If you were paying $400/month to your old card, keep paying $400/month to the new one — even if the minimum is only $50. Use the 0% window to nuke the principal. The Ghost Paycheck philosophy applies here: automate it, don’t think about it.

4. Don’t Close the Old Card

Once the balance transfers to $0, keep the old account open. Closing it kills your credit utilization — that available credit is actively helping your score. Put one small recurring charge on it (streaming service, phone bill) and autopay in full every month. That’s the Old Growth Bonus.

5. Complete the Transfer Within the Window

Most 2026 offers require you to move the money within 60–120 days of opening. If you wait until month five, you’ve missed the boat and any transfer after the window gets the regular APR, not the promotional 0%.

When a Balance Transfer Doesn’t Make Sense

Credit score below 670. Approval odds are low for the best 0% offers. Focus on the Debt Avalanche and negotiating your current rate instead.

You can’t afford the monthly payment. A balance transfer with a remaining balance at month 22 just moved your debt from one high-interest card to another — plus you paid a fee for the privilege.

Your balance is under $1,500. The transfer fee may eat most of your savings. Run the math — it might still be worth it, but the margin is thin.

You’ll spend on the new card. If you know you’ll use the available credit, the transfer makes things worse. A 5% fee for a temporary hit of dopamine is not a financial strategy.

FAQ

Will it hurt my credit score?

Short-term: small dip from the hard inquiry and high initial utilization on the new card. Long-term: paying down the balance improves utilization, payment history, and overall score. Net effect is positive if you follow through.

Can I transfer multiple cards?

Yes — up to the credit limit of the new card.

What if I can’t pay it off in time?

Transfer to another 0% card if your credit qualifies. Otherwise, pay as much as possible before the deadline. The regular APR kicks in on whatever remains — but on most modern cards, interest is not applied retroactively to the original balance (always confirm the terms).

Balance transfer or personal loan?

A 0% transfer is almost always better if you qualify and can clear it in the intro window. Personal loans (~11% average rate in 2026) make more sense for larger balances you need longer to pay off — the fixed rate and fixed term give you predictability.

The bottom line: A balance transfer is a powerful weapon against Interest Gravity, but only if you have the discipline to pay the bill. Do the math, pick a 21-month card, set your autopay, and give yourself 21 months to change your financial life.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: