How to Pay Off Credit Card Debt Fast in 2026 (A Step-by-Step Plan)

Quick Verdict: Stop Paying Interest on Last Year’s Groceries

The average credit card APR on accounts that carry a balance is roughly 22% right now — three times what most people pay on a mortgage. The typical balance for people carrying debt sits around $7,886. At those rates, minimum payments barely touch the interest, and that takeout you bought in 2024 could still be costing you years from now. You’re literally paying for 2024’s mistakes with 2044’s retirement money.

This isn’t some “someday” problem. This is Interest Gravity — the invisible force we talked about in our debt payoff guide that quietly pulls you backward every single day you carry a balance. The good news? With a clear plan and consistent payments, most people with $2,000–$8,000 in credit card debt can be completely free of it in 12–24 months.

The Quick Verdict:

- STACK: Pick a payoff method (Avalanche or Snowball) and actually stick with it ✅ — Having a strategy beats winging it every time.

- STACK: Pay more than the minimum — even $50 extra a month is a direct attack on Interest Gravity ✅

- RUNNER UP: Negotiate your interest rate — One phone call can save you hundreds. We wrote the exact scripts.

- RUNNER UP: Balance transfer to a 0% intro APR card — A powerful move if you qualify and have the discipline to pay it down.

- SKIP: Debt consolidation loans at similar rates, debt settlement companies, or just ignoring the debt ❌

Step 1: Stop the Bleeding (The Debt Rap Sheet)

Before you throw any extra money at the debt, you have to stop making it worse — and see exactly what you’re fighting.

Freeze the cards. Not cancel — freeze. Remove them from Apple Pay, Amazon, and your browser autofill. Switch to debit or cash for everyday spending. You can’t pay off credit card debt while you’re still adding to it.

Build your Debt Rap Sheet. List every card: the balance, the APR, and the minimum payment. You can’t fight what you haven’t measured.

| Card | Balance | APR | Minimum Payment |

|---|---|---|---|

| Card A | $2,800 | 24.99% | $56 |

| Card B | $1,400 | 19.99% | $35 |

| Card C | $600 | 22.99% | $25 |

| Total | $4,800 | $116 |

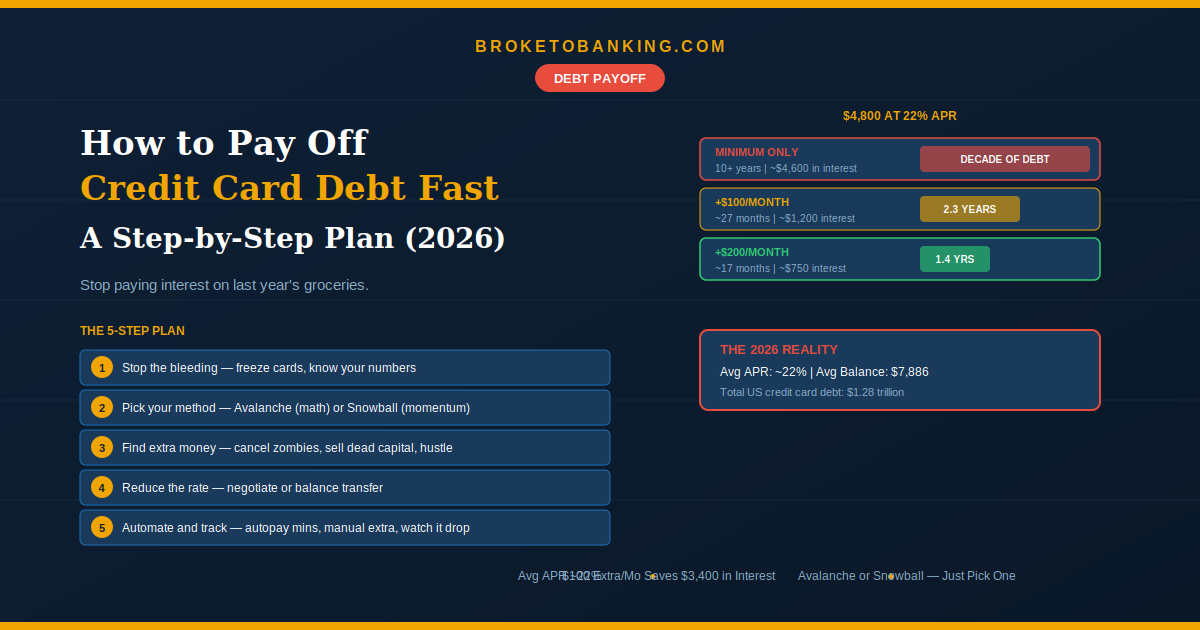

Look at Card A. At 24.99%, it’s a financial house fire — costing you roughly $1.90 a day in interest alone. If you only pay minimums on $4,800 at ~22% APR, you’ll be stuck in debt for over a decade and pay almost as much in interest as the original balance. That’s the Minimum Payment Multiplier we explained in our minimum payments article. The math is brutal — but it’s also the motivation you need.

Step 2: Pick Your Payoff Method

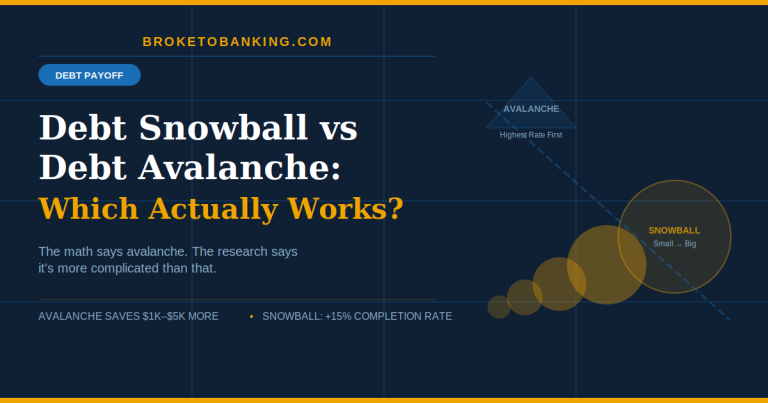

We broke down Snowball vs. Avalanche in detail in Post #8. Here’s the quick version:

Debt Avalanche (The Researcher’s Move): Pay minimums on everything, throw every extra dollar at the highest-APR card first. Mathematically minimizes total interest. Best if you’re motivated by saving the most money.

Debt Snowball (The Psychology Move): Pay minimums on everything, throw every extra dollar at the smallest balance first. Seeing a balance hit $0 gives you the Dopamine Hit that keeps you motivated to finish the job.

Which one? Use our Rate Gap Test: if the APR spread between your cards is more than 10 points, Avalanche saves you real money. Under 5 points? Snowball’s momentum is worth the minor extra interest — the Motivation Tax.

In the example above, Card A (24.99%) vs. Card B (19.99%) is only a 5-point spread. Either method works. If that $600 on Card C has been bugging you, knock it out first with Snowball and free up that $25 payment to attack Card A.

Step 3: Find Extra Money to Throw at the Debt

Minimum payments are designed to keep you in debt. The only way to speed things up is to pay more.

Audit your subscriptions. We’ve talked about Zombie Subscriptions in several posts — recurring charges for stuff you forgot about. Cancel anything you haven’t used in 30 days. Even $30/month freed up is $360/year straight to your debt.

Apply the Windfall Rule. Tax refunds, birthday cash, rebates, cash-back rewards — every unexpected dollar goes straight to your target card before it hits your checking account.

Run a Liquidation Sprint. Walk through your house. That old treadmill, the spare laptop, the designer shoes you never wear — that’s Dead Capital. Set a goal: sell $500 worth of stuff on Facebook Marketplace this weekend. Apply 100% to your target card. One liquidation sprint can shave months off your payoff timeline. We outlined the full process in Post #12.

Add a side hustle. Even $300/month from a realistic side hustle dedicated entirely to debt payoff can cut years off your timeline.

Step 4: Reduce the Interest Rate

Every percentage point you shave off your APR means more of your payment hits the actual balance.

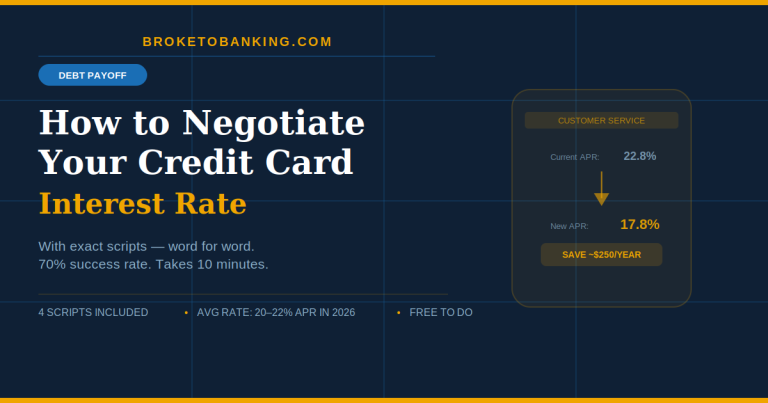

Call and negotiate. Use this line: “I’ve been a customer for X years, but my current APR is making it hard to stay current. I see competitors offering lower rates — what can you do to help me keep my account with you?” Many people who ask get a reduction. We wrote exact scripts for this — the Loyalty Tax Reversal in action.

Balance transfer. If your credit score is 670+, a 0% intro APR card can pause interest for 12–21 months. The typical transfer fee is 3–5% ($144–$240 on $4,800). But at 22% APR, you’d pay roughly $1,050 in interest over a year. The math clearly favors the transfer if you can pay it down during the intro window.

The Skeptic’s Friction Report:

Balance transfers are a tool, not a miracle. If you transfer the balance and keep spending on the old cards, you’ve built a bigger trap. The rules: don’t use the new card for purchases, don’t add balances to the old cards, and have a clear payoff plan that clears everything before the intro rate expires. If you can’t commit, skip the transfer and focus on paying more each month at your current rate.

Step 5: Automate and Track

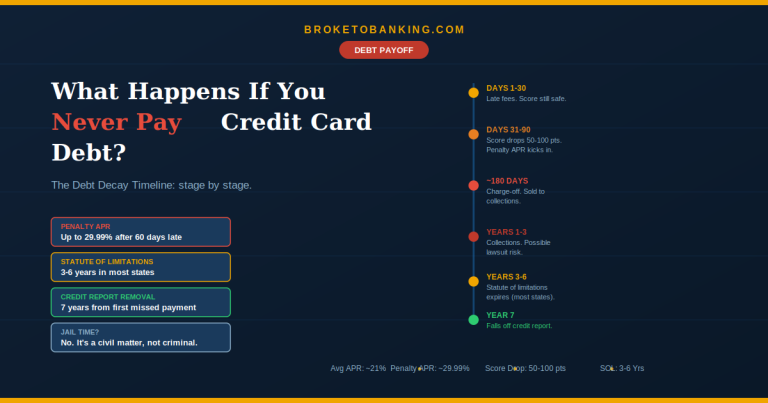

Set up autopay for at least the minimum on every card — this is your Insurance Policy against a 30-day late mark that can tank your credit score by up to 100 points and trigger a penalty APR as high as 27–30%. Then manually push extra payments to your target card each payday.

Track your progress monthly. Watching balances drop is the best motivation. Use the Fixed Payment Lock from our minimum payments article: when a card’s minimum drops (because the balance dropped), keep paying the original higher amount. That difference automatically accelerates your payoff without extra effort.

The Payoff Timeline: What to Realistically Expect

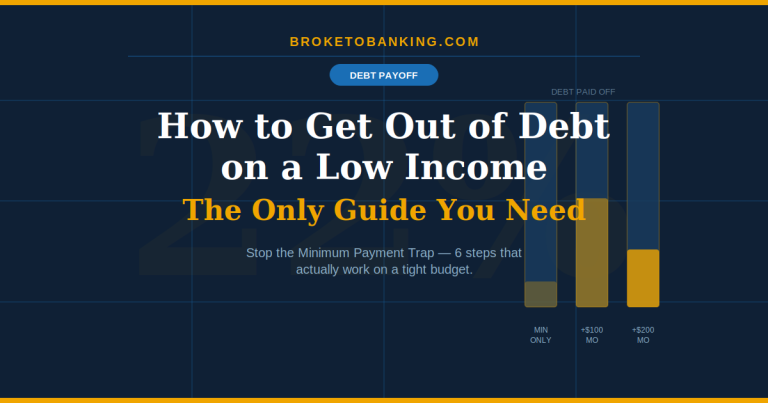

| Extra Payment/Month | Balance at ~22% APR | Time to Payoff | Total Interest Paid |

|---|---|---|---|

| Minimum only (~$116) | $4,800 | 10+ years | ~$4,600 |

| +$100 ($216/mo) | $4,800 | ~27 months | ~$1,200 |

| +$200 ($316/mo) | $4,800 | ~17 months | ~$750 |

| +$300 ($416/mo) | $4,800 | ~13 months | ~$550 |

The difference between minimum payments and $200 extra per month is about 8 years and $3,850 in interest. Even $100 extra completely changes the trajectory.

FAQ

Should I pay off debt or build an emergency fund first?

Both — in the right order. Build a small buffer ($500–$1,000) first so the next car repair doesn’t go right back on the card. Then attack the debt aggressively. See our emergency fund guide for the full Financial Armor strategy. And always capture your full 401(k) match — that 100% return beats even 22% credit card interest.

Should I close my credit cards after paying them off?

Usually no. Closing cards reduces your available credit, which can increase your utilization ratio and hurt your score. Keep them open with zero balances. Just don’t rebuild the debt you just killed.

What about debt settlement companies?

Skip them if you can still make minimum payments. These companies often tell you to stop paying your bills so they can negotiate a lower payoff — which nukes your credit score for up to 7 years. You can negotiate with your issuers yourself for free using our scripts guide. If you truly can’t make minimums, contact a nonprofit credit counseling agency first — they negotiate without the credit destruction.

The bottom line: You didn’t get into this debt in a day, and you won’t get out in a week. But every $50 you pay above the minimum is a direct attack on Interest Gravity. Stop paying for last year’s mistakes and start buying your 2027 freedom.

This article is for educational and informational purposes only. BrokeToBanking.com does not provide financial advice. Please consult a qualified financial professional for guidance specific to your situation.

BrokeToBanking is an independent personal finance blog. We may earn commissions from products we recommend. Our editorial opinions are never influenced by affiliate relationships.

Related Articles: